For millions of Americans, Social Security represents a cornerstone of their financial future, a vital safety net providing income during retirement, disability, and to survivors. Yet, deciphering how much you can expect to receive from this complex system can feel like navigating a labyrinth. Understanding your potential Social Security benefits is not just about a single number; it’s about grasping a dynamic interplay of factors influenced by your work history, earnings, and crucially, your claiming decisions. This article will demystify the process, providing a comprehensive guide to how your Social Security payments are calculated, the critical choices you face, and how to integrate these benefits into a robust retirement plan.

Deconstructing Social Security: Eligibility and Foundations

Before diving into specific payment amounts, it’s essential to understand the fundamental mechanics of Social Security: what it is, who qualifies, and how it’s funded. This foundational knowledge will illuminate why certain factors weigh so heavily on your future benefits.

What is Social Security?

Established in 1935, Social Security is a federal program designed to provide financial protection to retirees, the disabled, and survivors of deceased workers. It operates on a “pay-as-you-go” system, meaning current workers’ contributions largely fund the benefits of current retirees and other beneficiaries. While often thought of solely as a retirement program, its scope is broader, encompassing disability insurance and survivor benefits, offering a crucial layer of security against various life challenges.

Who is Eligible for Benefits?

Eligibility for Social Security benefits is determined by your work history, specifically by earning “credits.” In 2024, you earn one credit for every $1,730 in earnings, up to a maximum of four credits per year. To qualify for most types of benefits, you generally need 40 credits, which translates to 10 years of working and paying Social Security taxes. If you stop working before accumulating 40 credits, your prior earnings remain on your record, and you can earn additional credits later. Spouses and dependents may also be eligible for benefits based on a worker’s record, even if they haven’t earned enough credits themselves.

How Social Security is Funded

Social Security is primarily funded through dedicated payroll taxes, known as Federal Insurance Contributions Act (FICA) taxes. Employees and employers each contribute 6.2% of earnings up to an annual maximum (the “taxable maximum,” which is $168,600 in 2024), for a combined 12.4%. Self-employed individuals pay both halves, totaling 12.4%. These taxes are deposited into two trust funds: the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund. These funds are vital; they hold the assets that pay out current benefits and serve as a reserve for future obligations.

The Variables: What Determines Your Benefit Amount?

Your Social Security benefit isn’t a fixed sum; it’s a personalized calculation influenced by several key variables. Understanding these factors is crucial for projecting your future income and making informed decisions.

Your Earning History: Average Indexed Monthly Earnings (AIME)

The primary driver of your Social Security benefit is your earnings history. The Social Security Administration (SSA) calculates your “Average Indexed Monthly Earnings” (AIME). This involves taking your highest 35 years of earnings, adjusting them for historical wage growth (indexing) to reflect their value in today’s dollars, and then dividing the total by the number of months in those 35 years. If you have fewer than 35 years of earnings, the missing years are counted as zero, which can significantly reduce your AIME.

Once your AIME is determined, the SSA applies a progressive formula with “bend points” to calculate your Primary Insurance Amount (PIA). This formula ensures that lower-income workers receive a higher percentage of their average earnings back as benefits compared to high-income workers, reflecting the program’s social safety net function. For instance, a certain percentage of your earnings up to the first bend point is included, a lower percentage for earnings between the first and second bend points, and an even lower percentage for earnings above the second bend point.

Your Claiming Age: A Pivotal Decision

Perhaps the most significant factor you directly control is when you choose to start receiving benefits. While you can claim as early as age 62, or as late as age 70, your “Full Retirement Age” (FRA) serves as the benchmark. Your FRA is the age at which you are entitled to 100% of your PIA. It depends on your birth year:

- Born 1943-1954: FRA is 66

- Born 1955: FRA is 66 and 2 months

- …

- Born 1960 or later: FRA is 67

Claiming before your FRA results in a permanently reduced monthly benefit, while delaying beyond your FRA (up to age 70) earns you “delayed retirement credits,” permanently increasing your monthly benefit.

