In the landscape of global finance, few names command as much gravity as Microsoft. As of 2024, the company has cemented its status as one of the most valuable entities in human history, frequently jostling with Apple and Nvidia for the top spot on the global market capitalization leaderboard. To ask “how much Microsoft is worth” is to look at a figure that exceeds the GDP of many developed nations. However, for the serious investor or business analyst, the sticker price—the market capitalization—is only the beginning of the story.

To understand Microsoft’s true worth, one must look past the $3 trillion-plus valuation and examine the financial engines, capital allocation strategies, and fiscal discipline that allow a legacy software company to trade at such premium multiples in a volatile market.

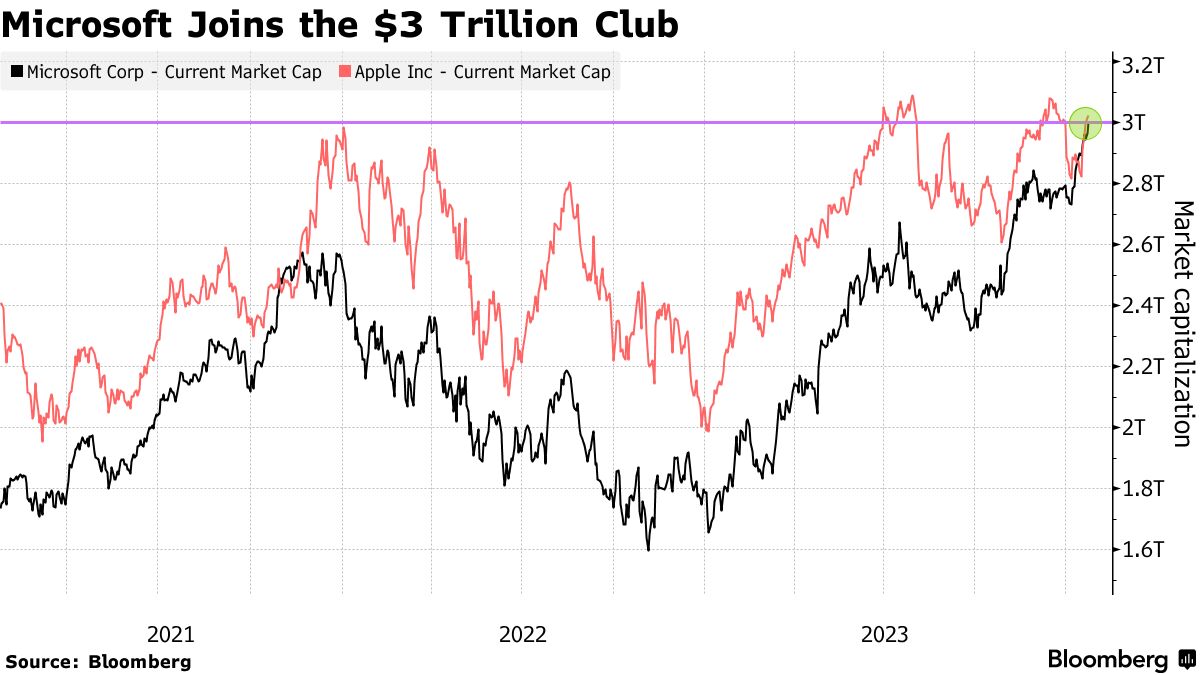

The Architecture of a Multi-Trillion Dollar Market Cap

Market capitalization is the most common metric used to determine a company’s worth, calculated by multiplying the total number of outstanding shares by the current share price. For Microsoft, this journey to the $3 trillion milestone has been a masterclass in shareholder value creation.

The 2024 Milestone and Historical Growth

In early 2024, Microsoft achieved a historic valuation milestone, crossing the $3 trillion threshold. This was not merely a symbolic victory; it represented a massive recovery and expansion following the post-pandemic market correction. To put this in perspective, Microsoft’s valuation has grown exponentially over the last decade. Under the leadership of CEO Satya Nadella, the stock price has seen a CAGR (Compound Annual Growth Rate) that has consistently outperformed the S&P 500, turning Microsoft from a “stagnant” legacy tech firm into the primary driver of the modern bull market.

Price-to-Earnings and Valuation Multiples

A company’s worth is often judged by what investors are willing to pay for every dollar of its earnings. Microsoft consistently trades at a high Price-to-Earnings (P/E) ratio, often hovering between 30x and 35x. This premium valuation suggests that the market does not just value Microsoft for what it is earning today, but for its perceived “moat” and future growth potential. Investors are willing to pay a premium because of the company’s recurring revenue models and its “Fortress Balance Sheet,” which provides a safety net during economic downturns.

Revenue Streams: The Financial Engines Driving the Valuation

Microsoft’s worth is underpinned by a highly diversified and resilient revenue model. Unlike many other tech giants that rely on a single source of income—such as advertising or hardware sales—Microsoft has three distinct pillars that contribute almost equally to its top and bottom lines.

Intelligent Cloud and the Azure Factor

The “Intelligent Cloud” segment is currently the most significant contributor to Microsoft’s valuation growth. Azure, Microsoft’s cloud computing platform, has seen consistent year-over-year revenue growth in the 20% to 30% range. From a financial perspective, the cloud is a high-margin business with immense scalability. As more enterprises migrate their digital infrastructure to the cloud, Azure’s recurring revenue provides a predictable and expanding cash flow that justifies a higher valuation multiple.

