The question of “how much should you have for retirement” is one of the most critical and frequently asked in personal finance. It’s a question that, while seemingly straightforward, unlocks a complex web of personal circumstances, economic realities, and future aspirations. There’s no universal magic number that applies to everyone; instead, your ideal retirement nest egg is a highly personal figure, shaped by your desired lifestyle, health considerations, projected income sources, and even the legacy you wish to leave.

Understanding this figure is not merely about accumulating a large sum; it’s about securing financial independence and peace of mind during your golden years. It’s about ensuring that when you decide to step away from full-time work, you can maintain your quality of life, pursue passions, and navigate unexpected challenges without financial stress. This article will delve into the essential components of calculating your retirement needs, offering insights and strategies to help you build a robust plan for your future.

Understanding Your Personal Retirement Landscape

Before you can determine “how much,” you need a clear picture of “what kind of retirement.” This involves more than just numbers; it’s about envisioning your post-work life and understanding the factors that will shape your financial needs.

Defining Your Retirement Vision and Lifestyle

Your retirement vision is the cornerstone of your financial planning. Will you be traveling the world, pursuing expensive hobbies, or simply enjoying a quiet life at home? Each choice carries a different price tag. Start by sketching out what your ideal retirement day, week, and year look like.

- Daily Living Expenses: Consider your current monthly spending habits. While some expenses like commuting and work-related attire might decrease, others like healthcare, travel, and leisure activities could increase. Don’t assume your expenses will automatically drop significantly; many retirees find their early retirement years to be quite active and therefore costly.

- Big-Ticket Items: Factor in any major purchases or goals you have for retirement, such as buying a second home, renovating your current one, or funding significant trips.

- Healthcare Costs: This is often the largest variable and a significant concern for retirees. Even with Medicare, out-of-pocket expenses, prescription drugs, and potential long-term care needs can be substantial. It’s crucial to factor in a robust allocation for healthcare.

The Role of Time Horizon and Life Expectancy

The longer you expect to be retired, the more money you will need. Advances in medicine and healthier lifestyles mean people are living longer, often into their 80s, 90s, and beyond. This extended lifespan is wonderful but requires a longer financial runway.

- Retirement Age: When do you plan to stop working? Retiring at 60 versus 70 has a profound impact on both the number of years you need to save and the number of years your savings need to last. Early retirement requires a larger nest egg.

- Personal and Family Health History: While no one can predict the future, understanding your family’s health history can offer clues about potential longevity and future healthcare needs.

- Inflation’s Silent Erosion: The purchasing power of money diminishes over time due to inflation. A dollar today will buy less in 20 or 30 years. Your retirement savings must not only cover your expenses but also grow at a rate that outpaces inflation to maintain your purchasing power throughout retirement. Financial plans must account for a realistic inflation rate, typically 2-3% per year, compounding over decades.

Key Metrics and Rules of Thumb for Retirement Savings

While a personalized plan is essential, several widely recognized rules of thumb can provide a starting point and offer benchmarks for your progress. These are general guidelines, not strict mandates, but they offer valuable perspective.

The 4% Rule and Its Implications

The 4% rule is a popular guideline suggesting that you can safely withdraw 4% of your initial retirement portfolio balance each year, adjusted for inflation, without running out of money for at least 30 years.

- Calculating Your Target: If you expect to need $80,000 per year in retirement, the 4% rule suggests you’d need a portfolio of $2,000,000 ($80,000 / 0.04). This provides a quick estimate but has its limitations, especially in periods of high market volatility or for longer retirement horizons.

- Limitations and Modern Adaptations: The 4% rule was based on historical market data and a specific asset allocation. Financial advisors sometimes suggest a more conservative withdrawal rate, like 3.5%, or dynamic withdrawal strategies that adjust based on market performance, especially for those with longer retirement spans or higher risk aversion.

