For most people, a car loan represents one of the largest financial commitments they’ll make outside of a mortgage. Yet, despite its significant impact on personal finances, many borrowers focus solely on the monthly payment or the advertised interest rate, overlooking a crucial metric: the Annual Percentage Rate (APR). Understanding and knowing how to calculate (or more accurately, determine and interpret) the APR on your car loan is not merely an academic exercise; it is a fundamental step toward intelligent financial decision-making, ensuring you grasp the true cost of borrowing and can compare loan offers effectively.

The APR provides a holistic view of your loan’s cost, encompassing not just the interest charged but also various fees levied by the lender. Ignoring it can lead to paying substantially more than anticipated over the life of your loan. This comprehensive guide will demystify APR, break down its components, offer practical approaches to understanding its calculation, and underscore its profound impact on your financial health. By the end, you’ll be equipped to evaluate car loan offers with confidence, ensuring you secure the most advantageous terms possible.

Understanding APR: More Than Just the Interest Rate

When you apply for a car loan, lenders will quote you an interest rate, which is the percentage of the principal loan amount they charge you for borrowing their money. However, the true cost of that loan extends beyond this percentage. This is where the Annual Percentage Rate (APR) comes into play, offering a more complete and accurate picture.

What is APR and How Does It Differ from the Interest Rate?

The interest rate is simply the cost of borrowing money, expressed as a percentage of the principal. It’s the compensation lenders receive for letting you use their capital. If you borrow $20,000 at a 5% interest rate, you’ll pay 5% of the outstanding balance in interest annually (or amortized monthly).

The Annual Percentage Rate (APR), on the other hand, is a broader measure of the cost of borrowing. It includes the stated interest rate plus certain upfront fees charged by the lender, spread out over the loan term. These fees can include origination fees, documentation fees, processing fees, credit report fees, and sometimes even prepaid interest or discount points. The APR is expressed as a single annual percentage, making it an excellent tool for comparing different loan offers, as it accounts for all mandatory lender charges.

Imagine two loan offers:

- Offer A: 5% interest rate, no fees. APR = 5%.

- Offer B: 4.5% interest rate, but with $500 in upfront fees. The APR for Offer B would be higher than 4.5% because those fees are folded into the total cost of borrowing, effectively increasing the percentage you pay annually.

Why APR Matters Critically for Car Loans

For car loans, focusing solely on the interest rate can be misleading. A lower interest rate might look appealing on the surface, but if it’s accompanied by hefty fees, the actual APR could be higher than a loan with a slightly higher interest rate but no associated fees. The APR allows for an “apples-to-apples” comparison between different loan products from various lenders.

By understanding your APR, you gain clarity on:

- The Total Cost of Borrowing: You see the comprehensive cost, not just a partial figure.

- Effective Comparison: It becomes the ultimate metric for evaluating and comparing loan offers, helping you identify the truly cheapest option.

- Informed Decision-Making: Armed with this knowledge, you can negotiate better terms or choose a lender whose fees and rates align with your financial goals.

Fixed vs. Variable APR

While most car loans come with a fixed APR, meaning the interest rate and fees remain constant for the life of the loan, it’s worth noting the distinction. A variable APR (more common in credit cards or some mortgages) fluctuates with a benchmark interest rate, like the prime rate. For car loans, stability is usually preferred, and fixed APRs provide predictability in your monthly payments and total cost. Always confirm whether your car loan offers a fixed or variable APR, though fixed is the norm for vehicle financing.

Key Components Influencing APR Calculation

Calculating the exact APR on a car loan is a complex actuarial process, often performed by financial software. However, understanding the factors that feed into this calculation is essential for grasping its significance. The APR fundamentally aggregates the core financial elements of your loan, presenting them as an annualized percentage.

The Principal Loan Amount

This is the initial sum of money you are borrowing to purchase the car. It’s the sticker price of the vehicle minus any down payment, trade-in value, or rebates. A larger principal generally means a larger overall interest payment, but it doesn’t directly dictate the APR unless the fees are a fixed dollar amount, in which case they represent a smaller percentage of a larger principal.

