Compound interest has often been called the “eighth wonder of the world.” This attribution, frequently linked to Albert Einstein, highlights a fundamental truth in the realm of personal finance: the ability of money to grow exponentially over time is the most potent tool in an investor’s arsenal. Unlike simple interest, which is calculated solely on the principal amount, compound interest is calculated on the principal plus the accumulated interest of previous periods.

Understanding how to calculate compounding interest is not merely an academic exercise; it is a vital skill for anyone looking to build long-term wealth, manage debt, or plan for retirement. This guide provides a deep dive into the mechanics, formulas, and strategic applications of compound interest to help you master your financial future.

1. The Mathematical Foundation: Understanding the Formula

At its core, compounding is the process of earning “interest on interest.” To utilize this effectively, one must understand the variables that drive the equation. The standard formula for compound interest is:

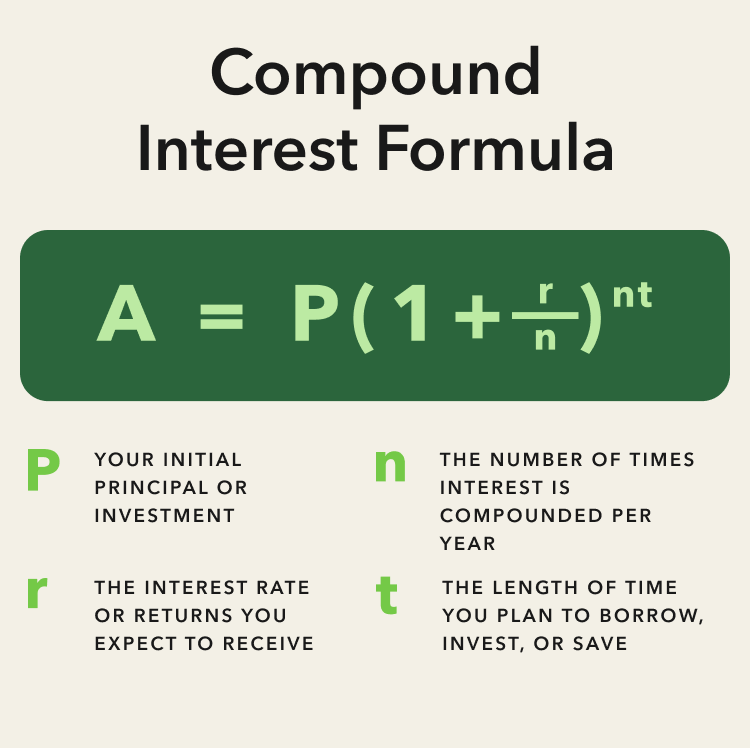

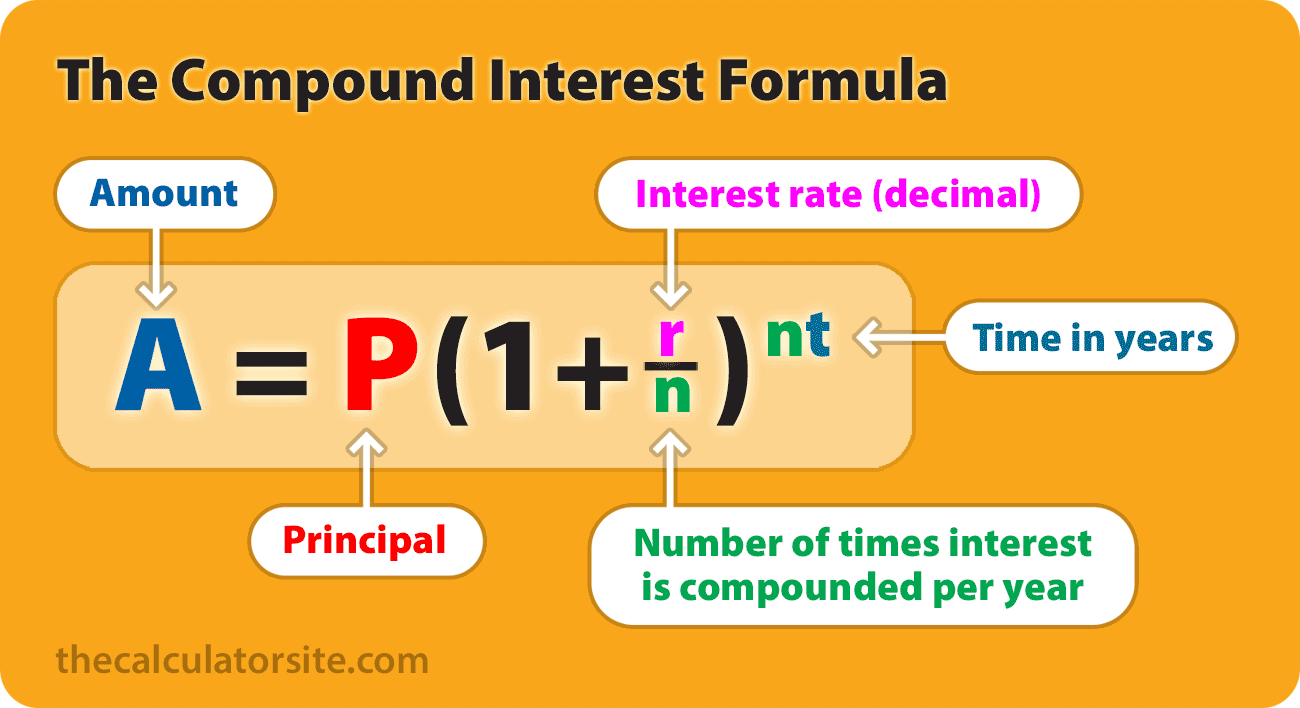

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest.

- P = the principal investment amount (the initial deposit).

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per unit t.

- t = the time the money is invested or borrowed for.

The Variables Explained

Each component of this formula plays a critical role in the final outcome. The principal (P) is your starting point. While a larger principal yields higher absolute returns, the magic of compounding is that even small principals can grow into substantial sums over time.

