For decades, the S&P 500 has been heralded as the “gold standard” for measuring the health of the United States economy and the primary vehicle for long-term wealth creation. Often referred to by financial experts as the single most effective tool for the average investor, the S&P 500 index fund offers a blend of simplicity, low cost, and historical reliability. Whether you are a seasoned investor or a complete novice, understanding how to navigate the process of buying an S&P 500 index fund is a foundational step toward financial independence.

In this guide, we will break down the mechanics of the S&P 500, provide a technical roadmap for purchasing your first shares, and explore the strategic nuances that separate successful long-term investors from those who succumb to market volatility.

Understanding the S&P 500 Index Fund

Before clicking the “buy” button, it is essential to understand exactly what you are purchasing. An index fund is not a single company; rather, it is a basket of stocks designed to mimic the performance of a specific financial market index.

What is the S&P 500?

The Standard & Poor’s 500, or S&P 500, is a stock market index that tracks the performance of 500 of the largest publicly traded companies in the United States. These companies span across all sectors—technology, healthcare, consumer discretionary, energy, and finance. Because the index is market-capitalization-weighted, larger companies like Apple, Microsoft, and Amazon have a more significant impact on the index’s movement than smaller constituents. When you buy an S&P 500 index fund, you are essentially buying a small piece of the 500 most powerful corporations in America.

The Philosophy of Passive Investing

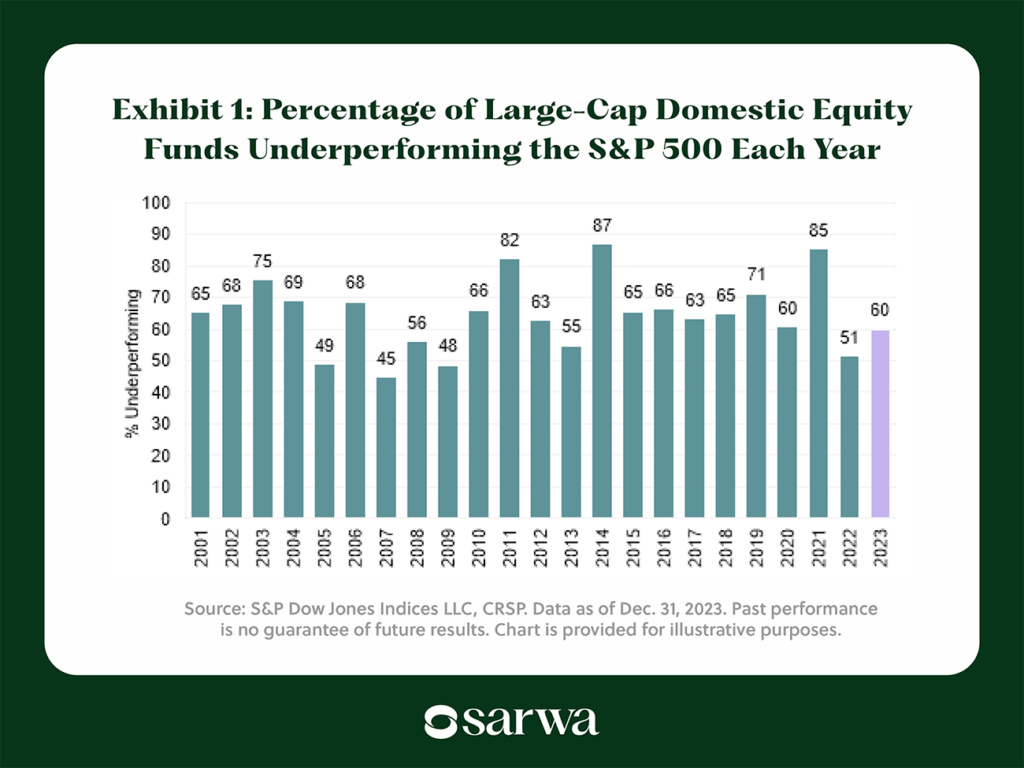

The rise of the index fund is largely credited to John Bogle, the founder of Vanguard, who championed the idea of “passive investing.” The philosophy is simple: rather than paying high fees to a fund manager to “beat the market” (a feat most fail to achieve consistently), you should simply “own the market.” By keeping costs low and maintaining a diversified portfolio, passive investors benefit from the aggregate growth of the US economy over time. Historical data shows that the S&P 500 has provided an average annual return of approximately 10% over the last several decades, making it a formidable tool for compounding wealth.

