Understanding and calculating Present Value (PV) is a fundamental skill for anyone involved in financial decision-making, whether for personal investments, business valuations, or project analysis. At its core, PV represents the current worth of a future sum of money or stream of cash flows, given a specified rate of return. In essence, it answers the question: “How much is a future amount of money worth to me today?” This concept is built upon the time value of money (TVM) principle, which asserts that a dollar today is worth more than a dollar tomorrow due to its potential earning capacity.

The ability to accurately calculate PV is crucial for making informed choices that maximize financial returns and mitigate risks. Without this understanding, individuals and businesses risk overvaluing future prospects, leading to suboptimal investment decisions or inflated business valuations. This article will delve into the practicalities of calculating Present Value, exploring its core components, different calculation methods, and its diverse applications within the realm of personal and business finance.

The Fundamentals of Present Value Calculation

Before diving into the formulas and methods, it’s essential to grasp the core components that underpin any PV calculation. These elements work in concert to translate future monetary values into their current equivalents.

The Importance of the Discount Rate

The discount rate is arguably the most critical variable in a PV calculation. It represents the rate of return required by an investor to compensate for the risk and opportunity cost associated with receiving money in the future rather than today. This rate is highly subjective and depends on several factors, including:

- Risk: Higher risk investments demand higher discount rates to compensate for the increased probability of not receiving the expected future cash flows. For example, a highly speculative startup will require a much higher discount rate than a well-established government bond.

- Opportunity Cost: This refers to the return an investor could earn on alternative investments of similar risk. If an investor can reliably earn 8% on a comparable investment, they will likely demand at least 8% to consider a future cash flow.

- Inflation: The erosion of purchasing power due to inflation needs to be factored in. A discount rate should ideally incorporate an inflation premium to ensure the real value of future money is considered.

- Market Conditions: Prevailing interest rates and overall economic sentiment influence the discount rate. In a rising interest rate environment, discount rates tend to increase.

Choosing an appropriate discount rate is crucial. An arbitrarily low rate will inflate the PV, making a future investment appear more attractive than it truly is, while an overly high rate can lead to dismissing potentially profitable opportunities.

Understanding Future Value (FV)

The Future Value (FV) is the amount of money an investment will grow to at a specific date in the future, based on a given interest rate and compounding period. In the context of PV calculation, the FV is the future sum of money whose current worth we are trying to determine. This could be the anticipated sale price of an asset, the maturity value of a bond, or the projected income from a business venture.

The Role of Time Period (n)

The time period (n) refers to the number of periods between the present date and the date on which the future cash flow will be received. These periods are typically expressed in years, but can also be months, quarters, or any other consistent time unit, depending on the frequency of cash flows and the discount rate. The longer the time period, the greater the impact of discounting, as the future sum has more time to be affected by compounding or the opportunity cost.

Cash Flows (CF)

For more complex scenarios involving multiple future payments, the Cash Flow (CF) refers to the individual amounts of money expected to be received or paid at specific points in the future. When calculating the PV of a series of cash flows, each individual cash flow is discounted back to the present, and then these individual present values are summed up to arrive at the total PV.

Methods for Calculating Present Value

There are several methods to calculate Present Value, ranging from simple formulas for single cash flows to more sophisticated approaches for annuities and uneven cash flows. The choice of method depends on the nature of the future cash flows.

