For many taxpayers, tax season is met with a mixture of anxiety and anticipation. The primary question on everyone’s mind as they gather their W-2s, 1099s, and receipts is: “How much tax return will I get?” While the term “tax return” actually refers to the forms you file with the IRS, what most people are truly interested in is the tax refund—the amount of overpaid tax returned to them by the government.

Understanding the mechanics behind this calculation is not just about satisfying curiosity; it is a vital component of personal finance management. A refund is essentially an interest-free loan you have provided to the government over the past year. By understanding how this figure is calculated, you can better manage your cash flow, optimize your investment strategies, and ensure you aren’t leaving money on the table.

Understanding the Mechanics of a Tax Refund

To estimate your refund accurately, you must first understand how the Internal Revenue Service (IRS) determines your final tax bill. Your refund is not a random gift; it is the mathematical result of your total tax payments minus your total tax liability.

The Concept of Tax Liability

Your tax liability is the total amount of tax you owe the government based on your annual income, after accounting for deductions and credits. If you have paid more throughout the year (via employer withholding or estimated quarterly payments) than this final liability number, you receive the difference back as a refund. Conversely, if you paid less, you owe the government the balance.

Tax Withholding and the W-4

For most employees, tax payments happen automatically through withholding. When you start a job, you fill out a Form W-4. The information you provide—such as your filing status and number of dependents—tells your employer how much to take out of each paycheck. If you find that you consistently receive a massive refund every year, it usually means your W-4 is set up to withhold too much, effectively reducing your monthly take-home pay.