Cost-of-Living Adjustments (COLAs)

Social Security benefits are designed to maintain their purchasing power over time through annual Cost-of-Living Adjustments (COLAs). Each year, typically in October, the SSA announces whether benefits will increase based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). These adjustments ensure that your benefits keep pace with inflation, helping to protect retirees from rising living costs.

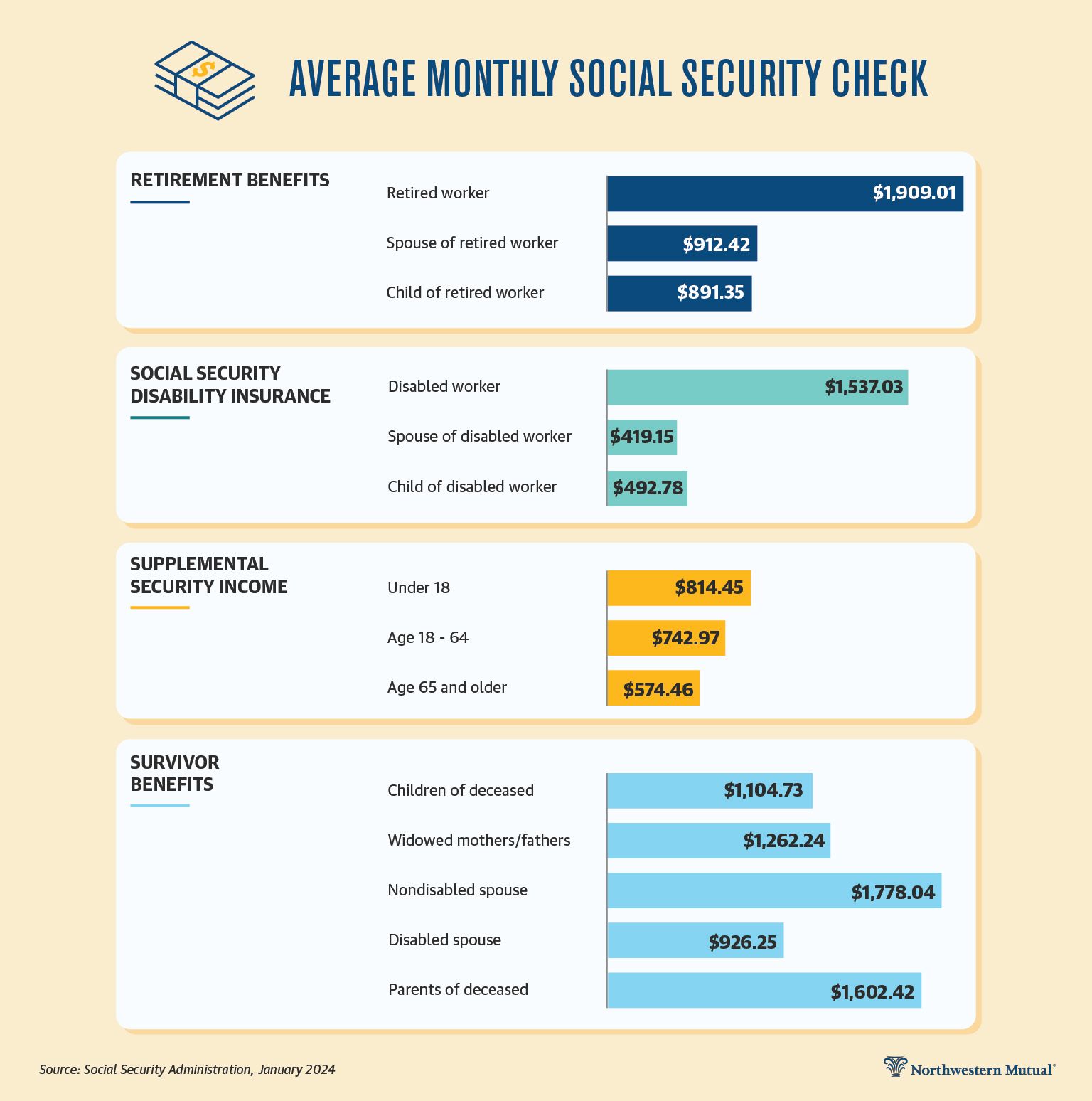

Spousal and Survivor Benefits

Social Security isn’t just for individual workers; it extends to families. If you’re married, divorced (under certain conditions), or widowed, you may be eligible for spousal or survivor benefits based on your current or former spouse’s work record.

- Spousal Benefits: A spouse can receive up to 50% of the working spouse’s FRA benefit, provided they claim at their own FRA. If they claim earlier, the benefit is reduced. Generally, you cannot claim spousal benefits unless the primary earner has already filed for their own benefits (with some exceptions for specific older strategies).

- Survivor Benefits: A widow or widower can receive up to 100% of their deceased spouse’s benefit at their own FRA. Benefits can be claimed as early as age 60 (or 50 if disabled), but they will be reduced.

These family benefits can significantly augment a household’s total Social Security income, especially for those with lower individual earning histories.

Strategic Claiming: Maximizing Your Payout

The decision of when to start receiving Social Security benefits is one of the most impactful financial choices you’ll make in retirement. It involves more than just picking an age; it requires careful consideration of your personal circumstances, health, and financial needs.

Understanding Your Full Retirement Age (FRA)

Your FRA is the pivotal age for Social Security. It’s the age at which you receive your Primary Insurance Amount (PIA) – the benefit calculated based on your earnings record. For anyone born in 1960 or later, your FRA is 67. If you claim exactly at your FRA, there are no reductions or increases; you get 100% of what you’re entitled to. This serves as the baseline for comparing early and delayed claiming options.

The Trade-offs of Early Claiming (Age 62)

