In the modern economic landscape, the ability to accept credit card payments is no longer a luxury for small businesses—it is a financial necessity. As consumer behavior shifts increasingly toward a cashless society, a business’s bottom line is directly tied to its ability to facilitate seamless, secure, and diverse payment options. However, for many small business owners, the world of payment processing feels like a labyrinth of hidden fees, complex contracts, and technical jargon.

Understanding how to navigate this financial ecosystem is essential for optimizing cash flow and ensuring long-term profitability. This guide delves into the financial intricacies of credit card processing, offering a strategic roadmap for small businesses to integrate these tools while protecting their margins.

1. The Core Financial Infrastructure: Merchant Accounts vs. Payment Service Providers

Before a single dollar can be processed, a small business must choose the foundational financial structure for its payments. This decision is primarily a choice between two models: a dedicated Merchant Account or a Payment Service Provider (PSP).

Merchant Accounts: The Traditional Financial Partnership

A dedicated merchant account is a specialized business bank account that allows you to accept credit and debit card payments. When a customer pays, the funds are first deposited into this account before being transferred to your regular business checking account.

The primary advantage of a dedicated merchant account is stability and customization. Because the bank performs a deep underwriting process on your business before opening the account, there is a lower risk of sudden fund freezes or account terminations. For businesses with high monthly volumes—typically exceeding $20,000—a dedicated merchant account often offers lower transaction rates through negotiated contracts.

Payment Service Providers (PSPs): Simplified Entry

For startups and smaller enterprises, Payment Service Providers like Square, Stripe, or PayPal are often the most accessible entry point. Unlike merchant accounts, PSPs aggregate thousands of small businesses into a single, massive merchant account.

The financial benefit here is the lack of monthly fees and the speed of setup. You can often begin accepting payments within minutes. However, the trade-off is “flat-rate” pricing, which can be more expensive as your volume grows, and a higher risk of account “holds” if the PSP detects unusual activity, as they do not perform comprehensive underwriting upfront.

Assessing Your Business’s Financial Scale

Choosing between these two requires a careful audit of your projected sales. If your business is seasonal or has low volume, the “pay-as-you-go” model of a PSP is financially superior. If you are a high-growth company with consistent, high-ticket transactions, the lower per-transaction cost of a dedicated merchant account will save thousands of dollars in the long run.

2. Decoding the Cost: Understanding Fee Structures and Pricing Models

The most daunting aspect of credit card processing is the fee structure. To maintain healthy profit margins, business owners must look past the “sticker price” and understand how the money is actually divided between the card-issuing bank, the card network (Visa/Mastercard), and the processor.

Interchange-Plus Pricing: The Transparent Choice

Interchange-plus is widely considered the most transparent and cost-effective pricing model for businesses. “Interchange” refers to the non-negotiable fee set by card networks (e.g., 1.8% + $0.10). The “Plus” is the markup charged by your processor.

By using this model, you see exactly what the bank takes and what your processor takes. When interchange rates drop for certain card types (like debit cards), those savings are passed directly to you. This is highly recommended for businesses that want a granular view of their financial outflows.

Flat-Rate and Tiered Pricing Models

Flat-rate pricing charges a fixed percentage for every transaction, regardless of the card type. While this makes bookkeeping incredibly simple (e.g., you know 2.9% is gone from every sale), it is often the most expensive option because the processor sets the rate high enough to cover their most expensive rewards cards.

Tiered pricing, on the other hand, categorizes transactions into “qualified,” “mid-qualified,” and “non-qualified.” While it may look cheap at first glance (advertising low “qualified” rates), most modern rewards and business cards fall into the “non-qualified” tier, resulting in much higher fees than anticipated.

Hidden Costs and Equipment Fees

Beyond transaction fees, small businesses must account for peripheral financial drains. These include:

- Statement Fees: Monthly charges for paper or digital reports.

- PCI Compliance Fees: Charges to ensure your system meets security standards.

- Hardware Leases: Many processors try to lease equipment to small businesses. Financially, it is almost always better to purchase POS hardware upfront rather than entering a multi-year lease that ends up costing five times the retail value of the device.

3. Financial Logistics: In-Person vs. Digital Transactions

How you accept a payment significantly impacts the transaction cost. In the financial world, risk equals cost. The more “verified” a transaction is, the lower the fee.

Point-of-Sale (POS) Systems and In-Person Efficiency

In-person transactions, known as “Card-Present” (CP) transactions, carry the lowest fees. This is because the physical presence of the card and the use of EMV chip technology or NFC (contactless) payments significantly reduce the risk of fraud.

From a financial management perspective, a modern POS system does more than just swipe cards; it integrates with your accounting software. For a small business, this automation reduces the labor costs associated with manual bookkeeping and ensures that inventory levels are updated in real-time, preventing the financial strain of overstocking or stockouts.

