In the realm of personal finance, interest is the invisible force that either builds your wealth or silently erodes your purchasing power. Whether you are looking at the growth of a high-yield savings account or the mounting balance on a credit card, understanding how interest is calculated on a monthly basis is a fundamental skill. It transforms financial literacy from a vague concept into a practical tool for decision-making.

When you understand the mechanics of monthly interest, you gain the ability to compare financial products accurately, plan your debt repayment strategies, and project your future investment growth. This guide provides a comprehensive breakdown of how to calculate monthly interest, the nuances of different compounding methods, and the practical applications of these formulas in your daily financial life.

Understanding the Core Components of Monthly Interest

Before diving into the formulas, it is essential to define the variables that dictate how much interest you will owe or earn. Interest is essentially the “rent” paid for the use of money. To calculate it accurately, you need three primary pieces of data.

Principal Balance: The Starting Point

The principal is the original amount of money involved in the transaction. In a loan scenario, the principal is the amount you borrowed. In a savings or investment scenario, it is the amount you initially deposited. It is important to note that for many financial products, the principal balance fluctuates. For instance, as you make payments on a mortgage, the principal decreases, which in turn reduces the amount of interest charged in subsequent months.

Annual Percentage Rate (APR) vs. Monthly Rate

Most financial institutions quote interest rates in annual terms, known as the Annual Percentage Rate (APR). However, because interest is often applied monthly, you must convert this annual figure into a periodic rate.

To find the monthly interest rate, you divide the APR by 12 (the number of months in a year). For example, if you have a credit card with an 18% APR, your monthly interest rate is 1.5% (0.18 / 12 = 0.015). Understanding this distinction is vital because while 18% sounds high, seeing the 1.5% monthly figure helps you understand exactly how much “rent” you are paying on your balance every 30 days.

The Role of the Time Factor

While we are focusing on monthly calculations, time is always the multiplier in interest equations. In a monthly calculation, the time factor (t) is usually represented as one unit (one month). However, some institutions calculate interest based on the number of days in a specific month (28, 30, or 31), which can lead to slight variations in the final amount. For the sake of standard calculation, using a monthly divisor is the most common approach for personal budgeting.

Step-by-Step Guide: Calculating Simple Monthly Interest

Simple interest is the most straightforward way to calculate the cost of borrowing or the gain on an investment. While it is less common in modern revolving credit, it is frequently used for short-term personal loans and certain types of fixed-term certificates of deposit.

The Standard Formula

The formula for simple interest is:

Interest = Principal × Rate × Time (I = P × r × t)

To find the monthly interest specifically, the formula is adapted:

Monthly Interest = Principal × (Annual Rate / 12) × 1

Converting APR to a Monthly Decimal

To use the formula, you must convert the percentage into a decimal. You do this by dividing the percentage by 100. If your rate is 6%, the decimal is 0.06.

Let’s look at a practical example. Suppose you have a personal loan with a remaining principal of $10,000 and an APR of 6%.

- Convert the APR to a monthly decimal: 0.06 / 12 = 0.005.

- Multiply by the principal: $10,000 × 0.005 = $50.

In this scenario, your interest charge for that specific month is $50. The remainder of your monthly payment would go toward reducing the principal balance.

Why Simple Interest Knowledge Matters

Even if your bank uses more complex methods, knowing how to calculate simple interest provides a “ballpark” figure that prevents you from being misled by predatory lending practices. If your calculated simple interest is significantly lower than what the bank is charging, it is a signal to look closer at the “fine print” regarding fees or compounding frequencies.