Productivity and Business Processes (Office 365)

The transition from one-time software licenses to the “Software as a Service” (SaaS) model with Office 365 was a pivotal moment in Microsoft’s financial history. By charging a monthly subscription fee, Microsoft eliminated the cyclical nature of its revenue. Today, this segment—which includes LinkedIn and Dynamics 365—acts as a cash cow. The high “stickiness” of these products ensures that even during a recession, businesses are unlikely to cancel their essential productivity tools, making Microsoft’s earnings remarkably “defensive.”

More Personal Computing and the Activision Acquisition

While Windows remains a foundational element of the business, the “More Personal Computing” segment has evolved. The recent $69 billion acquisition of Activision Blizzard is a strategic deployment of capital aimed at capturing the high-growth gaming market. By folding these assets into the Xbox ecosystem and Game Pass subscription model, Microsoft is applying its successful SaaS strategy to the $200 billion gaming industry, further diversifying its income streams and increasing its long-term intrinsic value.

The Financial Impact of the Artificial Intelligence Revolution

If the cloud was the story of the last decade, Artificial Intelligence (AI) is the primary catalyst for Microsoft’s current and future valuation. Microsoft’s early and aggressive investment in OpenAI has positioned it as the commercial leader in generative AI, adding hundreds of billions of dollars to its market cap in a matter of months.

Strategic Capital Expenditure and OpenAI

Microsoft’s multibillion-dollar investment in OpenAI is one of the most successful capital allocations in corporate history. By integrating GPT-4 models into its entire suite of products (branded as “Copilot”), Microsoft has created a new upselling opportunity. Financially, this allows the company to increase its Average Revenue Per User (ARPU). Analysts suggest that the AI “inflection point” could add an additional $10 billion to $20 billion in annual recurring revenue by 2025, a projection that is already being baked into the current stock price.

Future Earnings Projections and Margin Expansion

The “worth” of AI to Microsoft isn’t just in top-line revenue but in margin expansion. AI tools can automate internal processes, reducing the cost of goods sold (COGS). Furthermore, as Microsoft scales its AI infrastructure, the marginal cost of serving an additional AI customer will decrease. The market is currently pricing Microsoft as the “toll booth” of the AI era—if you want to build or use AI at scale, you will likely have to pay Microsoft for the compute power or the software layer.

Fundamental Analysis: Balance Sheet Strength and Capital Returns

A company’s worth is also measured by its liquidity and how it treats its shareholders. Microsoft is one of only two US-based companies (the other being Johnson & Johnson) to carry a AAA credit rating from Standard & Poor’s—higher than even the US federal government in some historical contexts.

Cash Reserves and Debt Management

As of the most recent filings, Microsoft maintains a massive cash position, often exceeding $100 billion in cash, cash equivalents, and short-term investments. This liquidity gives the company the “optionality” to weather high-interest-rate environments and to make strategic acquisitions (like LinkedIn, Nuance, or Activision) without diluting shareholder value. Its debt-to-equity ratio remains conservative, ensuring that interest payments never threaten the company’s operational stability.

Dividend Growth and Share Buybacks

Microsoft is a favorite among “Dividend Growth” investors. While the yield may seem modest (often around 1%), the company has a long history of increasing its dividend annually by double digits. Combined with an aggressive share buyback program, Microsoft is constantly reducing its share count, which increases the “Earnings Per Share” (EPS) for remaining investors. This return of capital is a key component of its total shareholder return (TSR), making the company worth more to long-term holders.

Investment Outlook: Is the Current Valuation Justified?

When assessing “how much Microsoft is worth,” one must eventually ask if the price is right. Professional valuation requires looking at both the risks and the rewards of the current price levels.

Valuation Metrics and Comparative Analysis

Compared to its peers in the “Magnificent Seven” (Apple, Alphabet, Amazon, Meta, Nvidia, and Tesla), Microsoft is often viewed as the most stable. While it may not have the explosive hardware growth of Nvidia or the consumer hardware dominance of Apple, it possesses the most balanced business model. At a forward P/E of roughly 32x, it is more expensive than Alphabet but offers more diversified enterprise security than Meta. Analysts often use a “Discounted Cash Flow” (DCF) model to estimate its intrinsic value, and many currently place it in the range of $420 to $500 per share, depending on the projected growth of AI.

Risk Factors for Investors

No valuation is without risk. For Microsoft, the primary financial risks include antitrust litigation from the EU and US, which could lead to heavy fines or forced divestitures. Additionally, the high cost of building AI data centers (capital expenditure) could temporarily compress margins if the revenue from AI products takes longer than expected to materialize. Finally, as a global entity, Microsoft is sensitive to currency fluctuations; a strong dollar can eat into the reported profits from international markets.

Conclusion: The Enduring Value of the Microsoft Ecosystem

To determine how much Microsoft is worth, one must look beyond a single number. Its value is the sum of its $3 trillion market cap, its unrivaled position in the enterprise software market, its leadership in the AI revolution, and its pristine balance sheet.

For the modern investor, Microsoft represents more than just a software company; it is a diversified financial powerhouse. Its ability to generate massive free cash flow, reinvest that cash into high-growth sectors like cloud and AI, and return the surplus to shareholders through dividends and buybacks creates a virtuous cycle of value creation. Whether the stock trades up or down in the short term, the fundamental worth of the Microsoft empire is rooted in its status as the indispensable backbone of the global digital economy. As long as businesses need to compute, create, and communicate, Microsoft’s valuation is likely to remain at the pinnacle of the financial world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.