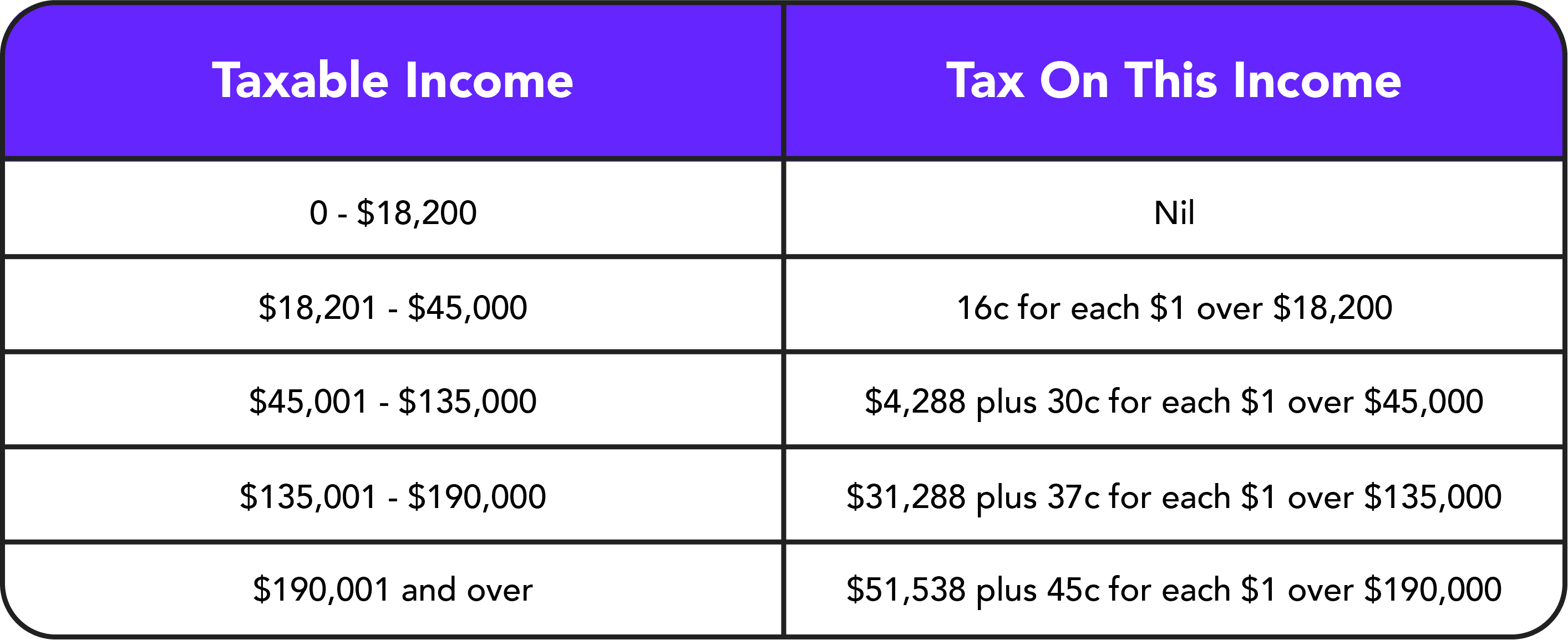

Tax Brackets and Progressive Taxation

The United States uses a progressive tax system, meaning that different portions of your income are taxed at different rates. As your income moves into higher “brackets,” only the money within those specific ranges is taxed at the higher rate. Understanding which bracket you fall into is the first step in calculating your potential liability and, subsequently, your refund.

Key Variables That Determine Your Refund Amount

Several factors dictate whether you will see a check in the mail or a bill from the IRS. These variables are the “moving parts” of your financial life that interact with the tax code.

Filing Status

Your filing status is perhaps the most significant factor in determining your tax rate and the size of your standard deduction. The IRS recognizes five statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Surviving Spouse. For instance, the “Head of Household” status offers more favorable tax brackets and a higher standard deduction than “Single,” which can significantly increase your refund if you qualify.

Gross Income vs. Adjusted Gross Income (AGI)

Your “Gross Income” includes everything from wages and bonuses to investment dividends and freelance earnings. However, the IRS allows you to subtract certain “above-the-line” adjustments—such as contributions to a traditional IRA, student loan interest, and health savings account (HSA) contributions—to arrive at your Adjusted Gross Income (AGI). A lower AGI is the key to unlocking many tax credits and reducing your overall tax burden.

Taxable Income

Once you have your AGI, you subtract either the standard deduction or your itemized deductions to reach your “Taxable Income.” This is the actual number upon which your tax is calculated. For the 2023 and 2024 tax years, the standard deduction has remained relatively high due to inflation adjustments, meaning fewer people find it beneficial to itemize.

Maximizing Your Return through Deductions and Credits

If you want to increase the amount of money you get back, you must focus on the two primary tools for tax reduction: deductions and credits. While they are often used interchangeably in casual conversation, they function very differently in the world of finance.

Standard Deduction vs. Itemized Deductions

The standard deduction is a flat dollar amount that reduces the income you’re taxed on. Itemized deductions, on the other hand, allow you to list specific expenses like mortgage interest, state and local taxes (SALT) up to $10,000, medical expenses exceeding a certain percentage of your AGI, and charitable contributions. You should only itemize if the total of these expenses exceeds the standard deduction amount for your filing status.

The Power of Tax Credits

While deductions reduce the amount of income subject to tax, tax credits are far more valuable because they provide a dollar-for-dollar reduction of your actual tax bill. For example, if you owe $5,000 in taxes and qualify for a $2,000 credit, your bill drops directly to $3,000.

- The Child Tax Credit (CTC): A significant boon for families, providing a credit for each qualifying child under age 17.

- The Earned Income Tax Credit (EITC): Designed for low-to-moderate-income working individuals and couples, particularly those with children. This is a “refundable” credit, meaning if the credit reduces your tax bill below zero, the government pays you the remaining balance.

- Education Credits: The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) help offset the costs of higher education.

Non-Refundable vs. Refundable Credits

It is crucial to distinguish between these two. A non-refundable credit can reduce your tax liability to zero, but any “leftover” credit is lost. A refundable credit, however, can result in a refund even if you owe no taxes at all. This distinction is often the reason why some taxpayers receive refunds that are much larger than the total amount of tax withheld from their paychecks.