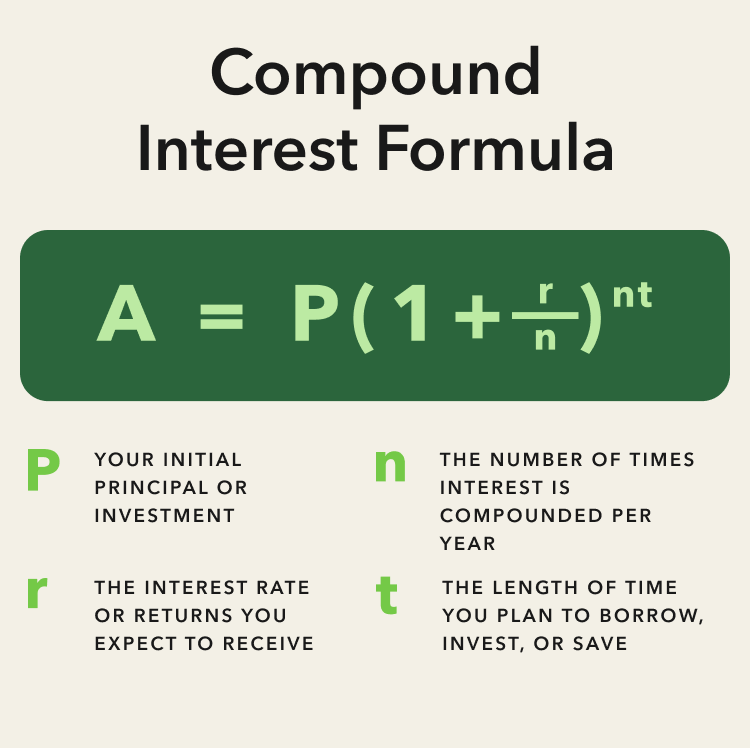

The Power of Compounding: How Monthly Interest Snowballs

In the modern financial world, “Compound Interest” is the standard. Unlike simple interest, which is only calculated on the principal, compound interest is calculated on the principal plus any interest that has already accumulated. This is often described as “interest on interest.”

Simple vs. Compound Interest: Key Differences

The primary difference lies in the growth curve. Simple interest grows linearly, while compound interest grows exponentially. For a saver, compounding is a best friend; for a debtor, it can be a significant burden. When interest is compounded monthly, the balance increases every month, and the next month’s interest is calculated based on that new, higher balance.

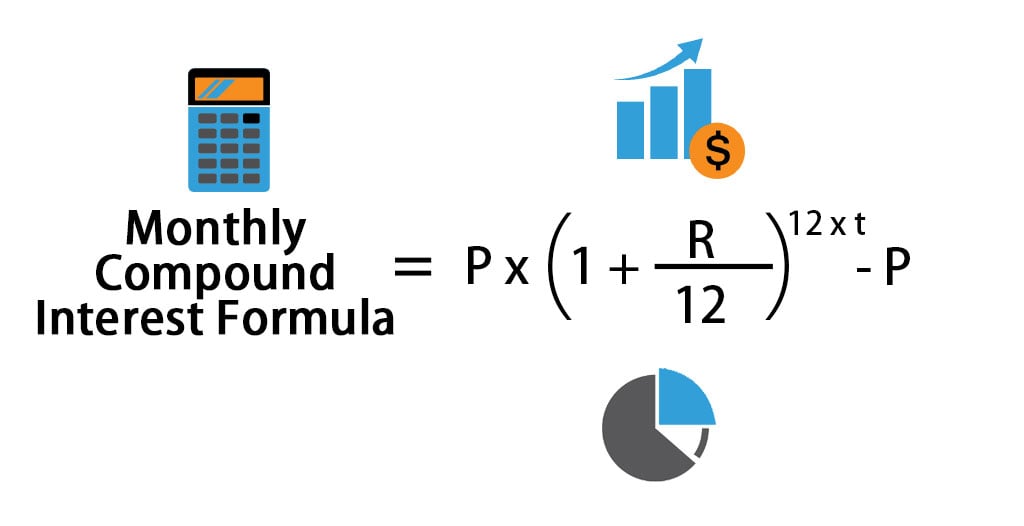

Calculating Compound Interest Manually

To calculate the total balance (Principal + Interest) after one month of compounding, you use the formula:

A = P (1 + r/n)

Where:

- A is the total amount.

- P is the principal.

- r is the annual interest rate (decimal).

