The journey to financial independence often begins with a single, crucial step: understanding how your money can work for you. For many, the concept of investing seems daunting, a realm reserved for the wealthy or finance professionals. Yet, at its core, one of the most powerful tools available to everyone, regardless of their starting capital, is compound interest. The question “how much would $1000 invested with compound interest be worth?” isn’t just a mathematical exercise; it’s an exploration into the potential of even a modest initial investment to transform your financial trajectory.

In this article, we’ll demystify compound interest, illustrate its incredible power with practical examples, and guide you on how to leverage it to build wealth, starting with that foundational $1000. Whether you’re a seasoned investor or just embarking on your financial journey, grasping the mechanics of compounding is fundamental to securing a prosperous future.

The Magic Behind Compound Interest: Understanding the Basics

Albert Einstein is often (apocryphally) quoted as calling compound interest the “eighth wonder of the world,” stating, “He who understands it, earns it; he who doesn’t, pays it.” While the exact quote’s origin is debated, its sentiment perfectly captures the transformative power of this financial principle. But what exactly is compound interest, and how does it differ from its simpler counterpart?

Simple vs. Compound Interest: A Fundamental Distinction

To appreciate compound interest, it’s essential to first understand simple interest. Simple interest is calculated only on the principal amount of an investment or loan. If you invest $1000 at a 5% simple interest rate for 10 years, you’d earn $50 per year, totaling $500 in interest over the decade. Your original $1000 would grow to $1500.

Compound interest, however, is a game-changer. It’s interest calculated on the initial principal and also on the accumulated interest from previous periods. In essence, your interest starts earning interest. This exponential growth is what makes it so powerful. Imagine that same $1000 at a 5% compound interest rate. In the first year, you earn $50. But in the second year, you earn 5% not on $1000, but on $1050, and so on. This continuous cycle of growth accelerating growth is the core principle of wealth building.

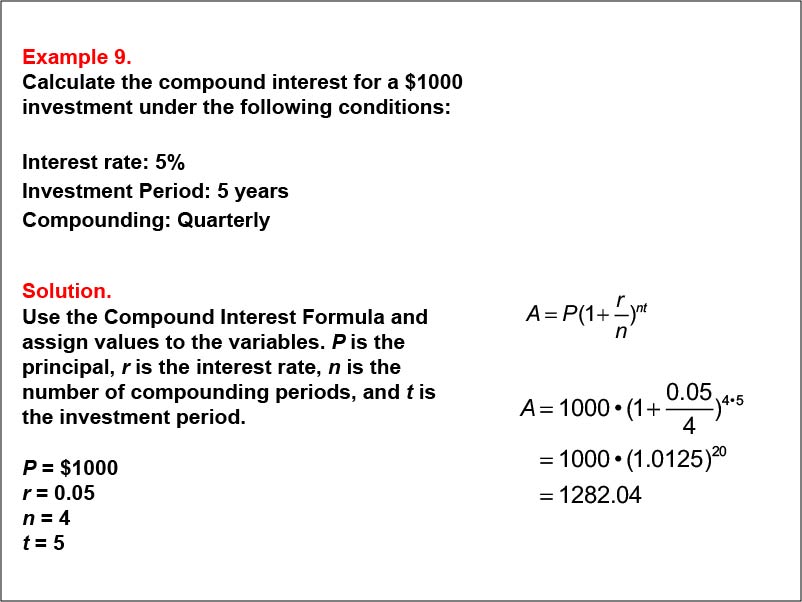

The Compound Interest Formula Explained

While you don’t need to be a math wizard to benefit from compound interest, understanding its formula can provide clarity:

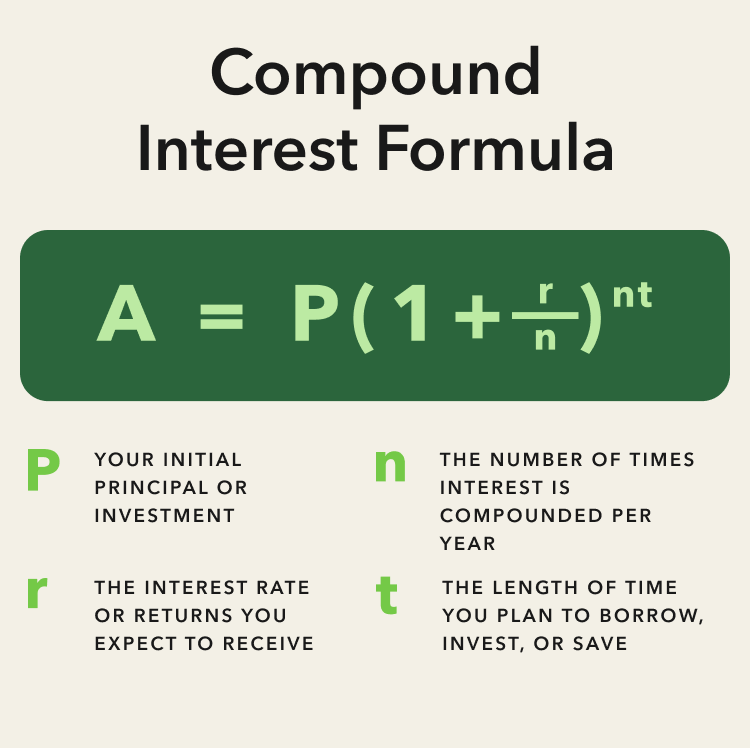

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (your initial $1000)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

This formula beautifully illustrates how time (t), interest rate (r), and compounding frequency (n) work together to amplify your principal. The higher the rate, the longer the time, and the more frequent the compounding, the greater your “A” will be.