How to Estimate Your Refund Before Filing

You don’t have to wait until you hit “submit” on your tax software to know where you stand. Several methods can help you estimate your refund amount with reasonable accuracy.

Using the IRS Tax Withholding Estimator

The IRS provides a robust online tool called the “Tax Withholding Estimator.” By inputting your most recent pay stubs and last year’s tax return, the tool can project whether you are on track for a refund or a balance due. This is particularly useful for those with complex financial lives, such as those with multiple jobs or side hustles.

The Role of Tax Preparation Software

Modern tax software has revolutionized personal finance. Most platforms allow you to input your data for free and will show you a “running tally” of your refund in the corner of the screen. This allows you to see in real-time how adding a specific deduction or reporting a piece of income affects your bottom line.

Manual Calculation for Financial Literacy

For those who prefer a “pencil and paper” approach to finance, you can estimate your refund by:

- Summing all your income sources.

- Subtracting adjustments to find your AGI.

- Subtracting your standard deduction to find taxable income.

- Applying the tax bracket rates to find your tentative tax.

- Subtracting tax credits.

- Comparing that final number to the total federal tax withheld on your W-2s.

Optimizing Your Financial Position for the Future

Once you determine “how much tax return you will get,” the final step is to decide if that number is actually healthy for your overall financial plan.

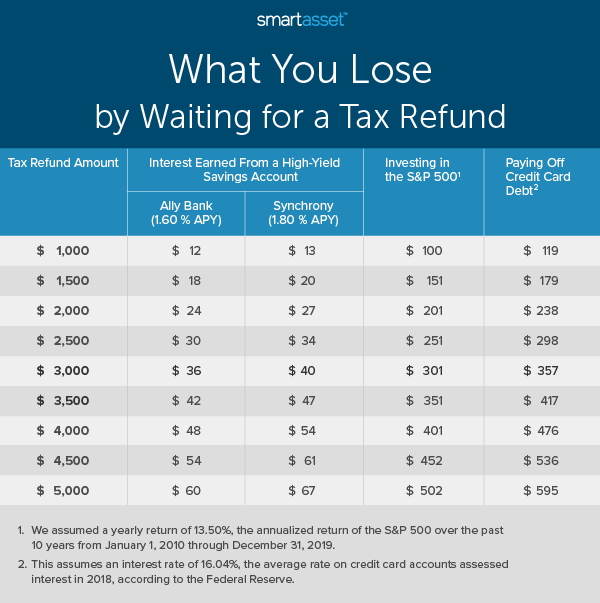

Why a Huge Refund Isn’t Always the Goal

While a $5,000 refund feels like a windfall, from a strict personal finance perspective, it represents poor capital management. That is $416 a month that you didn’t have access to for groceries, debt repayment, or investment in a high-yield savings account. Ideally, you want your refund to be as close to zero as possible—meaning you kept your money throughout the year rather than giving the government an interest-free loan.

Mid-Year Adjustments

If your refund is excessively large (or if you unexpectedly owe a large sum), you should update your W-4 with your employer immediately. Adjusting your withholdings ensures that your take-home pay reflects your actual tax obligation. This “paycheck optimization” is a hallmark of sophisticated financial planning.

Strategic Use of the Refund

If you do receive a significant refund, resist the urge to treat it as “free money” for luxury purchases. Instead, view it as a strategic tool for your financial foundation. Consider:

- Funding an Emergency Fund: Use the refund to build a 3–6 month safety net.

- High-Interest Debt Paydown: Target credit card balances to save on interest.

- Retirement Contributions: Use the refund to fund a Roth IRA or increase your 401(k) contributions, which can further reduce your tax liability for the following year.

By understanding the “why” and “how” behind your tax refund, you transform a yearly administrative task into a powerful lever for building long-term wealth. Whether your refund is $50 or $5,000, the knowledge of how that number was reached is your most valuable asset this tax season.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.