You can claim Social Security retirement benefits as early as age 62. However, doing so results in a permanent reduction in your monthly benefit. The reduction is significant: approximately 6.67% per year for the first three years before your FRA, and 5% for each year prior to that. For someone with an FRA of 67, claiming at 62 means a 30% reduction in benefits.

When early claiming might make sense:

- Immediate Financial Need: If you’ve lost your job, have unexpected medical expenses, or need income to cover basic living costs and have no other viable options.

- Poor Health/Shorter Life Expectancy: If you have a serious health condition that suggests a shorter life expectancy, taking benefits earlier could result in a higher total lifetime payout, as you’d receive more payments over fewer years.

- Funding Other Investments: If you have a high confidence in generating superior returns from investments with the early benefits, potentially offsetting the reduction. (This is a more aggressive strategy and carries risk.)

The Benefits of Delayed Claiming (Up to Age 70)

For every year you delay claiming benefits past your FRA, up to age 70, you earn “delayed retirement credits.” These credits permanently increase your monthly benefit by 8% per year. This means someone with an FRA of 67 who delays until age 70 could receive 124% of their PIA. This is a substantial increase that can provide a significant boost to your retirement income, especially in your later years.

When delayed claiming might be advantageous:

- Good Health/Longer Life Expectancy: If you anticipate living a long life, delaying benefits often leads to a higher total lifetime payout, as the increased monthly sum compounds over many years.

- Sufficient Retirement Savings: If you have enough income from other sources (pensions, 401(k)s, IRAs, investments) to cover your living expenses until age 70, delaying Social Security is often a financially savvy move.

- Spousal Considerations: If you are the higher earner in a couple, delaying your benefits can also increase the survivor benefit your spouse would receive if you pass away first.

Considering Spousal and Survivor Benefits Strategically

When one spouse has a significantly higher earnings record, the lower-earning spouse might be better off claiming spousal benefits (up to 50% of the higher earner’s FRA benefit) rather than their own earned benefit. However, the higher earner generally must file for their own benefits first for the spouse to claim.