Why Compound Interest is Called the “Eighth Wonder of the World”

The “eighth wonder” moniker isn’t hyperbole. Compound interest leverages time and patience to create substantial wealth from modest beginnings. It’s why starting early, even with a small amount like $1000, is far more advantageous than starting later with a larger sum. The earlier your money begins compounding, the longer it has to multiply itself, creating a snowball effect that gains momentum over decades. This principle is at the heart of nearly every successful long-term investment strategy.

Key Factors Influencing Your $1000 Investment’s Growth

When you invest $1000 with compound interest, its ultimate value isn’t predetermined. Several critical factors come into play, each significantly impacting the final sum. Understanding these variables allows you to make informed decisions and optimize your investment strategy.

The Enormous Impact of Time

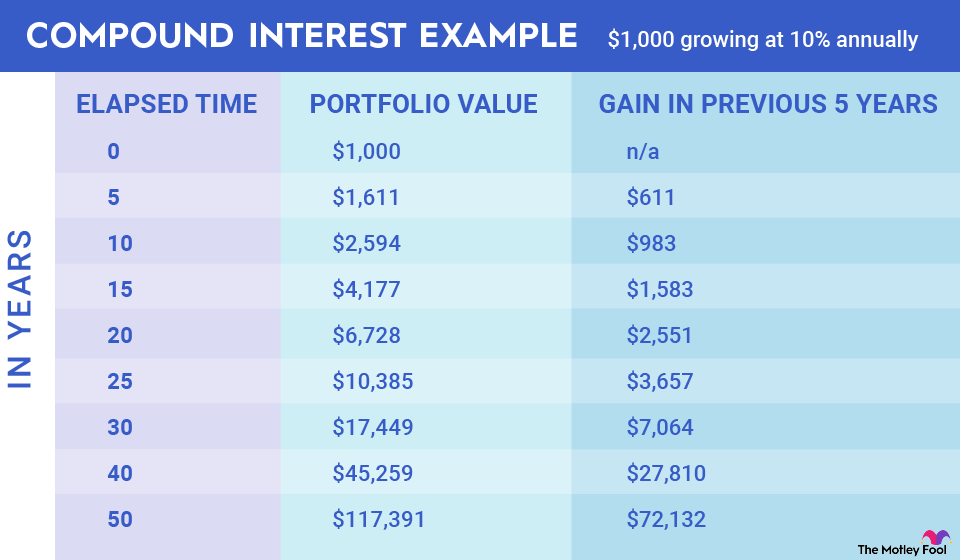

Time is arguably the most powerful ally of compound interest. The longer your money has to grow, the more pronounced the compounding effect becomes. Let’s look at an illustrative example with our $1000, assuming an annual compound interest rate of 7% (a reasonable historical average for stock market returns):

- After 5 years: Your $1000 would grow to approximately $1,402.55

- After 10 years: Your $1000 would grow to approximately $1,967.15

- After 20 years: Your $1000 would grow to approximately $3,869.68

- After 30 years: Your $1000 would grow to approximately $7,612.26

Notice how the growth accelerates dramatically in the later decades. The initial $400 increase over the first five years pales in comparison to the almost $3,750 increase from year 20 to year 30. This exponential curve underscores the irreplaceable value of starting early and letting time do its work.

The Role of the Interest Rate (Annual Return)

While time provides the runway, the interest rate dictates the speed of your aircraft. A higher annual return means your money compounds more rapidly. Let’s see how different rates impact our $1000 investment over 30 years:

- At 3% annual compound interest: Your $1000 would grow to approximately $2,427.26

- At 7% annual compound interest: Your $1000 would grow to approximately $7,612.26

- At 10% annual compound interest: Your $1000 would grow to approximately $17,449.40

The difference between a 3% and a 10% return over 30 years is staggering, highlighting why choosing investments with a reasonable return potential is crucial. It also explains why simply letting money sit in a low-interest savings account (often less than 1%) won’t generate significant wealth over time.

Frequency of Compounding: More Frequent, More Growth

The “n” in our compound interest formula represents the frequency of compounding. Interest can be compounded annually, semi-annually, quarterly, monthly, daily, or even continuously. The more frequently interest is calculated and added back to the principal, the faster your investment grows, albeit often by smaller margins for modest rates.

For instance, $1000 at 7% interest over 30 years:

- Compounded Annually: $7,612.26

- Compounded Monthly: $7,698.66

- Compounded Daily: $7,710.02

While the difference between annual and daily compounding might seem small for a $1000 investment, over long periods and with larger sums, these small increments can add up. Most investment accounts compound monthly or quarterly, offering a good balance.

