As tax season approaches, the question on every taxpayer’s mind is consistent: “How much should my tax return be?” For some, a large refund feels like a hard-earned windfall—a yearly bonus used for vacations or debt repayment. For others, a large refund is viewed as a missed opportunity, representing an interest-free loan given to the government.

In the realm of personal finance, understanding the mechanics of your tax return is essential for effective wealth management. A tax return is not a gift; it is a reconciliation of the taxes you owed versus the taxes you paid throughout the year. To determine what your specific number should be, you must look at your income, your filing status, your deductions, and your credits.

Understanding the Fundamentals of the Tax Refund Formula

To estimate your tax return, you must first understand the basic arithmetic the IRS uses. At its core, a tax refund (or a tax bill) is the difference between your total tax liability and the total amount of tax you have already paid through withholding or estimated payments.

Tax Liability vs. Tax Withholding

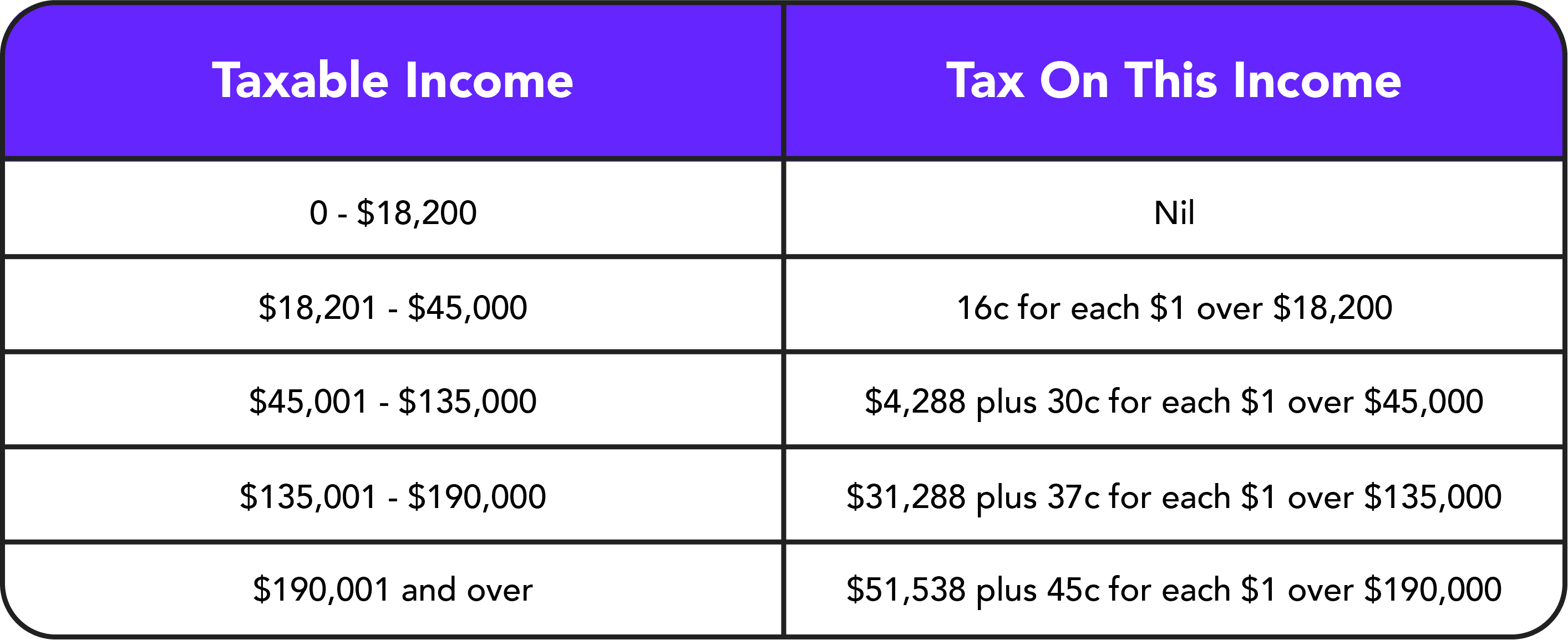

Your tax liability is the actual amount of money you owe the government based on your taxable income. This is determined by applying the current tax brackets to your adjusted gross income. Conversely, tax withholding is the money your employer takes out of your paycheck every pay period and sends to the IRS on your behalf.

If your withholdings exceed your liability, you receive a refund. If your liability exceeds your withholdings, you owe money. Therefore, if you are asking “how much should my return be,” you are actually asking “how much did I overpay?”