- n is the number of compounding periods per year (12 for monthly).

If you want to find just the interest for that month, you subtract the principal from the total amount (A – P). As the months progress, the “P” in the equation becomes the “A” from the previous month, creating the snowball effect.

The Impact of Compounding Frequency

While we are focusing on monthly interest, some accounts compound daily. Daily compounding is common in credit cards and high-yield savings accounts. Even if the statement is issued monthly, the interest is calculated every day. This results in a slightly higher effective yield than monthly compounding. When comparing financial products, always look for the Annual Percentage Yield (APY), which accounts for the frequency of compounding, rather than just the APR.

Specific Applications: Credit Cards, Mortgages, and Savings

The theory of interest calculation is consistent, but different financial products apply these rules in unique ways. Understanding these nuances is critical for effective money management.

Credit Cards: Dealing with Average Daily Balances

Credit cards are unique because you can charge new items and make payments throughout the month. Most credit card issuers use the Average Daily Balance (ADB) method. Instead of just looking at your balance on the last day of the month, they add up your balance for every day in the billing cycle and divide by the number of days.

To calculate your monthly credit card interest:

- Find your ADB by summing your daily balances and dividing by the days in the cycle.

- Divide your APR by 365 to get a daily periodic rate.

- Multiply the ADB by the daily periodic rate.

- Multiply that result by the number of days in the billing cycle.

This is why paying your credit card bill even a few days early can save you money on interest—it lowers your average daily balance.

Mortgages: Amortization and Interest Allocation

Mortgages use a process called amortization. In the early years of a mortgage, your monthly interest calculation is based on a very high principal. Consequently, a large portion of your monthly payment goes toward interest, and very little goes toward the principal.

As you pay down the loan, the “Principal” variable in your monthly interest calculation drops. This means the interest charge drops, allowing more of your fixed payment to go toward the principal. Understanding this allows homeowners to see the massive benefit of making even small extra payments toward the principal early in the loan term.

High-Yield Savings Accounts: Maximizing Monthly Accruals

For savings, the calculation works in your favor. Most high-yield savings accounts compound daily and credit the interest to your account monthly. To maximize this, many financial experts suggest depositing your paycheck as early as possible. Since the interest is often calculated on your daily balance, having the money in the account for 30 days instead of 15 days results in a higher interest payment at the end of the month.

Tools and Strategies to Simplify Your Financial Life

While knowing the math is empowering, you don’t have to do it by hand every time. Technology and strategy can help you apply these mathematical principles to improve your net worth.

Leveraging Online Calculators and Spreadsheets

For complex projections, such as a 30-year retirement plan or a 5-year car loan, spreadsheets like Excel or Google Sheets are invaluable. Using the formula =PMT(rate, nper, pv) can help you calculate monthly payments, while =IPMT can help you isolate exactly how much of a specific monthly payment is going toward interest. Online amortization calculators are also excellent for visualizing how interest disappears over the life of a loan.

Strategies for Minimizing Interest Payments

Once you understand how monthly interest is calculated, you can use the “Debt Avalanche” method. This strategy involves listing all your debts and focusing all extra funds on the debt with the highest interest rate first. Mathematically, this is the most efficient way to reduce the total amount of interest you pay over time, as it targets the most expensive “rent” you are paying on borrowed money.

Using Interest Knowledge for Smarter Investing

On the flip side, understanding interest helps you evaluate investment opportunities. If an investment offers a return that is lower than the interest rate on your debt, the math dictates that you should pay off the debt first. By comparing your “monthly interest out” (debt) versus “monthly interest in” (savings/investments), you can create a clear roadmap for wealth building.

In conclusion, the ability to calculate monthly interest is more than just a math exercise; it is a vital component of financial sovereignty. By mastering these formulas and understanding how they apply to various financial products, you move from being a passive participant in your financial life to an active strategist. Whether you are accelerating your journey to being debt-free or optimizing your investment portfolio, the math of interest is the foundation upon which your financial future is built.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.