In the ecosystem of modern commerce, a business’s creditworthiness is its most silent yet powerful asset. Much like a personal credit score dictates an individual’s ability to secure a mortgage or a favorable interest rate on a car loan, a company’s credit profile determines its capacity to scale, innovate, and weather economic downturns. Building company credit is not merely an administrative task; it is a strategic financial maneuver that separates the personal liabilities of the business owner from the operational obligations of the corporation.

For many entrepreneurs, the journey of building business credit is often misunderstood as simply “getting a credit card.” In reality, it is a multi-layered process that involves legal structuring, meticulous record-keeping, and the cultivation of relationships with vendors and financial institutions. By establishing a robust credit profile, a company gains access to higher loan amounts, lower insurance premiums, and better terms with suppliers—all of which contribute to a healthier bottom line.

Establishing the Legal and Financial Foundations

Before a company can begin reporting its payment history to credit bureaus, it must exist as a distinct legal and financial entity. You cannot build business credit on a foundation that is legally intertwined with your personal finances. The first step in this journey is ensuring the business is recognized by the government and financial institutions as an independent “person.”

Choosing the Right Legal Structure

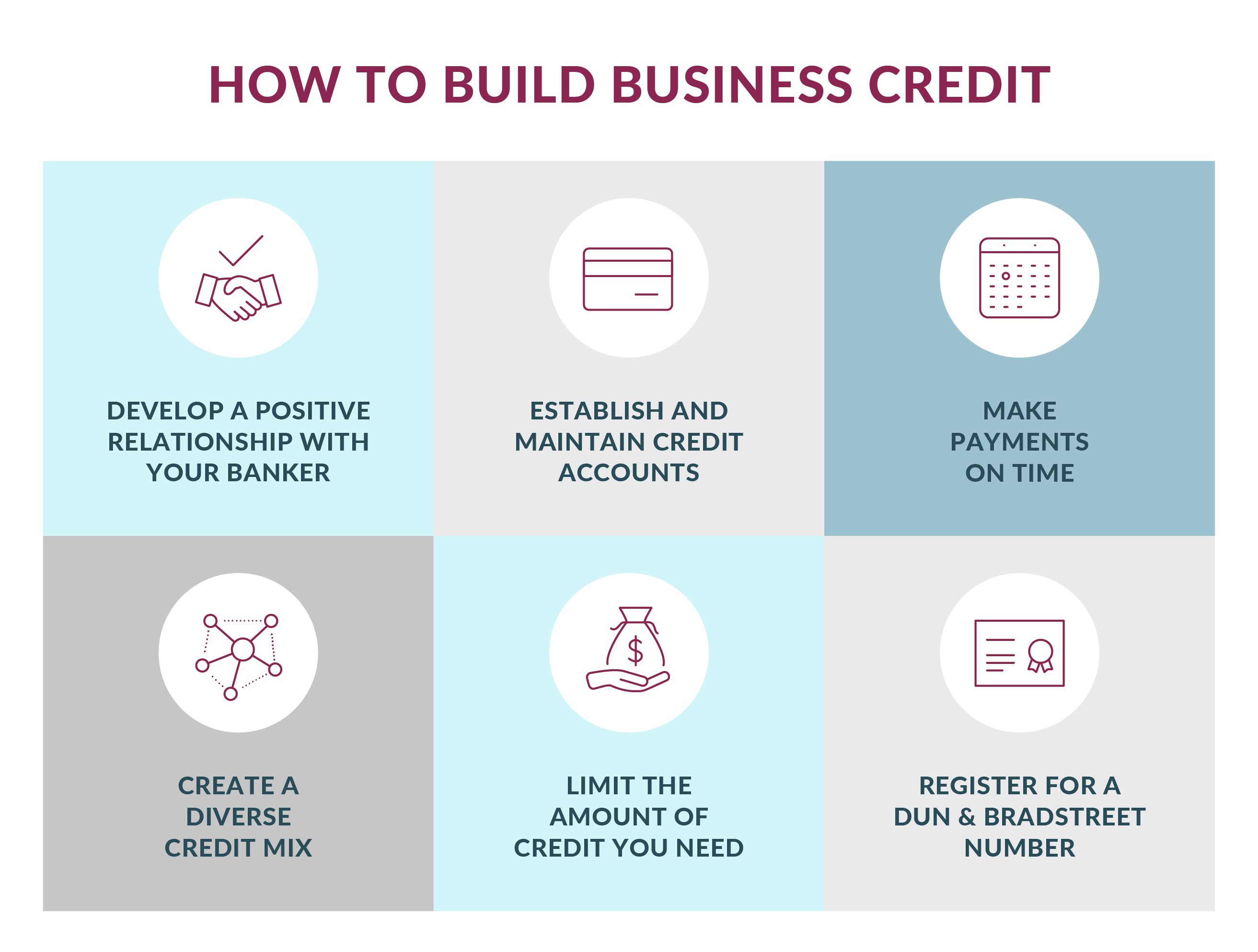

To build company credit, the business must be incorporated. Sole proprietorships and general partnerships often find it difficult to build separate business credit because the law views the owner and the business as the same entity. By forming a Limited Liability Company (LLC), an S-Corp, or a C-Corp, you create a legal “firewall.” This separation is the prerequisite for a business credit score that is independent of your personal Social Security Number.

Obtaining an Employer Identification Number (EIN)

Just as your Social Security Number (SSN) tracks your personal financial history, the Employer Identification Number (EIN) acts as the primary identifier for your business in the eyes of the IRS and credit reporting agencies. Obtaining an EIN is free through the IRS website and is mandatory for opening business bank accounts and applying for most forms of corporate credit. It is the cornerstone upon which your entire credit profile will be built.