Calculating the Present Value of a Single Sum

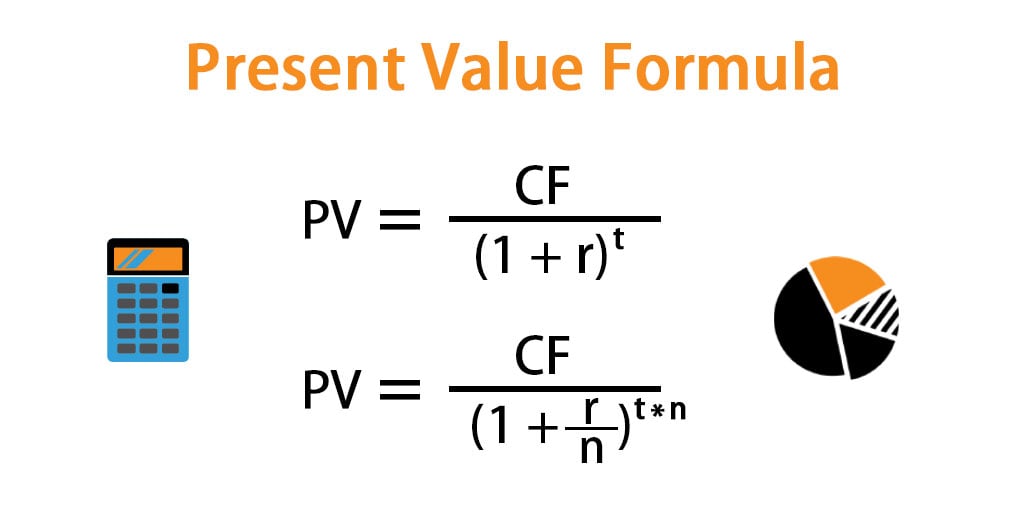

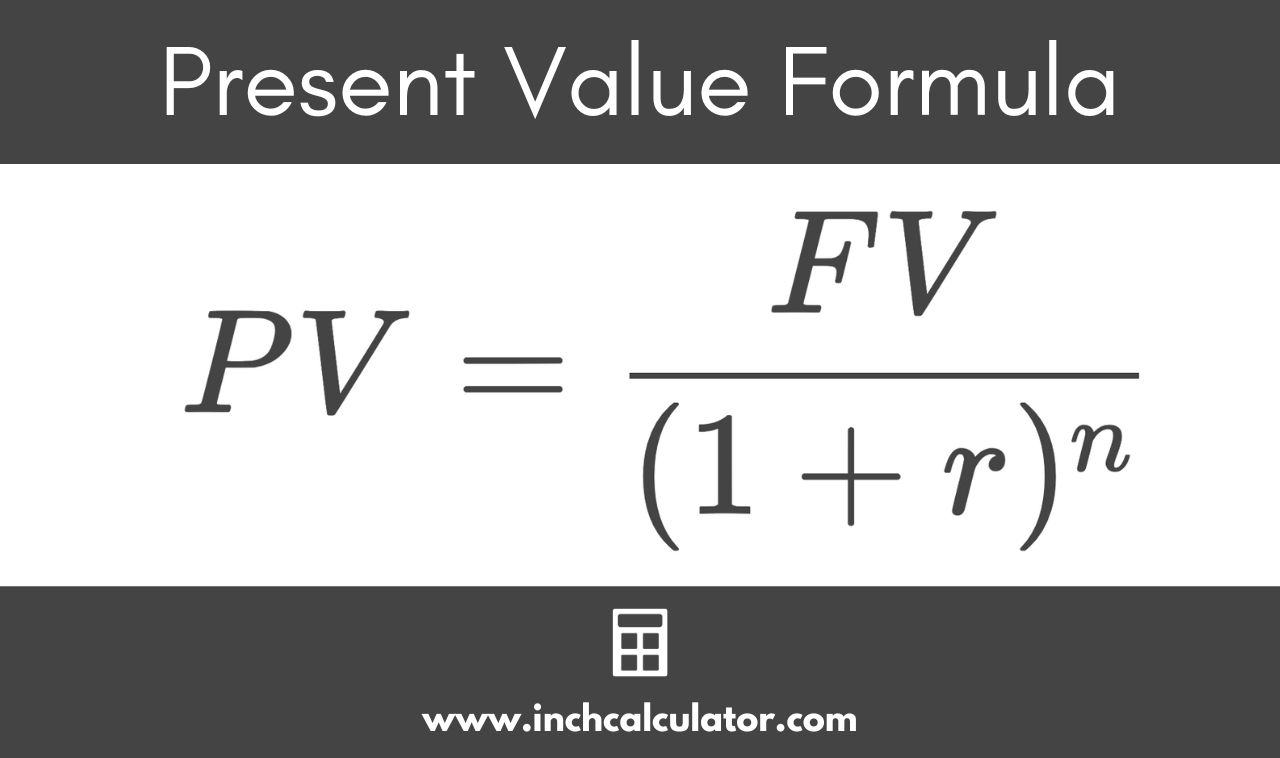

The most basic PV calculation involves a single future sum of money. The formula is as follows:

PV = FV / (1 + r)^n

Where:

- PV = Present Value

- FV = Future Value (the amount of money you expect to receive in the future)

- r = Discount rate per period (expressed as a decimal, e.g., 5% = 0.05)

- n = Number of periods (years, months, etc.)