The interest rate (r) is the engine of growth. However, it is the compounding frequency (n) that often surprises investors. Whether interest is compounded annually, semi-annually, quarterly, monthly, or daily determines how quickly the “interest on interest” effect takes hold. Finally, time (t) is the most influential variable. Because t is an exponent in the equation, increasing the duration of an investment has a far greater impact on the final total than increasing the principal.

Simple Interest vs. Compound Interest

To appreciate compounding, one must contrast it with simple interest. Simple interest is calculated only on the initial principal. For example, $10,000 at a 5% simple interest rate will earn $500 every year, indefinitely. After 20 years, you would have $20,000.

In contrast, with compound interest (compounded annually), that same $10,000 earns $500 in the first year. In the second year, you earn 5% on $10,500, which is $525. By year 20, the total grows to approximately $26,533. The “extra” $6,533 is the result of compounding—money working for you without any additional contribution.

2. Step-by-Step Calculation Methods

While the formula provides the theoretical basis, calculating compound interest in real-world scenarios requires practical application. There are three primary ways to approach these calculations: manual calculation, spreadsheet functions, and financial calculators.

Manual Calculation and the Power of Frequency

To calculate compound interest manually, convert your interest rate to a decimal (e.g., 6% becomes 0.06). If you are calculating monthly compounding for one year, your n is 12 and t is 1.

Consider a $5,000 investment at a 7% interest rate compounded monthly for 5 years:

- Identify variables: P=5000, r=0.07, n=12, t=5.

- Calculate the periodic rate: r/n = 0.07/12 ≈ 0.00583.

- Calculate the total periods: n*t = 12 * 5 = 60.

- Solve the equation: A = 5000 (1 + 0.00583)^60.

- Result: A ≈ $7,088.

Note how daily compounding would yield a slightly higher result than monthly, as the interest is added back to the principal more frequently, allowing it to start earning its own interest sooner.