For widows and widowers, the decision often centers on coordinating their own earned benefit with their survivor benefit. You can potentially claim one benefit (e.g., a reduced survivor benefit) early and switch to your own maximum earned benefit later (e.g., at age 70), or vice versa. The SSA provides guidance on which benefit would be higher and when to claim each to maximize the combined lifetime payout. It’s crucial to explore all options, as the rules can be intricate and specific to your situation.

Planning for the Future: Social Security and Your Retirement

Social Security is a critical component of most retirement plans, but it is rarely the sole source of income. Understanding its role, how to access your information, and its long-term outlook is key to holistic retirement planning.

Accessing Your Social Security Statement

The most direct way to get an estimate of your future benefits is through your Social Security Statement. You can access it online by creating an account at my Social Security (ssa.gov/myaccount). This statement provides:

- An estimate of your retirement benefits at age 62, your Full Retirement Age, and age 70.

- Estimates for disability and survivor benefits.

- A detailed record of your earnings history, which you should review for accuracy.

- Important information about Medicare.

Reviewing this statement annually is a crucial step in monitoring your retirement readiness and ensuring your earnings record is correct.

The Solvency of Social Security

Concerns about the long-term solvency of Social Security are a recurring topic. The annual Trustees’ Report provides projections on the health of the trust funds. While the system is not “going broke,” the report consistently indicates that without congressional action, the trust funds will be able to pay only a reduced percentage of scheduled benefits in the coming decades (e.g., around 80% by the mid-2030s). This is primarily due to demographic shifts, specifically a declining birth rate, increased life expectancy, and the retirement of the large baby boomer generation, which means fewer workers are supporting more retirees.

Potential solutions under discussion include increasing the full retirement age, raising the Social Security payroll tax rate, increasing the taxable maximum earnings limit, or adjusting the benefit formula. While the specific changes are uncertain, it is generally believed that Congress will act to ensure the long-term viability of the program, even if it means some adjustments to benefits or contributions. However, it’s prudent for individuals to factor in some level of uncertainty when relying solely on Social Security projections for their retirement.

Integrating Social Security into Your Overall Retirement Plan

Social Security should be viewed as one leg of a three-legged stool for retirement planning, alongside personal savings (401(k)s, IRAs, brokerage accounts) and pensions (if applicable). It provides a reliable base layer of income, but it’s often not enough to maintain your pre-retirement lifestyle.

Considerations for integration:

- Income Gap Analysis: Project your estimated retirement expenses and compare them to your Social Security benefit. The difference is the “income gap” you’ll need to cover with other savings.

- Longevity Risk: The guaranteed income stream from Social Security is invaluable for protecting against the risk of outliving your other savings. Delaying benefits, if possible, effectively buys you a larger, inflation-adjusted “annuity.”

- Taxation of Benefits: Be aware that a portion of your Social Security benefits may be subject to federal income tax if your “provisional income” (adjusted gross income + tax-exempt interest + 50% of your Social Security benefits) exceeds certain thresholds. Some states also tax Social Security benefits.

Beyond the Numbers: Making an Informed Decision

While calculations and projections are essential, your ultimate Social Security claiming decision should be deeply personal.

- Health and Longevity: Your personal health and family history of longevity are significant factors. If you expect a shorter lifespan, earlier claiming might yield more total benefits.

- Spousal and Dependent Needs: Consider how your decision impacts your spouse’s potential benefits and any eligible dependent children.

- Other Income Sources: The availability of pensions, part-time work, or robust investment income can give you the flexibility to delay Social Security.

- Legacy Goals: Do you want to leave a larger survivor benefit for your spouse?

Consulting with a qualified financial advisor can provide personalized guidance, helping you navigate these complexities and make the most strategic claiming decision for your unique circumstances. Social Security is a powerful financial tool, and understanding how much it will pay you, and how to maximize those payments, is a cornerstone of a secure retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.