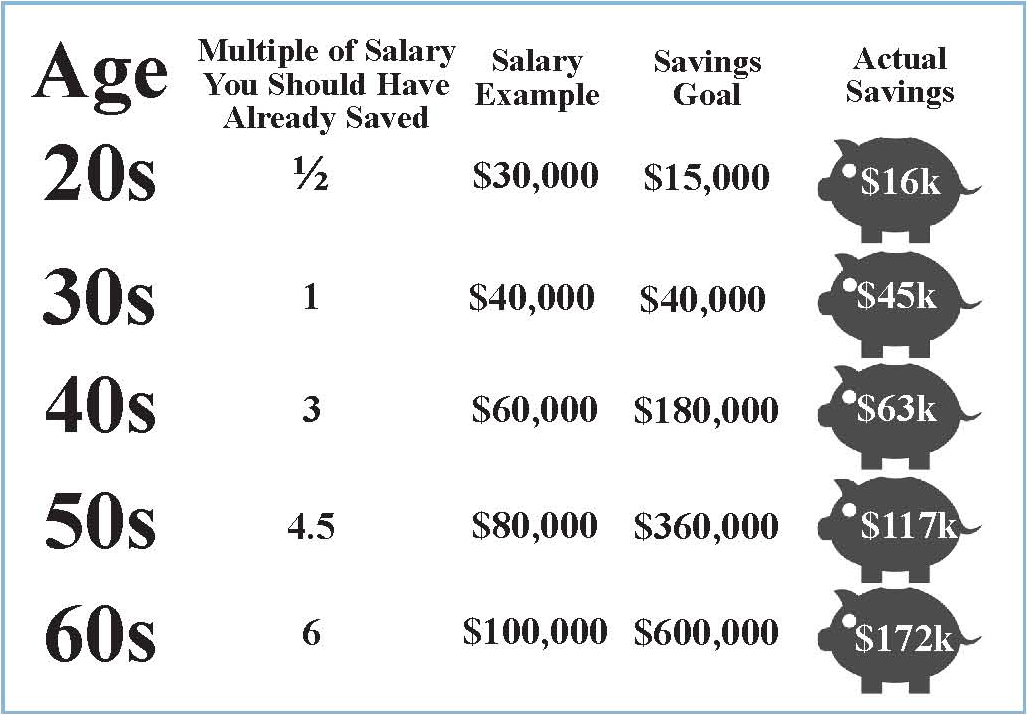

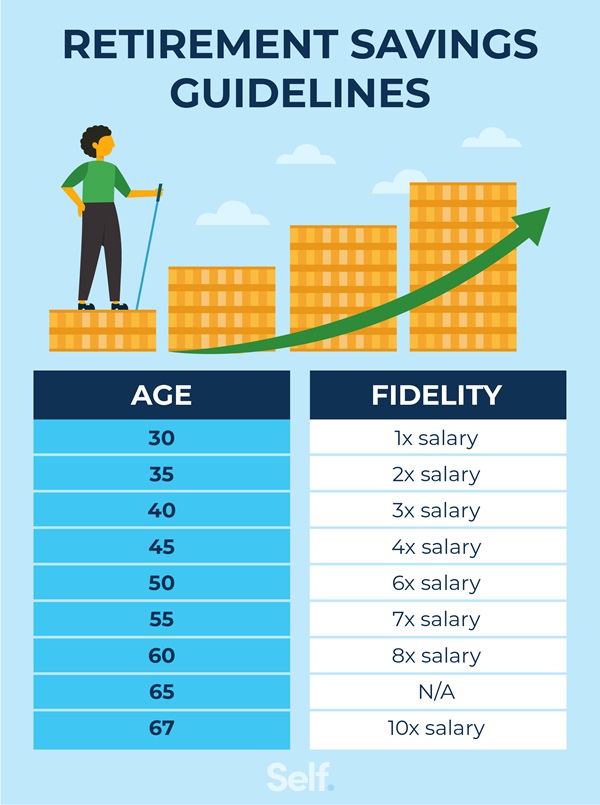

The Power of Multiples of Salary

Another common approach is to aim for a certain multiple of your pre-retirement salary by specific ages. Financial institutions and advisors often publish these benchmarks.

- Example Benchmarks:

- By age 30: 1x your salary

- By age 40: 3x your salary

- By age 50: 6x your salary

- By age 60: 8x your salary

- By retirement (e.g., age 67): 10x your salary

- Using as a Guide: These benchmarks are helpful for tracking progress but should be adjusted based on your individual income needs in retirement. Someone planning to live frugally might need less, while someone with ambitious retirement goals might need more. The key is to continuously evaluate if your current savings trajectory aligns with your ultimate financial objectives.

Considering Other Income Streams

Your retirement doesn’t solely depend on your personal savings. Other income sources can significantly reduce the amount you need to save yourself.

- Social Security Benefits: For many, Social Security will provide a foundational layer of income in retirement. Understanding your estimated benefits (which you can typically access via the Social Security Administration’s website) is crucial. Remember, Social Security is generally intended to replace only a portion of your pre-retirement income, not all of it.

- Pensions: If you are fortunate enough to have a defined-benefit pension plan from an employer, this can be a substantial guaranteed income stream. Understand its terms, payout options, and any survivor benefits.

- Part-Time Work or Side Gigs: Many retirees choose to work part-time, either for supplemental income or to stay engaged. This can alleviate pressure on your savings, allowing them to last longer or grow further.

- Rental Property Income: If you own rental properties, the income generated can contribute to your retirement living expenses.

Strategies for Building Your Retirement Nest Egg

Once you have a target in mind, the next step is to implement effective strategies to reach it. Consistency, smart investing, and diligent planning are your allies.

