Embarking on the journey to homeownership is one of the most significant financial milestones in an individual’s life. However, before you start browsing listings or attending open houses, there is a critical question that must be answered: “How much of a house loan do I qualify for?” Understanding your borrowing capacity is not just about knowing the maximum number a bank will lend you; it is about understanding the intersection of lender requirements, your personal financial health, and your long-term wealth-building goals.

In the world of personal finance, mortgage qualification is a multifaceted process determined by several key variables, including your income, debt levels, credit history, and the current economic environment. This guide provides an in-depth look at how lenders evaluate your profile and how you can calculate your affordability to ensure you make a sound investment.

The Fundamentals of Mortgage Qualification

Lenders do not simply look at your salary and decide on a loan amount. Instead, they use a series of standardized metrics to assess the risk of lending to you. The goal for a lender is to ensure that you can comfortably manage your monthly payments without defaulting on the loan.

Debt-to-Income (DTI) Ratio: The Magic Number

The Debt-to-Income (DTI) ratio is perhaps the most critical factor in determining your loan amount. This ratio compares your total monthly debt obligations to your gross monthly income (before taxes). Most lenders adhere to the “28/36 rule.” This guideline suggests that your mortgage payment (including principal, interest, taxes, and insurance) should not exceed 28% of your gross monthly income, and your total debt (including the mortgage, car loans, student loans, and credit card payments) should not exceed 36%. While some government-backed loans allow for a DTI as high as 43% or even 50% in specific cases, staying closer to the lower end ensures greater financial flexibility.

Credit Scores and Their Impact on Interest Rates

Your credit score is a numerical representation of your reliability as a borrower. It doesn’t just determine if you qualify for a loan, but also the cost of that loan. A higher credit score (typically 740 or above) qualifies you for the lowest possible interest rates. A lower interest rate increases your purchasing power because more of your monthly payment goes toward the principal of the home rather than interest. Even a 1% difference in your interest rate can translate to tens of thousands of dollars in savings over the life of a 30-year mortgage and significantly increase the loan amount you qualify for today.

Employment History and Income Stability

Lenders seek stability. Generally, they want to see at least two years of consistent employment in the same field. If you are a salaried employee, qualification is straightforward. However, if you are self-employed, a freelancer, or rely heavily on bonuses and commissions, the calculation becomes more complex. Lenders will typically average your last two years of tax returns to determine a “qualifying income.” Understanding how your specific income type is viewed is essential to predicting your loan ceiling.

Calculating Your Down Payment and Loan-to-Value (LTV)

The amount of cash you can bring to the table upfront significantly influences your loan qualification. This is expressed through the Loan-to-Value (LTV) ratio, which is the amount of the loan divided by the value of the property.

The 20% Rule vs. Low Down Payment Programs

For decades, a 20% down payment was the gold standard. Putting 20% down immediatey gives you substantial equity and often results in better loan terms. However, in today’s market, many borrowers qualify for loans with much less. Conventional loans can be found with as little as 3% down, and FHA loans require only 3.5%. While a lower down payment allows you to enter the market sooner, it results in a higher loan balance and higher monthly payments, which may actually lower the total price of the home you can afford under DTI constraints.

Private Mortgage Insurance (PMI) Considerations

If you put down less than 20%, lenders usually require Private Mortgage Insurance (PMI). This is an additional monthly fee that protects the lender if you default. When calculating how much you qualify for, you must factor in PMI. Because PMI increases your monthly housing expense, it eats into the 28% DTI limit mentioned earlier. Consequently, a borrower with a 20% down payment will almost always qualify for a higher purchase price than a borrower with a 3% down payment, even with the same income.

Closing Costs: The Often Forgotten Expense

When determining how much of a loan you can afford, you must account for closing costs, which typically range from 2% to 5% of the home’s purchase price. These costs include appraisal fees, title insurance, attorney fees, and taxes. If you have $50,000 saved, you cannot use all $50,000 for a down payment; you must set aside a portion for these closing costs. Failing to account for this can result in a smaller-than-expected down payment, which in turn affects your LTV and loan qualification.

Understanding Interest Rates and Loan Terms

The mortgage market is sensitive to the broader economy. Interest rates fluctuate based on inflation, the Federal Reserve’s policies, and global financial stability. These rates have a direct “inverse” relationship with your loan qualification amount.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

A 30-year fixed-rate mortgage is the most common product, offering stability with a constant interest rate for the life of the loan. However, some borrowers look at Adjustable-Rate Mortgages (ARMs), which offer a lower “teaser” rate for an initial period (e.g., 5 or 7 years). Because the initial rate is lower, you might technically qualify for a larger loan amount with an ARM. However, this comes with the risk of the rate—and your payment—increasing significantly in the future. Financial experts usually recommend ARMs only for those who plan to sell or refinance before the rate adjustment period begins.

15-Year vs. 30-Year Terms: Finding Your Balance

Choosing a 15-year mortgage term usually secures a lower interest rate, but because the loan is paid off in half the time, the monthly payments are substantially higher. If your goal is to maximize the amount of the loan you qualify for, a 30-year term is usually necessary. If your goal is to minimize interest and build equity quickly, the 15-year term is superior. From a qualification standpoint, the higher monthly payment of a 15-year loan will lower the total purchase price a lender will allow.