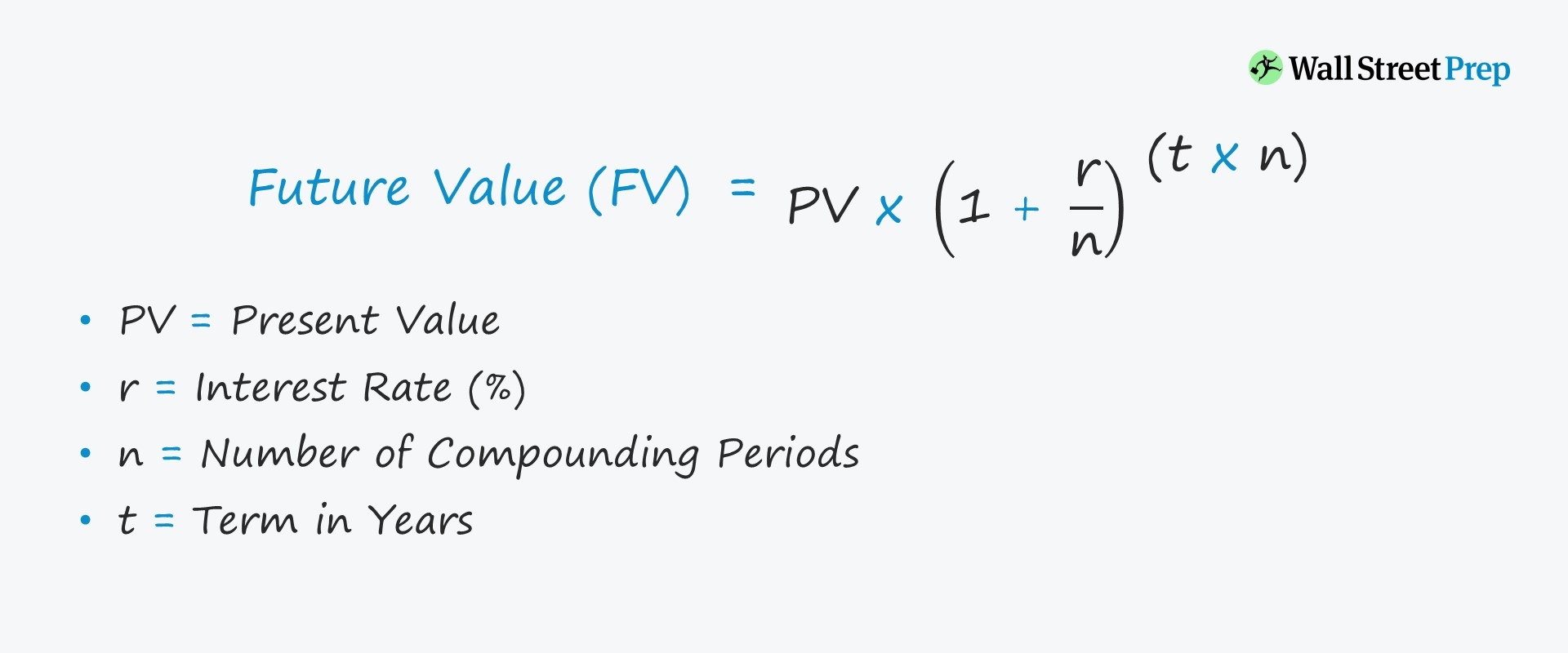

Utilizing Excel and Google Sheets

For more complex financial planning, digital spreadsheets are indispensable. The primary function used for compound interest is the Future Value function: =FV(rate, nper, pmt, [pv], [type]).

- Rate: The interest rate per period (r/n).

- Nper: The total number of payment periods (n*t).

- Pmt: Any additional payments made each period (set to 0 if only calculating the initial principal).

- Pv: The present value or principal (entered as a negative number to represent an outflow).

Using a spreadsheet allows you to create “what-if” scenarios, such as seeing how an extra $100 a month in contributions changes your retirement outlook over 30 years.