Where to Invest Your First $1000 for Compound Growth

Knowing the theory of compound interest is one thing; putting it into practice is another. The good news is that there are numerous accessible avenues to invest your first $1000 and harness the power of compounding. The best choice depends on your financial goals, risk tolerance, and time horizon.

High-Yield Savings Accounts (HYSAs) & Certificates of Deposit (CDs)

For those prioritizing safety and liquidity, HYSAs and CDs are excellent starting points. They offer interest rates significantly higher than traditional savings accounts, often between 3-5% (depending on market conditions).

- HYSAs: Offer flexibility, allowing you to deposit and withdraw money easily while earning compound interest. Ideal for emergency funds or short-term savings goals.

- CDs: Require you to lock up your money for a fixed period (e.g., 6 months, 1 year, 5 years) in exchange for a slightly higher, guaranteed interest rate. Great for money you won’t need immediate access to.

While returns here are modest compared to the stock market, they offer a secure way to let your money grow without risk of principal loss.

Low-Cost Index Funds & ETFs

For long-term wealth building, especially if you have a time horizon of 5 years or more, low-cost index funds and Exchange Traded Funds (ETFs) are often recommended. These funds hold a diversified basket of stocks or bonds, giving you exposure to the broader market without needing to pick individual companies.

- Index Funds: Track a specific market index (e.g., S&P 500), offering diversification and market-average returns. They inherently compound returns as the underlying companies grow and reinvest profits.

- ETFs: Similar to index funds but trade like stocks. You can buy fractional shares with your $1000, immediately diversifying your investment.

These options typically offer annual returns in the 7-10% range over long periods, making them ideal for leveraging compound interest for substantial growth. Many brokerage firms allow you to invest with as little as $100 or less to start.

Retirement Accounts (IRAs/401(k)s)

If your goal is retirement, directing your $1000 into a tax-advantaged retirement account is one of the smartest moves you can make.

- Traditional IRA: Contributions might be tax-deductible, and your investments grow tax-deferred until retirement.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are entirely tax-free.

Both IRAs allow you to invest in a wide range of assets, including index funds and ETFs, meaning your money compounds tax-free or tax-deferred for decades. Many brokerages allow you to open an IRA with $0 or a minimal deposit, making your $1000 an excellent starting point. If your employer offers a 401(k) with a matching contribution, that’s often the absolute best place to start, as you’re getting “free money” alongside the power of compounding.

Robo-Advisors

For beginners who want a hands-off approach, robo-advisors like Betterment or Wealthfront are excellent options. You answer a few questions about your risk tolerance and goals, and the robo-advisor creates and manages a diversified portfolio of ETFs for you. They automatically rebalance your portfolio and reinvest dividends, maximizing the compounding effect. Many robo-advisors have low or no minimums, making them perfect for investing your first $1000.

Maximizing the Power of Your $1000 Investment and Beyond

Investing your initial $1000 is a fantastic first step, but truly maximizing the power of compound interest involves more than just setting it and forgetting it. It requires consistency, patience, and a few strategic habits.

Consistency is Key: The Power of Regular Contributions

While $1000 can grow significantly, its potential skyrockets when you add to it consistently. Even small, regular contributions, like an extra $50 or $100 each month, dramatically accelerate the compounding process. This is known as dollar-cost averaging, where you invest a fixed amount regularly, regardless of market fluctuations. Over time, this strategy averages out your purchase price and ensures your portfolio is continually growing and compounding.

Starting Early: The Ultimate Advantage

We’ve touched on this, but it bears repeating: time is your greatest asset. The earlier you start, the less you need to save to reach your financial goals. A 25-year-old investing $1000 today will likely see a much larger return by retirement than a 45-year-old investing the same amount, even if the latter adds more later. The “lost” compounding years can never be regained.

Reinvesting Returns

Ensure that any dividends, interest, or capital gains generated by your investments are automatically reinvested. If you take the income out, you interrupt the compounding cycle. Most investment platforms offer the option to automatically reinvest, ensuring your earnings are put back to work to generate even more earnings.

Diversification and Risk Management

While compound interest is powerful, no investment is without risk. Diversifying your $1000 (and subsequent investments) across different asset classes, industries, or geographies helps mitigate risk. If one investment underperforms, others may compensate. With $1000, an index fund or ETF provides instant diversification, reducing the impact of any single company’s poor performance.

Financial Discipline and Patience

Building substantial wealth through compound interest is a marathon, not a sprint. There will be market ups and downs, economic uncertainties, and perhaps times when you’re tempted to withdraw your money. Financial discipline and patience are paramount. Stick to your long-term plan, resist impulsive decisions, and trust in the undeniable power of compounding over decades.

In conclusion, $1000 invested with compound interest can be the seed from which a significant financial future blossoms. Its ultimate worth depends on the interest rate, the compounding frequency, and, most critically, the passage of time. By understanding these principles and taking advantage of accessible investment vehicles, anyone can harness the magic of compound interest to build wealth and achieve their financial aspirations. Your journey to financial freedom starts with that first thousand dollars and the commitment to let it grow.