In the contemporary financial landscape, the transition to renewable energy is no longer merely an environmental statement; it is a sophisticated capital allocation strategy. For homeowners and property investors alike, asking “how much is solar panel installation” is the first step in evaluating a long-term asset that promises to hedge against rising utility inflation. Solar photovoltaic (PV) systems represent a significant upfront capital expenditure (CAPEX), but when structured correctly, they transform a recurring monthly liability—the electricity bill—into a predictable, income-generating, or cost-saving asset.

To truly understand the cost of solar, one must look beyond the initial price tag and analyze the net investment after incentives, the internal rate of return (IRR), and the eventual impact on property valuation. This guide provides an exhaustive breakdown of the financial components of solar installation, helping you navigate the complexities of this modern investment.

1. Understanding the Upfront Investment: Breaking Down the Bill

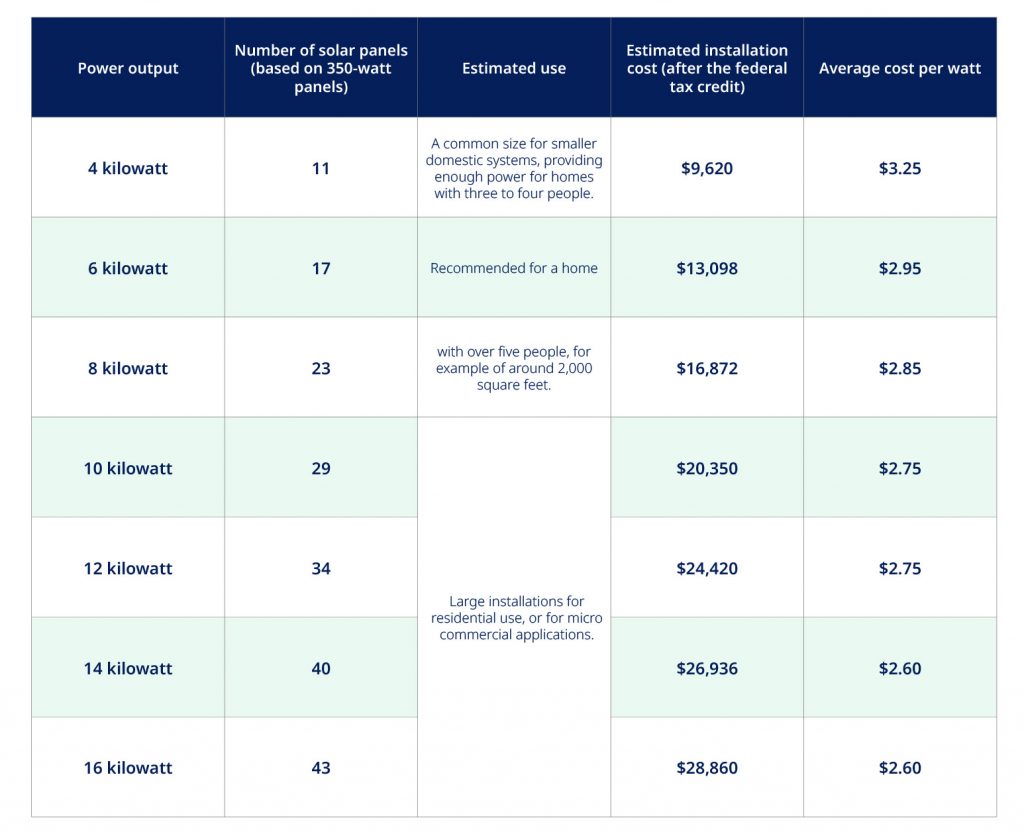

The gross cost of a solar panel system varies significantly based on geographic location, system size, and equipment quality. As of the current market, most residential systems range between $15,000 and $35,000. However, savvy investors look at the “price per watt” (PPW) as the primary metric for comparison.

Equipment Costs vs. Labor Costs

The “hardware” of a solar installation typically accounts for about 25% to 30% of the total price. This includes the silicon-based PV panels, the inverters (which convert DC to AC power), and the racking systems that secure the panels to the structure. While high-efficiency monocrystalline panels carry a premium, they often yield a better long-term ROI by producing more kilowatt-hours (kWh) per square foot.

Labor and operational costs represent a substantial portion of the remaining balance. This includes the engineering design, physical installation by licensed electricians, and the overhead of the installation firm. Choosing a reputable installer with a robust warranty may increase the initial labor cost but serves as an insurance policy against future maintenance liabilities.

Soft Costs: Permitting and Interconnection

In the financial analysis of solar, “soft costs” are often the most overlooked variables. These include the fees associated with local building permits, inspections, and the “interconnection” fee charged by the utility company to hook your system into the grid. In some jurisdictions, these administrative hurdles can account for up to 10% of the total project cost. Understanding these localized expenses is crucial for accurate budgeting and ensuring that your initial capital outlay remains within the projected limits.

2. Leveraging Incentives and Tax Credits to Reduce Capital Outlay

The true cost of solar is rarely the “sticker price.” Government intervention in the energy market has created several financial vehicles designed to de-risk the investment and shorten the payback period.