Step-by-Step Guide: How to Buy Your First Index Fund

Purchasing an index fund is more accessible today than ever before. What once required a phone call to a high-commission broker can now be done in minutes via a smartphone app.

Choosing a Brokerage Platform

The first step is selecting a brokerage. Your choice should depend on your goals and the user experience you prefer.

- Vanguard, Fidelity, and Charles Schwab: These are the “big three” of the indexing world. They offer their own proprietary S&P 500 funds with some of the lowest expense ratios in the industry.

- Modern FinTech Apps: Platforms like Robinhood, Betterment, or M1 Finance offer streamlined interfaces that are excellent for beginners who prefer a mobile-first experience.

- Retirement Accounts: If you have a 401(k) or a 403(b) through your employer, you likely already have access to an S&P 500 index fund within that plan.

Opening and Funding Your Account

Once you have selected a brokerage, you will need to open an account. You will typically choose between a taxable brokerage account (flexible withdrawals) or a tax-advantaged account like a Roth IRA or Traditional IRA (better for long-term retirement savings). After the account is approved, you must link your bank account and transfer the funds you wish to invest. Most modern brokerages allow for “fractional shares,” meaning if you only have $50 to invest, you can still buy a portion of an S&P 500 fund even if the full share price is $400.

Identifying the Right Ticker Symbol (VOO, SPY, IVV)

When you are ready to buy, you will need to search for the specific “ticker symbol” of the fund. While they all track the same 500 companies, they are issued by different institutions.

- VOO (Vanguard S&P 500 ETF): Known for extremely low fees.

- SPY (SPDR S&P 500 ETF Trust): The oldest and most liquid S&P 500 ETF, often used by institutional traders.

- IVV (iShares Core S&P 500 ETF): BlackRock’s highly efficient and low-cost version.