Current Market Trends and Economic Influence

In a high-interest-rate environment, your “buying power” shrinks. For every 1% increase in mortgage rates, your purchasing power typically drops by about 10%. This means if you qualified for a $400,000 loan at a 4% rate, you might only qualify for roughly $360,000 at a 5% rate. Monitoring the market and locking in a rate when it is favorable is a key strategy for maximizing your loan qualification.

Government-Backed vs. Conventional Loans

The type of loan program you choose can change the qualification criteria entirely. Different programs are designed to help different types of buyers, particularly those who might not fit the traditional “prime” borrower mold.

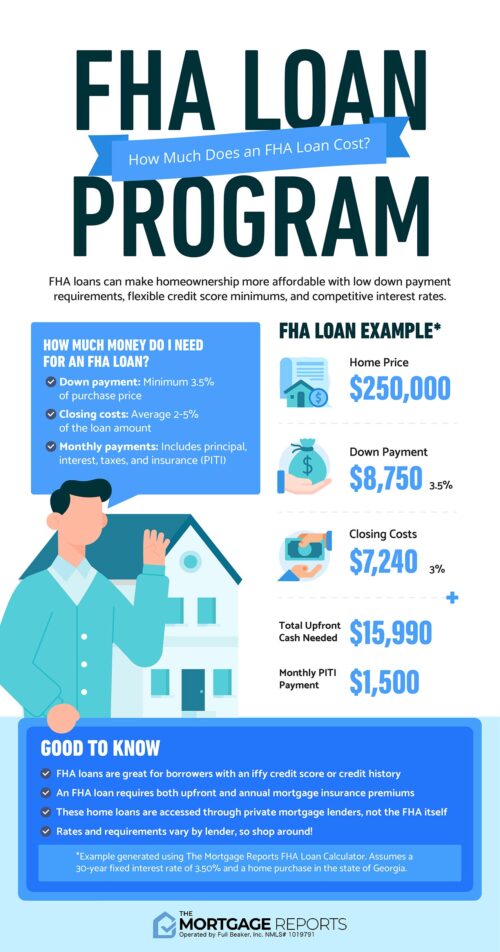

FHA Loans: Low Credit and Low Down Payment Options

Federal Housing Administration (FHA) loans are popular among first-time homebuyers. They allow for credit scores as low as 580 with a 3.5% down payment. Because the government insures these loans, lenders are often more lenient with DTI ratios, sometimes allowing total debt to reach 50% of gross income. This can significantly increase the loan amount for a borrower with moderate income but some existing debt.

VA and USDA Loans: Specialized Benefits

For veterans and active-duty service members, VA loans offer incredible benefits, including 0% down payment requirements and no monthly mortgage insurance. This lack of a down payment and PMI means more of the borrower’s monthly income can go toward the loan principal, often leading to a higher qualification amount. Similarly, USDA loans offer 0% down for buyers in eligible rural and suburban areas, provided they meet certain income limits.

Conventional Financing and Conforming Loan Limits

Conventional loans are not insured by the government and typically have stricter requirements. They must also adhere to “conforming loan limits” set by the Federal Housing Finance Agency (FHFA). If you need to borrow more than these limits, you move into the territory of “Jumbo Loans.” Jumbo loans often require higher credit scores (720+), larger down payments (10-20%), and significant cash reserves in the bank, making them harder to qualify for despite the higher loan amounts.

Proactive Steps to Increase Your Loan Qualification Amount

If the initial estimate of your loan qualification isn’t enough to buy the home you want, there are strategic financial moves you can make to move the needle.

Reducing Existing Debt Loads

Since DTI is a major component of the lender’s formula, paying off a car loan or an outstanding credit card balance can have a massive impact. For every $100 of monthly debt you eliminate, you potentially free up enough room in your DTI to qualify for an additional $15,000 to $20,000 in mortgage debt (depending on interest rates).

Boosting Your Credit Profile

Before applying for a mortgage, spend six months to a year polishing your credit. Ensure all payments are on time, keep your credit utilization below 30%, and avoid opening new lines of credit. A jump from a “fair” credit score to an “excellent” one could lower your interest rate enough to increase your loan qualification by tens of thousands of dollars.

Saving for a Larger Down Payment

While it takes time and discipline, increasing your down payment is the most direct way to afford a more expensive house. A larger down payment reduces the loan amount you need, lowers your LTV, potentially eliminates PMI, and proves to the lender that you are a disciplined saver.

Conclusion

Determining how much of a house loan you qualify for is a vital exercise in financial literacy. It requires a deep dive into your income, a sober look at your debts, and a strategic understanding of the mortgage market. While online calculators provide a quick estimate, the true answer lies in the nuances of your financial profile and the specific loan products available to you.

By managing your DTI ratio, maintaining a stellar credit score, and choosing the right loan program, you can maximize your borrowing power. However, always remember that what a lender will give you and what you should comfortably spend are two different things. Aim for a loan that fits within your broader financial plan, allowing you to own your home without letting your home own you. Seeking a pre-approval from a reputable lender is the best next step to turn these calculations into a concrete plan for your future home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.