The Federal Solar Tax Credit (ITC)

The most significant financial lever available in the United States is the Residential Clean Energy Credit, commonly known as the Investment Tax Credit (ITC). Currently, this allows homeowners to deduct 30% of the total installation cost from their federal income taxes.

Crucially, this is a tax credit, not a deduction, meaning it reduces your tax liability dollar-for-dollar. For a $30,000 system, the ITC provides a $9,000 credit, effectively bringing the net cost down to $21,000. For investors, this represents an immediate 30% “return” on capital in the first tax year, significantly enhancing the project’s net present value (NPV).

State-Level Rebates and SRECs

Beyond federal incentives, many states offer cash rebates or performance-based incentives. One of the most lucrative “income” streams from solar is the Solar Renewable Energy Certificate (SREC). In states with SREC markets, for every 1,000 kWh your system produces, you earn one credit that can be sold to utility companies. This turns your roof into a micro-power plant that generates monthly or quarterly passive income, further accelerating the amortization of the initial investment.

3. Financing Your Green Asset: Loans, Leases, and PPAs

The method by which you fund a solar installation dramatically alters the financial outcome. There is a fundamental divide between owning the system and third-party ownership.

Solar Loans: Ownership vs. Debt

Securing a solar loan allows you to maintain ownership of the equipment while spreading the cost over 10 to 20 years. From a wealth-building perspective, solar loans are often preferable to leasing because the homeowner retains the right to the 30% federal tax credit and any SRECs.

When the monthly loan payment is lower than the previous average utility bill, the project becomes “cash-flow positive” from day one. This “bill swap” strategy is a classic financial move that reallocates existing expenses into an equity-building loan.

Solar Leases and Power Purchase Agreements (PPAs)

For individuals who cannot utilize the federal tax credit (due to low tax liability), a lease or PPA may be considered. In these models, a third-party developer owns and maintains the system on your roof, and you simply pay a fixed monthly fee or a set rate for the power produced.

While this eliminates the upfront CAPEX, it generally offers a lower long-term ROI than ownership. Investors should be wary of “escalator clauses” in these contracts, which increase the price of power annually, potentially eroding the savings over time.

4. Calculating the Return on Investment (ROI) and Payback Period

To determine if solar is a sound financial move, one must calculate the “payback period”—the time it takes for the cumulative energy savings to equal the net cost of the system.

Net Metering and Utility Savings

The primary driver of solar ROI is “Net Energy Metering” (NEM). This policy allows you to send excess energy produced during the day back to the grid in exchange for credits on your utility bill. During the night, you use those credits to pull power from the grid. Effectively, the grid acts as a free battery.

In regions with high electricity rates (e.g., California, Massachusetts, or Hawaii), the savings per kWh are higher, leading to a much faster payback period—often between 5 and 8 years. Considering the system’s lifespan is typically 25 to 30 years, this leaves nearly two decades of essentially free electricity.

Property Value Appreciation

From a real estate investment perspective, solar panels are a value-add. Multiple studies, including those by the Lawrence Berkeley National Laboratory, have shown that solar-equipped homes sell for a premium—often around $4,000 per kilowatt of installed solar.

Unlike a kitchen remodel, which may only return 60-80% of its cost, solar panels often offer a 1:1 or higher return on property value, while simultaneously lowering the “holding costs” of the property through reduced utility bills. This makes solar an attractive option for those looking to increase their net worth through real estate.

5. Long-Term Financial Planning: Maintenance and Opportunity Cost

A disciplined financial analysis must also account for the ongoing operational expenses (OPEX) and the opportunity cost of the invested capital.

Inverter Replacement and Upkeep

While solar panels are remarkably durable with no moving parts, the system’s inverter—the “brain” of the operation—typically has a lifespan of 10 to 15 years. Investors should budget for a one-time replacement cost midway through the system’s life, which can range from $1,500 to $3,000. Additionally, in dusty climates, periodic professional cleaning may be required to maintain peak efficiency. Factoring these costs into your 25-year financial model ensures there are no surprises that could negatively impact your IRR.

Solar as a Hedge Against Inflation

Perhaps the most underrated financial benefit of solar is its role as an inflation hedge. Utility companies historically raise rates by 2% to 5% annually. When you install solar, you are essentially “locking in” your electricity rate for the next 25 years.

If you were to take the $20,000 required for a solar system and invest it in the stock market instead, you would need to achieve a post-tax return higher than the combined value of the utility savings, tax credits, and property appreciation to come out ahead. In many high-cost energy markets, the “guaranteed” return of solar savings outperforms the “risk-adjusted” return of traditional market investments, making it a cornerstone of a diversified personal finance strategy.

In conclusion, the question of “how much is solar panel installation” is not just about the check you write today. It is a calculation of net investment, tax optimization, and long-term cash flow. By treating solar as a financial asset rather than a home improvement project, you can secure a predictable, high-yield return that stabilizes your financial future against the volatility of energy markets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.