In the modern financial landscape, the definition of a “wallet” has undergone a radical transformation. No longer confined to leather bifolds and physical currency, the contemporary consumer manages their capital through a sophisticated ecosystem of digital platforms. Among these, Venmo has emerged as a titan of peer-to-peer (P2P) finance, facilitating billions of dollars in transactions annually. However, to leverage Venmo not just as a payment relay but as a functional financial tool, one must understand the nuances of managing the “Venmo Balance.”

Adding money to your Venmo account is more than a technical necessity; it is a strategic move for managing liquidity, budgeting for social expenses, and ensuring seamless transactions. This guide explores the financial mechanics of funding your Venmo account, the strategic implications of digital cash management, and the security protocols necessary to protect your assets in the fintech era.

The Role of Venmo in Modern Personal Finance

The evolution of financial technology has blurred the lines between traditional banking and daily lifestyle choices. Venmo occupies a unique space in this intersection, acting as a social-financial hybrid. To use it effectively, one must view it as a specialized sub-account within their broader personal finance portfolio.

Bridging the Gap Between Traditional Banking and Fintech

For many, Venmo serves as the “last mile” of financial delivery. While your primary bank account houses your long-term savings and handles major bills, Venmo facilitates the micro-transactions of daily life. By adding money directly to your Venmo balance, you create a dedicated pool of “social capital” that is siloed from your main checking account. This separation is a core principle of modern budgeting, allowing users to allocate specific funds for discretionary spending without risking the integrity of their primary financial reserves.

The Psychology of Digital Liquidity

There is a distinct psychological difference between spending from a credit card and spending from a pre-funded digital balance. When you add money to Venmo, you are effectively practicing a digital version of the “envelope system.” By maintaining a specific balance, you gain immediate visibility into your spending power within that specific ecosystem. This helps prevent the “debit card creep” where small, social transactions accumulate unnoticed on a bank statement, making it difficult to track monthly discretionary outflows.

How to Add Money to Your Venmo Balance: A Strategic Walkthrough

While Venmo allows you to pay people directly using a linked bank account or card, many users prefer to maintain a standing balance. This is particularly useful for those who use the Venmo Debit Card or want to ensure that their payments are instantaneous without waiting for bank processing times.

Verifying Your Identity for Full Functionality

Before you can add funds to your Venmo balance, you must comply with federal financial regulations. Under the USA PATRIOT Act and other “Know Your Customer” (KYC) requirements, Venmo must verify your identity. This typically involves providing your legal name, date of birth, and Social Security Number. From a financial management perspective, this step is crucial as it transitions your account from a basic relay tool to a “Venmo Balance” account, unlocking the ability to hold and manage funds within the app.