Example: Suppose you are offered an investment that will pay you $10,000 in 5 years. You require an annual rate of return of 7%.

- FV = $10,000

- r = 0.07

- n = 5

PV = $10,000 / (1 + 0.07)^5

PV = $10,000 / (1.07)^5

PV = $10,000 / 1.40255

PV ≈ $7,129.86

This means that $10,000 received in 5 years is equivalent to $7,129.86 today, assuming a 7% annual discount rate.

Calculating the Present Value of an Ordinary Annuity

An ordinary annuity is a series of equal cash flows occurring at regular intervals, with the payments made at the end of each period. For example, receiving $1,000 every year for 10 years would constitute an ordinary annuity. The formula for the present value of an ordinary annuity is:

PV = C * [1 – (1 + r)^-n] / r

Where:

- PV = Present Value of the annuity

- C = Cash flow per period (the equal amount paid each period)

- r = Discount rate per period

- n = Number of periods

Example: You are offered an investment that will pay you $2,000 at the end of each year for the next 10 years. Your required rate of return is 6% per year.

- C = $2,000

- r = 0.06

- n = 10

PV = $2,000 * [1 – (1 + 0.06)^-10] / 0.06

PV = $2,000 * [1 – (1.06)^-10] / 0.06

PV = $2,000 * [1 – 0.558395] / 0.06

PV = $2,000 * [0.441605] / 0.06

PV = $2,000 * 7.36009

PV ≈ $14,720.18

This means that receiving $2,000 annually for 10 years, discounted at 6%, is equivalent to receiving $14,720.18 today.

Calculating the Present Value of an Annuity Due

An annuity due is similar to an ordinary annuity, but the payments are made at the beginning of each period rather than at the end. This slight difference significantly impacts the PV because each payment is received one period sooner, and thus has one less period to be discounted. The formula for the present value of an annuity due is:

PV = C * [1 – (1 + r)^-n] / r * (1 + r)

Notice that this formula is the same as the ordinary annuity formula multiplied by (1 + r).

Example: Using the same scenario as the ordinary annuity example, but assume the $2,000 payments are made at the beginning of each year.

- C = $2,000

- r = 0.06

- n = 10

PV = $2,000 * [1 – (1 + 0.06)^-10] / 0.06 * (1 + 0.06)

PV = $14,720.18 * 1.06 (from the previous ordinary annuity calculation)

PV ≈ $15,503.39

The PV of the annuity due is higher because each payment is received earlier.

Calculating the Present Value of Uneven Cash Flows

When cash flows are not equal or do not occur at regular intervals, a more detailed approach is needed. This involves discounting each individual cash flow back to the present and then summing up all the individual present values.

PV = CF1 / (1 + r)^1 + CF2 / (1 + r)^2 + … + CFn / (1 + r)^n

Where:

- CF1, CF2, …, CFn are the cash flows for periods 1, 2, …, n respectively.

- r is the discount rate per period.

- n is the number of periods.

Example: An investment is expected to generate the following cash flows over the next three years: Year 1: $5,000, Year 2: $8,000, Year 3: $12,000. The required rate of return is 9%.

- r = 0.09

PV = $5,000 / (1 + 0.09)^1 + $8,000 / (1 + 0.09)^2 + $12,000 / (1 + 0.09)^3

PV = $5,000 / 1.09 + $8,000 / 1.1881 + $12,000 / 1.295029

PV = $4,587.16 + $6,733.40 + $9,266.19

PV ≈ $20,586.75

This method is fundamental for valuing businesses, real estate, or any investment with a stream of irregular future income.

Practical Applications of Present Value Calculations

The ability to calculate Present Value is not merely an academic exercise; it has profound and practical implications across various financial contexts, enabling more informed and strategic decision-making.

Investment Appraisal and Capital Budgeting

For businesses, PV is a cornerstone of investment appraisal and capital budgeting. When considering a new project or capital expenditure, businesses use PV analysis to determine if the expected future returns justify the initial investment.

-

Net Present Value (NPV): This is a widely used metric that calculates the difference between the present value of future cash inflows and the present value of initial cash outflows.