The Rule of 72: A Mental Shortcut

For those who need a quick estimate without a calculator, the “Rule of 72” is a classic personal finance tool. To find out approximately how many years it will take for your money to double at a given compound interest rate, divide 72 by the annual interest rate.

For instance, at a 6% return, your money will double in 12 years (72 / 6 = 12). At a 10% return, it takes just 7.2 years. This shortcut illustrates the dramatic difference a few percentage points can make over a lifetime of investing.

3. Strategic Applications in Wealth Building

Understanding the math is only the first step; applying it to your financial strategy is where wealth is truly built. Compounding is a double-edged sword: it can build a fortune when investing, but it can also lead to financial ruin when managing high-interest debt.

Maximizing Investment Vehicles

Different financial products offer different compounding advantages.

- Savings Accounts and CDs: These typically offer monthly or daily compounding. While the rates are often lower than the stock market, the safety and frequent compounding make them ideal for emergency funds.

- Dividend Reinvestment Plans (DRIPs): In the stock market, one of the most effective ways to leverage compounding is by reinvesting dividends. Instead of taking the cash, you use the dividend to buy more shares, which in turn produce more dividends. This creates a powerful compounding loop.

- Retirement Accounts (401k/IRA): These accounts allow your investments to compound tax-deferred or tax-free. In a standard brokerage account, you might owe taxes on capital gains or dividends each year, which “leaks” money out of the compounding engine. Tax-advantaged accounts keep that money working for you.

The Cost of Delay

The most critical factor in compounding is time. This is often illustrated by the “Two Savers” anecdote. Saver A starts investing $200 a month at age 25 and stops at age 35, never adding another cent. Saver B starts at age 35 and invests $200 a month until age 65.

Even though Saver B invested for 30 years and Saver A only invested for 10, Saver A often ends up with a larger portfolio because their money had an extra decade to compound. The lesson is clear: the best time to start calculating and utilizing compound interest was yesterday; the second-best time is today.

Managing Negative Compounding (Debt)

Compounding works against you in the form of high-interest debt, such as credit cards. Credit card companies typically compound interest daily. If you only pay the minimum, the interest charges are added to your balance, and you begin paying interest on your interest. This is why credit card debt can feel impossible to escape; the exponential growth of the debt can quickly outpace your ability to pay down the principal. Understanding this calculation should motivate borrowers to prioritize high-interest debt repayment to stop the “reverse compounding” effect.

4. Advanced Considerations: Inflation and Real Returns

When calculating compound interest for long-term goals, it is essential to distinguish between nominal returns and real returns.

Factoring in Inflation

If your investment compounds at 7% but inflation is at 3%, your “real” purchasing power is only growing at approximately 4%. When planning for a retirement 30 years away, failing to account for inflation can lead to a significant shortfall. Sophisticated investors often subtract the expected inflation rate from their interest rate (r) in the compounding formula to get a more accurate picture of their future wealth in today’s dollars.

The Impact of Taxes and Fees

Just as inflation erodes the value of compounding, so do taxes and management fees. A 1% annual management fee might seem small, but when applied to a compounding balance over 40 years, it can reduce the final portfolio value by hundreds of thousands of dollars. This is because the fee isn’t just taking your money; it’s taking the future interest that money would have earned. When calculating your future wealth, always use a “net” interest rate that accounts for these costs.

Conclusion: The Path to Financial Freedom

Mastering the calculation of compound interest is a transformative milestone in personal finance. It shifts your perspective from linear thinking—where wealth is built only through labor—to exponential thinking, where wealth is built through strategic capital allocation.

By understanding the formula $A = P(1 + r/n)^{nt}$, utilizing digital tools for precision, and respecting the unparalleled power of time, you can design a financial roadmap that ensures long-term security. Whether you are seeking to optimize your 401(k), pay down a mortgage, or simply understand the growth of a high-yield savings account, the principles of compounding remain the same. Start early, stay consistent, and let the math of compounding do the heavy lifting for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.