The Stated Interest Rate

As discussed, this is the base percentage rate the lender charges you for borrowing the principal. It’s typically determined by factors such as your credit score, the loan term, the vehicle’s age, and market interest rates set by central banks. This is the most significant component of the APR.

Loan Term (Duration of Repayment)

The loan term is the period over which you agree to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term can result in lower monthly payments, it almost invariably leads to a higher total amount of interest paid over the life of the loan. Critically for APR, a longer term spreads the fixed upfront fees over a longer period, which can slightly decrease the effective annualized percentage impact of those fees, but the total cost of interest will still increase.

Lender Fees and Charges

These are the additional costs that lenders might impose to cover their administrative expenses or as a condition of the loan. When these fees are rolled into the loan or paid upfront, they contribute directly to raising the APR above the stated interest rate. Common fees include:

- Origination Fees: A charge for processing the loan.

- Documentation Fees (Doc Fees): Fees for preparing and processing loan paperwork.

- Credit Report Fees: The cost of pulling your credit report.

- Underwriting Fees: Fees for evaluating your creditworthiness.

- Prepaid Interest: Some lenders might require you to pay a portion of interest upfront.

- Discount Points: Fees paid to the lender in exchange for a lower interest rate (less common in car loans but possible).

It’s crucial to differentiate between lender fees (which are included in APR) and third-party fees, such as dealership fees, registration fees, taxes, or extended warranty costs, which are typically not included in the APR calculation. However, if these third-party fees are financed as part of the total loan amount, they will increase your principal, and thus the total interest you pay, but they don’t directly inflate the APR itself unless the lender specifically includes them in their APR calculation (which is rare for non-lender fees). Always scrutinize your loan estimate for a clear breakdown of all charges.

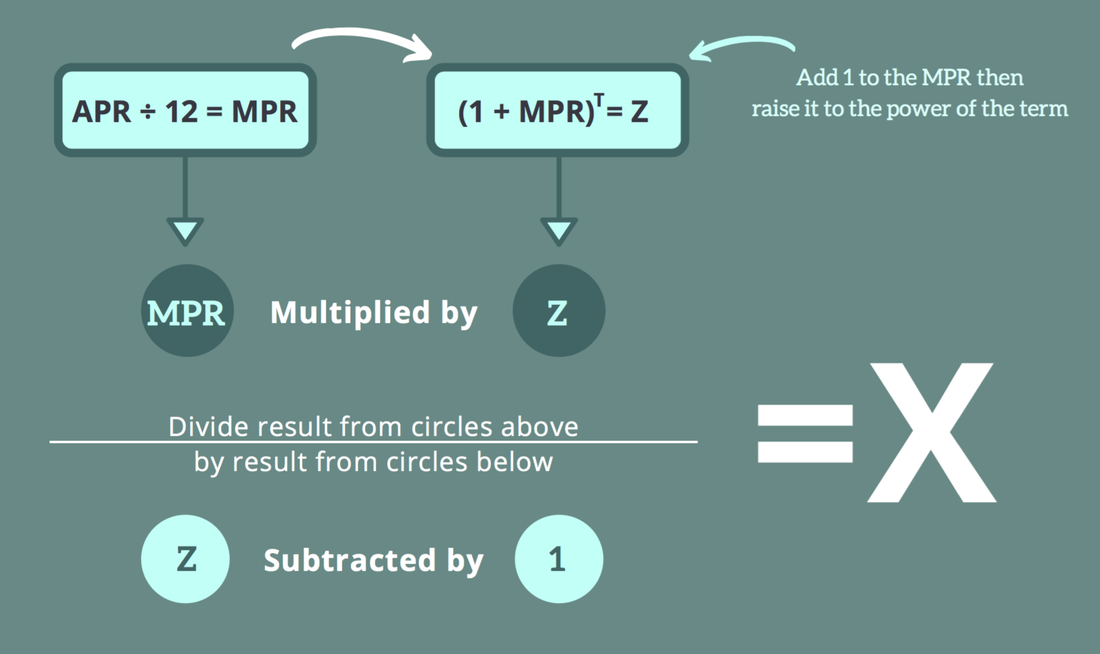

Deconstructing the APR Determination: A Practical Approach

The exact mathematical calculation of APR involves complex financial formulas that account for the time value of money, requiring iterative processes often handled by specialized software. For most consumers, the goal isn’t to manually derive the APR from first principles, but rather to understand how it’s presented, what it means, and how to verify it using practical tools.