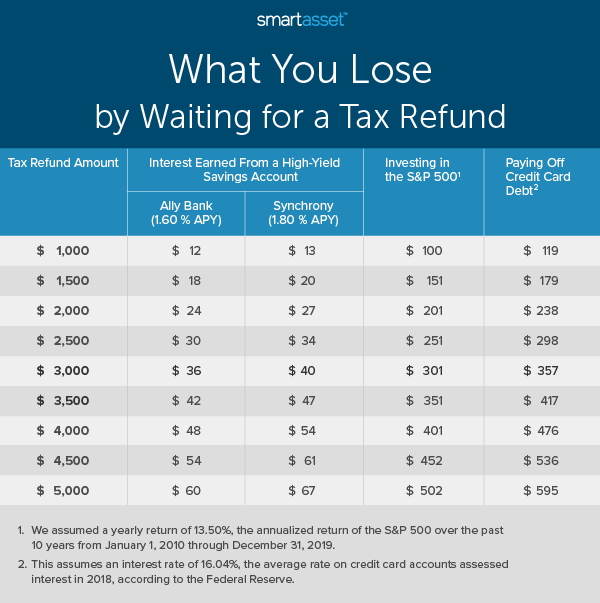

Why a “Big Refund” Isn’t Always a Financial Victory

While receiving a $5,000 check in April feels rewarding, from a professional financial perspective, it indicates a lack of precision in your monthly budgeting. That $5,000 represents roughly $416 per month that you did not have access to during the year. Had that money been in your possession, it could have been invested in a high-yield savings account, used to hedge against inflation, or applied to high-interest debt. Ideally, a “perfect” tax return is as close to zero as possible, meaning you kept your money throughout the year while still meeting your legal obligations.

Key Factors that Influence the Size of Your Return

The specific dollar amount of your return is highly individualized. Several levers can increase or decrease your refund, and understanding these can help you predict your outcome more accurately.

Filing Status and Standard Deductions

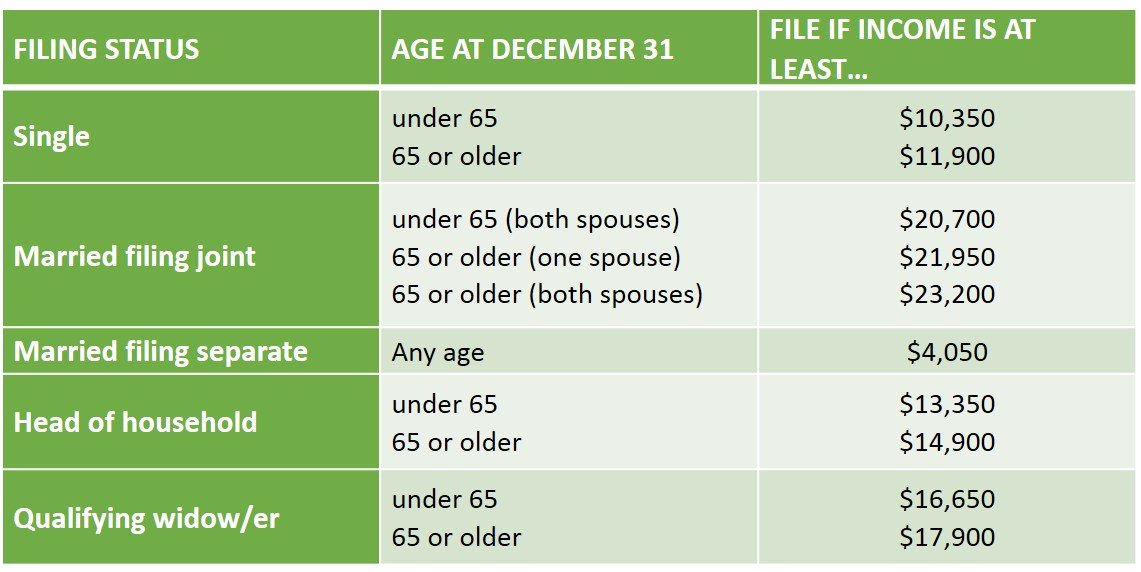

Your filing status is the first major variable. Whether you file as Single, Married Filing Jointly, Married Filing Separately, or Head of Household dictates your standard deduction. The standard deduction is a flat dollar amount that reduces the income you’re taxed on.

For the 2024 tax year, these amounts have increased to account for inflation. A higher standard deduction lowers your taxable income, which generally leads to a lower tax liability. If your employer withheld taxes based on an older, lower deduction estimate, your refund might be larger than in previous years.