The Step-by-Step Funding Process

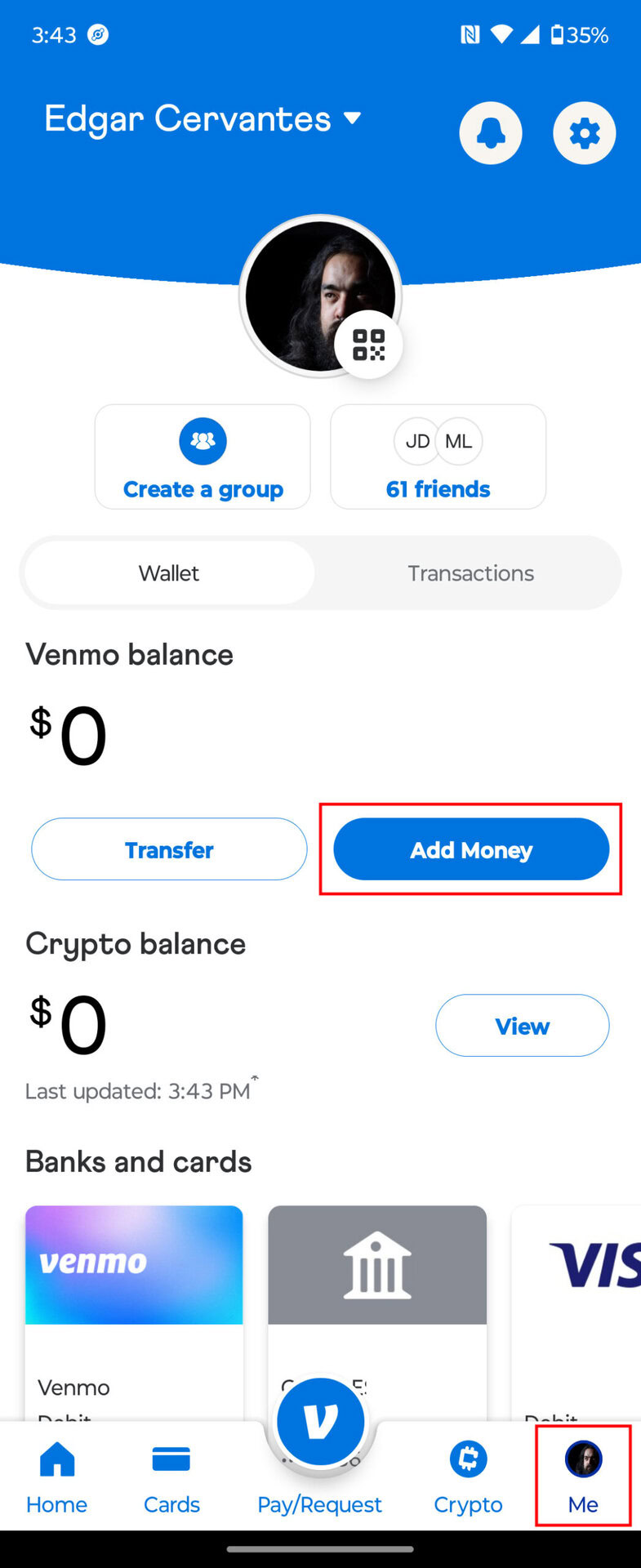

Once your identity is verified, adding money is a straightforward financial transfer. Navigate to the “Me” tab, select the “Manage Balance” or “Add Money” option, and enter the desired amount.

- Source Selection: You must choose a verified bank account as the source. Venmo typically does not allow you to add money to your balance via credit card due to the high risk of cash-advance fees and fraud.

- Confirmation: Review the transfer details. Accuracy is paramount here, as digital transfers, once initiated, are difficult to reverse.

- Wait Times: Standard transfers usually take 3 to 5 business days. This delay is a critical factor to consider when planning your weekly cash flow.

Instant vs. Standard Transfers: The Cost of Velocity

In the world of personal finance, time is often equated with money. Venmo offers “Instant Transfers” for moving money out of the app, but when adding money, you are largely at the mercy of the ACH (Automated Clearing House) system. Understanding the “float”—the time it takes for money to move from your bank to Venmo—is essential for avoiding overdrafts in your primary account. A savvy financial manager plans these transfers well in advance of scheduled social events or bill payments.

Optimizing Your Liquidity: Choosing the Right Funding Source

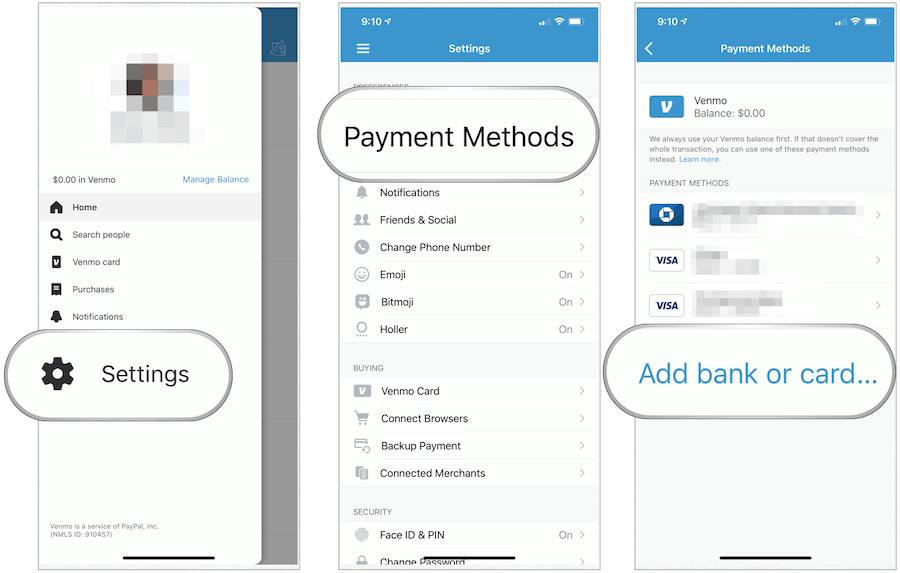

The efficiency of your digital wallet depends heavily on how it is tethered to your traditional financial institutions. Choosing the right source for your Venmo funds involves balancing speed, security, and cost-effectiveness.