Maximizing Retirement Savings Vehicles

Leverage tax-advantaged accounts to accelerate your savings growth.

- 401(k) and Other Employer-Sponsored Plans: If your employer offers a 401(k), 403(b), or similar plan, contribute at least enough to get the full employer match – this is essentially free money. Maxing out these accounts annually is an excellent goal, as contributions are often pre-tax, reducing your current taxable income, and growth is tax-deferred.

- Individual Retirement Accounts (IRAs): Traditional IRAs offer tax-deferred growth, and contributions may be tax-deductible. Roth IRAs, while funded with after-tax dollars, offer tax-free withdrawals in retirement, which can be immensely valuable, especially if you expect to be in a higher tax bracket later.

- Health Savings Accounts (HSAs): Often referred to as a “triple-tax-advantaged” account, HSAs are unique. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. If you’re covered by a high-deductible health plan, an HSA can be a powerful retirement savings tool, especially for those inevitable healthcare costs.

The Power of Compounding and Early Saving

Compound interest is often called the “eighth wonder of the world” for a good reason. The sooner you start saving, the more time your money has to grow exponentially.

- Illustrative Example: A 25-year-old who saves $500 per month until age 65 (40 years) could accumulate significantly more than a 35-year-old saving $750 per month until age 65 (30 years), assuming the same rate of return. The extra decade of compounding makes a massive difference.

- Automate Your Savings: Set up automatic transfers from your checking account to your retirement accounts immediately after payday. “Set it and forget it” removes the temptation to spend the money and ensures consistent contributions. Gradually increase your contribution percentage over time, especially when you receive raises.

Strategic Investing and Portfolio Diversification

How you invest your savings is just as important as how much you save. A well-constructed portfolio can maximize returns while managing risk.

- Asset Allocation: This refers to how you divide your investment portfolio among different asset categories, such as stocks, bonds, and cash equivalents. A younger investor typically has a higher allocation to stocks for growth, while an older investor might shift towards bonds for stability and income as retirement approaches.

- Diversification: Don’t put all your eggs in one basket. Diversify across different types of stocks (large-cap, small-cap, international), bonds (government, corporate), and industries to mitigate risk.

- Regular Rebalancing: Periodically adjust your portfolio back to your target asset allocation. Market fluctuations can cause certain asset classes to grow disproportionately, requiring you to sell some high-performers and buy some under-performers to maintain your desired risk level.

Navigating Retirement Planning Challenges and Adjustments

The path to retirement is rarely linear. Market downturns, unexpected expenses, and life changes can all impact your plan. Staying flexible and proactive is key.

Handling Market Volatility and Economic Downturns

Stock market corrections and recessions are an inevitable part of investing. While they can be unsettling, a long-term perspective is crucial.

- Resist Panic Selling: Selling investments during a downturn locks in losses. History shows that markets tend to recover over time.

- View as an Opportunity: For those still contributing, market dips can be an opportunity to buy assets at lower prices, which can lead to greater returns when the market recovers (dollar-cost averaging).

- Maintain Diversification: A diversified portfolio can cushion the blow of specific market sectors performing poorly.

Adapting to Life Changes and Unexpected Expenses

Life throws curveballs. Job loss, major health issues, or supporting adult children can all impact your retirement savings trajectory.

- Emergency Fund: Maintaining a robust emergency fund (3-6 months of living expenses, or even more for certain situations) is vital to avoid dipping into retirement savings for immediate needs.

- Regular Review and Adjustment: Your retirement plan isn’t a static document. Review it annually or whenever significant life events occur. You may need to adjust your savings rate, investment strategy, or even your planned retirement age.

- Seeking Professional Guidance: A qualified financial advisor can provide invaluable assistance in navigating complex financial situations, optimizing your investment strategy, and ensuring your plan remains on track. They can help you stress-test your assumptions and provide tailored advice.

The Importance of Long-Term Care Planning

One of the most significant and often overlooked expenses in retirement is long-term care. This includes services like nursing home care, assisted living, or in-home care, which are typically not covered by Medicare.

- Understanding the Costs: Long-term care costs can be exorbitant, potentially depleting a lifetime of savings very quickly.

- Exploring Options: Consider long-term care insurance, hybrid life insurance policies with long-term care riders, or self-funding strategies if you have substantial assets. Planning for this eventuality can protect your nest egg and provide peace of mind for you and your family.

Determining “how much you should have for retirement” is an ongoing process that requires careful thought, consistent effort, and periodic adjustments. By defining your vision, understanding the key financial metrics, maximizing your savings vehicles, and preparing for life’s inevitable challenges, you can build a robust retirement plan that ensures a financially secure and fulfilling future. Start today, stay disciplined, and empower your future self with the financial freedom you deserve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.