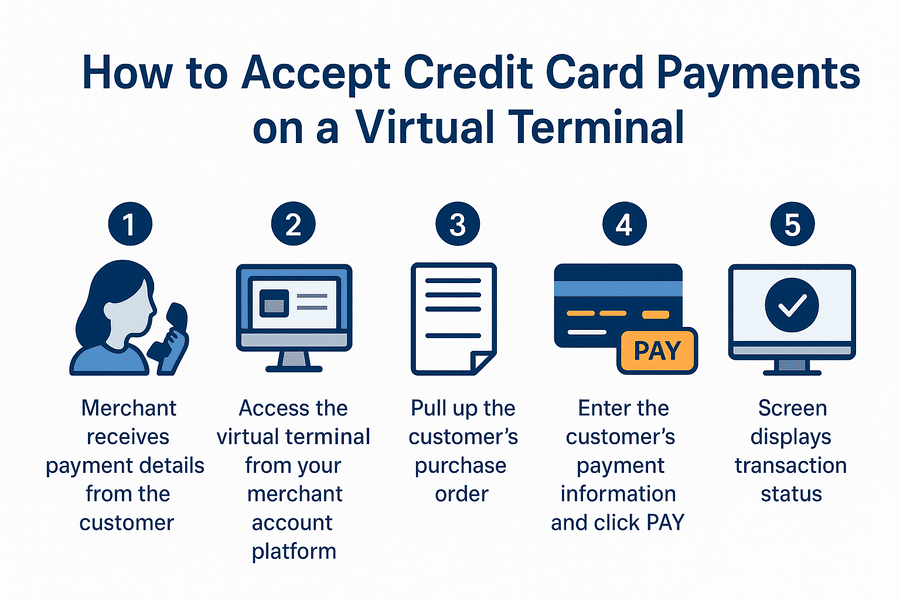

E-commerce Gateways and Virtual Terminals

When a customer buys online or over the phone, it is a “Card-Not-Present” (CNP) transaction. Because the risk of fraud is higher, processors charge a premium for these sales. Small businesses operating online must factor these higher percentages (often 0.5% to 1% higher than CP) into their product pricing.

Virtual terminals allow you to turn your computer into a credit card terminal to take payments over the phone. While convenient for service-based businesses (like consultants or contractors), these should be used judiciously due to the higher fee structure.

Mobile Payments and Contactless Growth

The rise of mobile wallets like Apple Pay and Google Pay has streamlined the financial exchange. These use “tokenization,” which means the customer’s actual card number is never shared with the merchant. From a financial perspective, this reduces your “scope” for PCI compliance, potentially lowering your security-related overhead and protecting you from the massive financial fallout of a data breach.

4. Protecting Your Bottom Line: Chargebacks and Security

Accepting credit cards introduces specific financial risks that can erode profits if not managed proactively. The two primary threats are chargebacks and data insecurity.

The Financial Impact of Chargebacks

A chargeback occurs when a customer disputes a transaction with their bank rather than seeking a refund from the merchant. For the small business, this is a double financial blow: you lose the sale amount, and the processor hits you with a chargeback fee (ranging from $15 to $100).

To protect your business finance, you must have clear refund policies and use robust tracking for shipped goods. High chargeback rates can lead to your merchant account being flagged or terminated, forcing you into “high-risk” processing categories where fees are exorbitant.

PCI Compliance and Financial Liability

The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements designed to ensure that all companies that process, store, or transmit credit card information maintain a secure environment. Failing to maintain compliance can result in monthly fines from your processor and, in the event of a breach, catastrophic financial liability.

Small businesses should look for “PCI-compliant” hardware and software providers who handle the brunt of the security burden. By shifting the data storage to a secure third-party vault (a feature offered by most modern PSPs), you minimize your financial exposure.

Fraud Prevention as a Cost-Saving Strategy

Investing in fraud prevention tools—such as Address Verification Services (AVS) and Card Verification Value (CVV) checks—is a smart financial move. While these might add a few seconds to the checkout process, the money saved by preventing a single fraudulent transaction (and the subsequent chargeback) far outweighs the minor friction.

Conclusion: Strategic Financial Empowerment

Accepting credit card payments is more than a technical setup; it is a core component of a small business’s financial strategy. By choosing the right provider, understanding the nuances of interchange fees, and implementing rigorous security measures, a business owner can significantly reduce overhead and improve the customer experience.

The key to financial success in payment processing lies in transparency and regular auditing. As your business grows, revisit your processing statements. What worked for a startup making $2,000 a month will not be the most cost-effective solution for a business making $50,000 a month. By staying informed and proactive, you ensure that your payment systems serve as a catalyst for growth rather than a drain on your resources. In the end, every fraction of a percentage saved in processing fees is a direct contribution to your business’s net profit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.