Maximizing Itemized Deductions vs. The Standard Deduction

While the majority of taxpayers take the standard deduction, those with significant expenses—such as high mortgage interest, large charitable contributions, or substantial medical bills—may choose to itemize. If your total itemized deductions exceed the standard deduction, your taxable income drops further, potentially increasing your refund. However, since the Tax Cuts and Jobs Act of 2017 nearly doubled the standard deduction, many people find that “how much their return should be” is now dictated by the standard amount rather than complex itemization.

The Power of Tax Credits (Refundable vs. Non-Refundable)

Tax credits are significantly more powerful than deductions. While a deduction reduces the income you are taxed on, a credit reduces your tax bill dollar-for-dollar.

- Non-refundable credits (like the Adoption Credit) can reduce your tax bill to zero, but they won’t give you extra money back.

- Refundable credits (like the Earned Income Tax Credit or the Child Tax Credit) are the primary drivers of large tax refunds. If these credits exceed your total tax liability, the IRS sends you the remaining balance as a check. If you qualify for these, your tax return “should” be significantly higher.

Life Changes and Their Impact on Your Tax Outcome

Your tax return is rarely the same two years in a row because life is rarely static. Major milestones often trigger significant shifts in how much you owe or are owed.

Marriage, Dependents, and Household Composition

Adding a member to your family is one of the quickest ways to change your tax return profile. Getting married can often move a couple into a more favorable tax bracket, especially if there is a disparity between the two incomes. Similarly, each qualifying dependent can open the door to the Child Tax Credit (CTC) or the Credit for Other Dependents. If you recently had a child and didn’t update your W-4 at work, you will likely see a much larger refund than usual because your employer was withholding money as if you had fewer credits.

Investment Gains and Losses

If you are active in the stock market or own real estate, your tax return will be influenced by capital gains and losses. Short-term capital gains are taxed as ordinary income, while long-term gains enjoy lower rates. If you sold assets for a profit, your refund might shrink—or you might even owe money. Conversely, “tax-loss harvesting”—selling losing investments to offset gains—can reduce your taxable income and help protect the size of your return.

Self-Employment and the 1099 Reality

For freelancers, contractors, and side-hustlers, the question of “how much should my tax return be” is often replaced by “how much will I owe?” Unlike W-2 employees, 1099 workers do not have taxes automatically withheld. They are responsible for both the employer and employee portions of Social Security and Medicare taxes (Self-Employment Tax). If you haven’t been making quarterly estimated payments, you should expect your “return” to be a bill. However, you can mitigate this by tracking every business expense, from home office deductions to professional software subscriptions.

Strategic Financial Planning: Adjusting Your Withholding for the Future

Once you determine how much your tax return is likely to be, the next step is to decide if that number serves your long-term financial goals. Professional financial planning involves proactive management of your tax position.

The W-4 Form Strategy

The W-4 is the document you provide to your employer to dictate how much tax is taken out of your paycheck. If your refund last year was $3,000 and your financial situation hasn’t changed, you are overpaying by $250 a month. By submitting a new W-4 and adjusting your “allowances” or “extra withholding,” you can decrease your refund and increase your take-home pay. This is a powerful move for those looking to accelerate debt repayment or increase contributions to a 401(k) or IRA.

Tools and Calculators for Accurate Estimation

You don’t have to wait until April to know your number. The IRS offers a “Tax Withholding Estimator” on their website, which is an invaluable tool for any savvy investor or budgeter. By inputting your current year-to-date pay stubs and last year’s tax return, you can get a real-time snapshot of where you stand. If the tool suggests you will owe a large amount, you can start saving now to avoid interest and penalties. If it suggests a massive refund, you can adjust your withholding to get that money back in your pockets sooner.

Reinvesting the Refund

If you do receive a substantial return, the best “Money” niche advice is to have a plan for it before it hits your bank account. Treating a tax refund as “found money” often leads to lifestyle creep or impulsive spending. Instead, consider the following hierarchy for your refund:

- Emergency Fund: Ensure you have 3–6 months of expenses.

- High-Interest Debt: Pay off credit cards or personal loans.

- Retirement Accounts: Max out your Roth IRA or increase your 401(k) contribution.

- Sinking Funds: Save for known upcoming expenses like car repairs or home maintenance.

Conclusion

So, how much should your tax return be? There is no universal “right” number, but there is a “right” number for your specific strategy. If you prefer the psychological safety of a forced savings plan, a large refund might be your goal. If you are focused on maximizing the time-value of your money, your goal should be a return of zero.

By understanding the interplay between your income, deductions, and credits, and by proactively managing your W-4 withholding, you take control of your financial destiny. Your tax return is not a mystery or a lottery—it is a reflection of your financial planning throughout the year. Use it wisely to build your net worth and secure your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.