NPV = Sum of PV of future cash flows – Initial Investment

A positive NPV generally indicates that the project is expected to be profitable and should be undertaken, assuming it meets the company’s required rate of return. A negative NPV suggests the project is likely to be a loss-making endeavor. -

Internal Rate of Return (IRR): While not directly a PV calculation, IRR is intrinsically linked. IRR is the discount rate at which the NPV of an investment equals zero. Businesses compare the IRR to their hurdle rate (minimum acceptable rate of return) to decide on project viability. If IRR > Hurdle Rate, the project is considered attractive.

Business Valuation

When valuing a business, analysts often project its future earnings or cash flows and then discount them back to the present to arrive at an estimated current value. This is known as the Discounted Cash Flow (DCF) method. The accuracy of the valuation heavily relies on the reliability of the cash flow projections and the appropriateness of the chosen discount rate. A higher discount rate will result in a lower valuation, reflecting higher perceived risk or opportunity cost.

Loan and Bond Analysis

Lenders and investors use PV to determine the fair value of loans and bonds. For a bond, the PV of its future coupon payments and its face value at maturity, discounted at the market interest rate, represents its current market price. Understanding PV helps investors assess whether a bond is trading at a premium, discount, or at par value. Similarly, borrowers can understand the true cost of a loan by considering the PV of all future payments.

Personal Finance Decisions

While not always as formal as in corporate finance, PV principles are implicitly used in personal financial planning.

- Retirement Planning: Estimating how much money you need to save today to fund your desired retirement lifestyle requires discounting future retirement expenses and income streams back to the present.

- Major Purchases: Deciding whether to buy or lease a car, or whether to pay cash for a home or take out a mortgage, often involves comparing the PV of different financial options.

- Evaluating Job Offers: Comparing salary offers with different payment structures or benefits can involve calculating the PV of the total compensation package to make an apples-to-apples comparison.

Tools and Techniques for PV Calculation

While the formulas provide the theoretical framework, various tools and techniques can simplify and expedite PV calculations, making them more accessible for both individuals and professionals.

Financial Calculators

Dedicated financial calculators are programmed with built-in functions for PV, FV, PMT (payment), n, and i (interest rate). These devices are invaluable for quick and accurate calculations, especially for complex annuity scenarios. They eliminate the need for manual formula input and reduce the risk of calculation errors.

Spreadsheet Software (Excel, Google Sheets)

Spreadsheet software offers powerful and flexible tools for PV calculations. They provide dedicated functions that mirror those on financial calculators:

-

PV Function:

=PV(rate, nper, pmt, [fv], [type])rate: The discount rate per period.nper: The total number of periods.pmt: The payment made each period (for annuities).fv: The future value (optional, if not provided, it defaults to 0).type: When payments are due (0 = end of period, 1 = beginning of period).

-

FV Function: Can be used to calculate the future value, which is then used in the PV formula.

-

NPV Function:

=NPV(rate, value1, [value2], ...)This function calculates the NPV of a series of cash flows, assuming the first cash flow occurs at the end of the first period. For projects where the initial investment is at time zero, you would typically subtract the initial investment from the result of the NPV function.

Spreadsheets are particularly useful for scenarios involving uneven cash flows, allowing users to create a table of cash flows and apply the PV formula to each, or use the NPV function for more streamlined analysis.

Online Calculators and Software

A plethora of online financial calculators and specialized financial modeling software are available. These tools can perform PV calculations with varying degrees of complexity, often with user-friendly interfaces. They are an excellent resource for quick estimations or for individuals who may not have regular access to financial calculators or spreadsheet software. However, it’s important to verify the source and reliability of any online calculator.

The Importance of Data Accuracy and Assumptions

Regardless of the tool used, the accuracy of the PV calculation is entirely dependent on the accuracy of the input data and the validity of the underlying assumptions.

- Reliable Cash Flow Projections: Overly optimistic or pessimistic forecasts for future cash flows will lead to skewed PV results. Thorough research, market analysis, and realistic estimations are paramount.

- Appropriate Discount Rate Selection: As discussed, the discount rate is highly subjective. A poorly chosen discount rate can invalidate the entire analysis. This requires a deep understanding of risk, opportunity cost, and market conditions.

- Consistent Time Periods: Ensure that the discount rate and the time periods are aligned (e.g., if the rate is annual, the periods must be in years).

By diligently applying these calculation methods and employing appropriate tools while maintaining a critical eye on the underlying assumptions, individuals and businesses can leverage the power of Present Value to make more robust and financially sound decisions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.