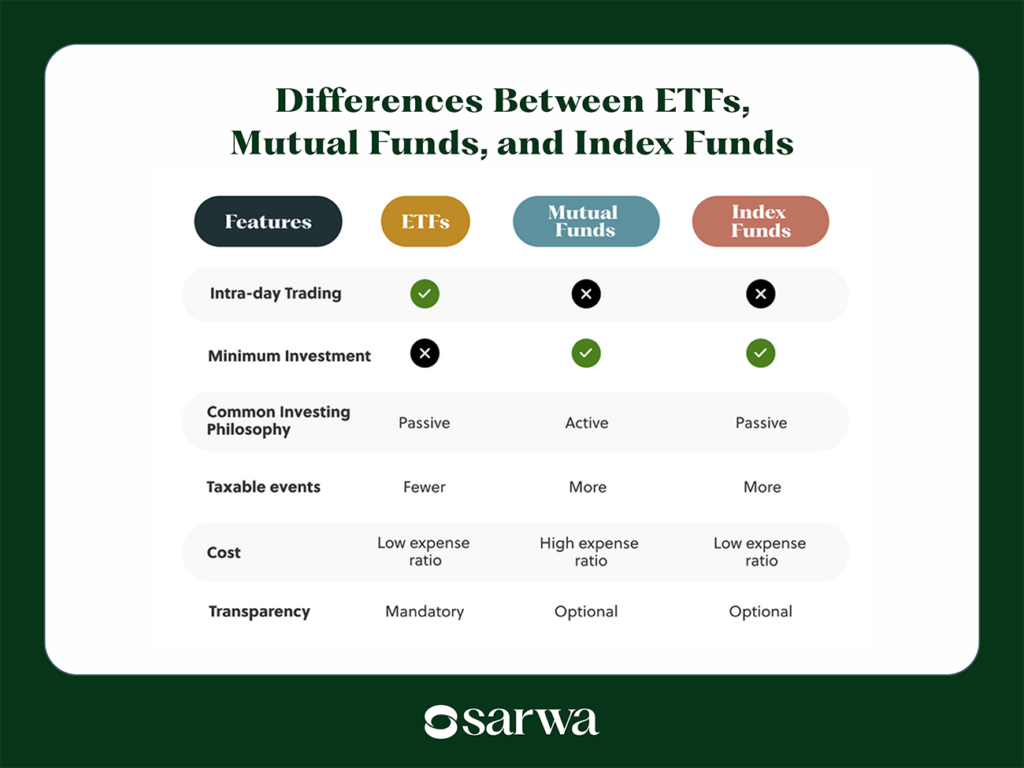

- Mutual Fund vs. ETF: You may also see mutual fund versions like VFIAX (Vanguard). The primary difference is that ETFs trade like stocks throughout the day, while mutual funds only price once at the end of the business day.

Key Factors to Consider Before Investing

While buying an S&P 500 fund is relatively straightforward, the “hidden” details can significantly impact your total returns over twenty or thirty years.

Expense Ratios and Fees

The “expense ratio” is the annual fee that the fund management company charges you to run the fund. It is expressed as a percentage. For example, an expense ratio of 0.03% means you pay $3 for every $10,000 invested. While this seems negligible, a fund with a 1.0% fee—common in actively managed funds—can cost you hundreds of thousands of dollars in lost gains over a lifetime of investing. When buying an S&P 500 index fund, always look for the lowest possible expense ratio.

Dividend Reinvestment Plans (DRIP)

Most companies in the S&P 500 pay dividends—a portion of their profits distributed to shareholders. When you own an index fund, you receive these dividends. To maximize growth, you should enable a “Dividend Reinvestment Plan” (DRIP) within your brokerage account. This automatically uses your dividend payments to buy more shares of the fund. This creates a powerful feedback loop where you earn “interest on your interest,” accelerating the compounding process.

Tax-Advantaged vs. Taxable Accounts

Where you hold your index fund matters for your tax bill. In a taxable brokerage account, you may owe capital gains taxes when you sell for a profit. In a Roth IRA, your investments grow tax-free, and withdrawals in retirement are also tax-free. If you are investing for the long term (10+ years), utilizing tax-advantaged accounts should be your priority to ensure you keep the maximum amount of your earnings.

Long-Term Strategies for S&P 500 Success

Investing in the S&P 500 is not a “get rich quick” scheme; it is a “get wealthy slowly” strategy. Success requires a disciplined approach to market psychology.

Dollar-Cost Averaging (DCA)

One of the biggest mistakes new investors make is trying to “time the market”—waiting for a “dip” to buy. Unfortunately, even the professionals rarely time the market correctly. A more effective strategy is Dollar-Cost Averaging (DCA). This involves investing a fixed amount of money at regular intervals (e.g., $500 every month), regardless of whether the market is up or down. When prices are high, your $500 buys fewer shares; when prices are low, your $500 buys more. Over time, this lowers your average cost per share and removes the emotional stress of watching daily price fluctuations.

Managing Risk and Market Volatility

The S&P 500 is historically resilient, but it is not a straight line up. It has experienced significant “drawdowns,” such as the 2008 financial crisis and the 2020 pandemic crash. During these times, the value of your portfolio may drop by 20% or even 50%. The key to S&P 500 investing is the “time in the market.” Historically, every single downturn in the S&P 500 has eventually ended in a new all-time high. Investors who panic-sell during a crash lock in their losses, while those who stay the course (or buy more) reap the rewards of the eventual recovery.

Conclusion: The Power of Consistency

Buying an S&P 500 index fund is perhaps the most democratic financial tool ever created. It allows an individual with $50 to own the same assets as a billionaire. By selecting a low-cost brokerage, choosing a fund with a minimal expense ratio, and committing to a consistent contribution schedule through dollar-cost averaging, you are placing yourself on a proven path to financial security.

The beauty of the S&P 500 lies in its simplicity. You do not need to analyze balance sheets, predict the next tech trend, or watch the news 24/7. You simply need to trust in the collective ingenuity of the world’s largest companies and give your money the most valuable asset of all: time. Start early, stay consistent, and let the power of the 500 do the heavy lifting for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.