Establishing a Professional Financial Presence

Consistency is vital for credit bureaus. To appear as a legitimate, credit-worthy entity, your business must have a dedicated physical address (not a P.O. Box), a dedicated business phone line listed in the 411 directory, and a professional website and email address. Most importantly, you must open a business checking account. Using a personal bank account for business transactions—a practice known as “commingling”—is one of the fastest ways to jeopardize your corporate veil and hinder your ability to build professional credit.

Navigating Business Credit Reporting Agencies

Unlike personal credit, which is dominated by the “Big Three” (Equifax, Experian, and TransUnion) and the FICO score, business credit operates under a different set of rules and agencies. Understanding who is watching your business and how they calculate your score is essential for strategic management.

The Significance of the Data Universal Numbering System (DUNS)

Dun & Bradstreet (D&B) is perhaps the most influential business credit bureau globally. To begin your journey with them, you must obtain a DUNS Number. This is a unique nine-digit identification sequence for each physical location of your business. Without a DUNS Number, you essentially do not exist in the D&B database. Many government contractors and large corporate vendors will not even consider a partnership without seeing a DUNS Number on the application.

Understanding the Paydex Score and Intelliscore

The metrics used in business finance differ from personal finance. The D&B Paydex score, for instance, ranges from 1 to 100. A score of 80 is considered excellent and generally signifies that the business pays its bills on time. To achieve a score higher than 80, a company must actually pay its bills before the due date. Similarly, Experian’s Intelliscore Plus uses a highly predictive model to determine the likelihood of a business becoming seriously delinquent. Knowing these benchmarks allows a business owner to target specific behaviors—like early payment—to boost their standing.

Registering with Equifax Business and Experian Business

While D&B is a major player, Experian and Equifax also maintain extensive business databases. These agencies often collect information from different sources, such as public records, legal filings, and small business financial exchanges. It is prudent for a business owner to check their reports with all three major bureaus annually to ensure there are no errors that could lead to a sudden credit squeeze.

Strategic Credit Building through Tiered Tradelines

Once the foundation is set and you are registered with the bureaus, the actual process of “building” begins. You cannot start by asking for a $100,000 unsecured line of credit. Instead, you must climb the “credit ladder” through a series of tiered accounts.

Starting with Tier 1 Vendor Tradelines

The most accessible way to start building credit is through “Net-30” vendors. These are suppliers that allow you to buy products—such as office supplies, shipping materials, or cleaning products—and pay the full invoice within 30 days. The key is to find vendors that report these payments to the major business credit bureaus. By making small, frequent purchases and paying them off immediately, you create a paper trail of reliability that triggers the generation of your first business credit scores.

Leveraging Business Credit Cards for Operational Expenses

Once you have established a few positive tradelines with vendors, you can move toward business credit cards. In the early stages, these may require a personal guarantee (meaning your personal credit is used as a fallback). However, many modern business cards report only to the business credit bureaus, not your personal report, unless you default. Using these cards for recurring expenses like software subscriptions, utility bills, or inventory—and paying them in full each month—demonstrates that your company can handle revolving credit responsibly.

The Critical Role of Payment Velocity

In the world of business finance, “on time” is the bare minimum. To truly accelerate your credit growth, you should focus on “payment velocity”—paying invoices several days or even weeks before they are due. Since business credit scores like the Paydex are heavily weighted toward payment timing, early payments can dramatically increase your score in a shorter timeframe than in the personal credit world.

Managing and Scaling Your Company’s Financial Reputation

Building credit is not a “set it and forget it” task. As your business grows, your financial needs will become more complex, requiring higher limits and more sophisticated financial instruments. Maintaining your credit profile is an ongoing discipline of monitoring and strategic scaling.

Monitoring Credit Reports and Correcting Inaccuracies

Errors on business credit reports are surprisingly common. A vendor might fail to report your payments, or a different company with a similar name might have their debts mistakenly tied to your EIN. Regularly monitoring your reports allows you to catch these discrepancies early. Unlike personal credit, anyone can buy a copy of your business credit report, including competitors, potential partners, and lenders. Ensuring the data is accurate is a matter of protecting your corporate reputation.

Transitioning to Tier 2 and Tier 3 Credit

As your scores improve and your revenue grows, you can move away from simple vendor accounts toward “Tier 2” and “Tier 3” credit. Tier 2 includes retail credit cards (like those for major hardware or electronics stores) with higher limits and no personal guarantee requirements. Tier 3 consists of unsecured bank loans, large-scale equipment leases, and specialized lines of credit. Each step up the ladder provides more capital at a lower cost, which can be reinvested into the business to drive further growth.

Avoiding Common Pitfalls and “Credit Blunders”

The most significant threat to a growing business credit profile is the high credit utilization ratio and late payments. Additionally, business owners should be wary of applying for too many lines of credit in a short period, as excessive hard inquiries can signal financial distress to lenders. Perhaps most importantly, never close old accounts that are in good standing. The “age of credit” is a significant factor in your score; keeping your oldest vendor accounts active demonstrates long-term stability and reliability.

Conclusion: The Competitive Edge of Corporate Credit

Building company credit is a marathon, not a sprint. It requires a disciplined approach to financial management, a keen eye for detail, and a proactive stance toward vendor relationships. However, the rewards for this effort are substantial. A business with a strong credit profile enjoys a level of freedom and flexibility that cash-only businesses do not. It can seize opportunities for expansion, survive lean months without depleting cash reserves, and eventually move toward a state where the business’s financial health is entirely independent of the owner’s personal assets.

By following this roadmap—from legal formation and bureau registration to the strategic use of tiered tradelines—you transform your company from a mere “job” into a robust financial entity. In the modern marketplace, credit is more than just borrowed money; it is a testament to your company’s integrity and a catalyst for its future success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.