The Superiority of Bank Accounts over Debit Cards

While you can link a debit card to Venmo for making payments, adding money to your balance generally requires a direct link to a checking account. This is advantageous for two reasons. First, it avoids the transaction limits often imposed by debit card processors. Second, it creates a cleaner paper trail for your financial records. When you link a bank account via Plaid or manual verification, you are establishing a secure, high-capacity pipeline for your capital.

Managing Transaction Limits and Cash Flow

Venmo imposes limits on how much you can add to your balance and how much you can spend. For most verified users, these limits are generous (often up to $5,000 per rolling week), but they are an important constraint to keep in mind for larger purchases or business-related expenses. Tracking these limits ensures that you are never caught in a situation where your liquidity is frozen due to a platform-enforced cap.

Security Protocols and Financial Safety in Digital Asset Management

As you move significant amounts of money into a digital ecosystem, the stakes for security increase. Protecting your Venmo balance requires a multi-layered approach to digital hygiene and financial oversight.

Protecting Your Balance with Multi-Factor Authentication

Treat your Venmo account with the same level of security as your primary bank account. This means enabling Multi-Factor Authentication (MFA), utilizing biometric locks (FaceID or Fingerprint), and ensuring that your recovery email is secure. Since Venmo balances are often not FDIC-insured in the same way traditional bank accounts are (unless specific conditions are met, such as having a Venmo Debit Card or using Direct Deposit), your first line of defense is your own security settings.

Understanding the Risks of “Digital Cash”

Money held in a Venmo balance is essentially a promise of payment. Unlike a savings account, it does not accrue interest. Therefore, from an investment perspective, it is unwise to keep excessively large sums in your Venmo account for long periods. The “opportunity cost” of having $2,000 sitting in Venmo versus a High-Yield Savings Account (HYSA) can be significant over a year. Use Venmo as a transit hub for your money, not a long-term storage vault.

Integrating Venmo into Your Broader Financial Strategy

To truly master your money, you must view adding funds to Venmo as part of a larger strategic plan. It is not just about moving $50 for dinner; it is about how that $50 fits into your monthly financial objectives.

Using Venmo for Micro-Budgeting

One effective strategy is to “fund” your social life at the beginning of the month. By transferring a set amount—say $300—into your Venmo balance, you create a hard limit for social spending. Once the Venmo balance is zero, your “social budget” for the month is exhausted. This provides a level of discipline that is difficult to maintain when all spending comes from a single, larger pool of money.

The Role of Venmo in the Gig Economy and Side Hustles

For freelancers and those with side hustles, Venmo can act as a secondary accounts receivable department. However, adding money to the account from your personal bank to cover business expenses requires careful bookkeeping. It is essential to categorize these transfers to ensure that you are not complicating your tax situation. Venmo’s “Business Profile” features are designed specifically to help separate personal and professional cash flows, providing more robust reporting tools for the modern entrepreneur.

Conclusion: The Future of Your Digital Capital

Learning how to add money to your Venmo account is a fundamental skill in the modern economy, but doing so with a financial mindset elevates it from a simple task to a strategic advantage. By understanding the mechanics of transfers, the importance of identity verification, and the psychological benefits of segregated budgeting, you can turn Venmo into a powerful ally in your personal finance journey.

As the world continues to move away from physical currency, the ability to fluidly move capital between different digital platforms will become even more critical. Stay proactive, stay secure, and always view your digital balance as a tool to be managed, not just a convenience to be used. Whether you are funding a weekend trip or simply splitting a cup of coffee, the way you handle your digital wallet is a reflection of your overall financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.