The Theoretical Foundation: Why It’s More Than Simple Interest

APR isn’t simply the total interest plus fees divided by the principal and then annualized. Instead, it represents the uniform annual rate that, when applied to the declining loan balance, results in the total payments (principal, interest, and includable fees) matching the loan amount. It effectively “re-calculates” the interest rate such that it incorporates all mandatory lender fees as if they were additional interest. This is why financial calculators or specific algorithms are usually needed.

Identifying All Relevant Costs: The APR Ingredients

To understand your APR, the first practical step is to identify all the costs associated with your loan.

- Stated Interest Rate: This is the base percentage.

- Loan Term: The duration in months.

- Principal Amount: The amount you are borrowing.

- All Lender-Imposed Fees: Scrutinize your loan estimate or disclosures for items like:

- Origination fee

- Documentation fee (if charged by the lender, not the dealer)

- Underwriting fee

- Credit check fee (if separate from application)

- Any other mandatory charges from the lender required to get the loan.

Important Note: Sales tax, registration fees, extended warranty costs, and dealership preparation fees are typically not included in the APR calculation, even if they are rolled into your total loan amount. While financing these items increases your total principal and thus the overall interest paid, they are not considered part of the lender’s cost of funds or administrative fees for the purpose of APR.

Leveraging Online APR Calculators: Your Best Bet

For most consumers, the most effective and reliable way to “calculate” or determine a potential APR is by using online loan calculators that include fields for fees. Many reputable financial websites, bank lending pages, and consumer advocacy sites offer such tools.

How to use them:

- Input Principal Loan Amount: The amount you wish to borrow.

- Enter Stated Interest Rate: The rate quoted by the lender.

- Specify Loan Term: The number of months.

- Input All Lender-Imposed Fees: Crucially, enter the dollar amount of all applicable fees that would be included in the APR.

The calculator will then provide you with an estimated APR. This allows you to model different scenarios and compare offers by seeing how various fees impact the final rate. This method is far more practical than attempting a manual calculation.

Understanding Lender Disclosures: The Official APR

The most direct and accurate source for your loan’s APR is the lender itself. Under the Truth in Lending Act (TILA), lenders are legally obligated to disclose the APR to you before you sign a loan agreement. This disclosure ensures transparency and allows you to make an informed decision.

Where to find it:

- Loan Estimate: Before committing, lenders provide a loan estimate document, which clearly states the APR.

- Loan Agreement/Promissory Note: The final loan documents you sign will also prominently display the APR.

Always compare the APR disclosed by the lender with any estimates you’ve generated using online calculators. Significant discrepancies should prompt further questions to your lender. The legally disclosed APR is the official rate you will be charged, encompassing all qualifying lender fees.

The Impact of APR on Your Car Loan

The APR is more than just a number; it’s a powerful indicator of the true financial burden of your car loan. A seemingly small difference in APR can translate into hundreds or even thousands of dollars over the loan’s lifetime.

Total Cost of Ownership

A higher APR directly translates to a higher total cost of ownership for your vehicle, beyond its purchase price. This is because every percentage point increase in APR means you’re paying more in interest and fees annually on the outstanding principal. Over several years, this accumulates significantly.

- Example: On a $25,000 loan over 60 months:

- At 5% APR, your total cost might be around $28,300.

- At 7% APR, your total cost could jump to approximately $30,000.

- That 2% difference in APR results in nearly $1,700 more paid over five years.

Monthly Payment Implications

While the loan term primarily dictates your monthly payment, the APR plays a substantial role too. A higher APR will increase your monthly payment for the same principal and term, or necessitate a longer term to achieve a similar monthly payment, which further increases the total interest paid. Understanding this link helps you determine if a particular loan is truly affordable within your budget.

Comparison Shopping: APR as the Ultimate Metric

This is arguably the most critical impact of understanding APR. When shopping for a car loan, you will likely receive offers from multiple lenders – banks, credit unions, and dealership financing. Each might present a different interest rate and a unique set of fees. Trying to compare them based solely on interest rates or monthly payments is like comparing apples and oranges.

The APR standardizes these comparisons. It is the single best metric for evaluating which loan offer is genuinely the most economical. Always ask for the APR from every lender, and use it as your primary tool for comparison. The offer with the lowest APR is almost always the cheapest option overall, provided all other terms (like loan term and principal) are equal.

Refinancing Considerations

Knowing the impact of APR is also crucial if you consider refinancing your car loan. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower APR. If your credit score has improved since you first took out the loan, or if market rates have dropped, refinancing to a lower APR can significantly reduce your monthly payments and the total amount you pay over the remaining life of the loan. Conversely, if the new APR isn’t significantly lower, the costs associated with refinancing might outweigh the benefits.

Tools and Resources for APR Management

While manual calculation of APR for installment loans is notoriously complex, a wealth of tools and resources are available to help you understand, compare, and manage your car loan’s APR effectively. Leveraging these can empower you to make savvy financial decisions.

Online APR Calculators

As discussed, online calculators are indispensable. They are readily available on:

- Bank and Credit Union Websites: Many financial institutions offer their own calculators, which can be useful even if you don’t plan to borrow from them.

- Financial News & Advice Sites: Reputable sites like Bankrate, NerdWallet, or Investopedia often feature robust loan calculators that allow you to input various fees to see their impact on APR.

- Consumer Finance Portals: Government-backed or non-profit consumer sites might also offer unbiased tools.

When using these, ensure they allow you to input both the interest rate and any specific lender fees, as this is critical for an accurate APR estimate.

Loan Amortization Schedules

An amortization schedule is a table detailing each payment made over the life of a loan. It breaks down how much of each payment goes towards interest and how much goes towards the principal balance. While it doesn’t directly show APR, it illustrates the cost structure of your loan and how interest accrues. Many online calculators can generate amortization schedules, helping you visualize the long-term impact of your APR and payments. Understanding how your principal reduces over time, and how interest is calculated on the declining balance, reinforces the importance of a lower APR.

Lender Disclosures: The Truth in Lending Act (TILA)

The Truth in Lending Act (TILA) is a federal law designed to protect consumers in credit transactions. A key provision of TILA requires lenders to disclose the APR prominently and clearly before you finalize a loan. This legal mandate ensures transparency.

- Your Rights: Always look for the APR on your loan estimate and final loan documents. If a lender is hesitant to provide it or makes it difficult to find, consider it a red flag.

- Official Source: The APR stated on your official loan documents is the legally binding rate you’re being charged, inclusive of all TILA-mandated fees. Use this as your definitive number for comparison.

Financial Advisors and Credit Counselors

For complex financial situations or if you simply prefer professional guidance, a financial advisor or credit counselor can be an invaluable resource. They can help you:

- Understand Loan Terms: Break down confusing jargon and ensure you fully grasp all aspects of your loan.

- Compare Offers: Provide an expert opinion on different loan proposals, helping you identify the best deal based on your financial situation.

- Budgeting: Integrate your car loan payments into a broader financial plan.

- Refinancing Advice: Advise on whether refinancing is a sound strategy for your current loan.

While there might be a cost associated with these services, the long-term savings from securing a better APR could easily outweigh the initial expense.

In conclusion, knowing “how to calculate APR on car loan” isn’t about mastering complex formulas, but rather about understanding its components, appreciating its critical role in comparison shopping, and knowing how to access and interpret the correct information. By focusing on the APR, you equip yourself with the most powerful tool for navigating the world of car financing, ensuring you drive away with a deal that truly benefits your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.