For the majority of households, a vehicle represents the second-largest financial investment after real estate. Yet, unlike a home, which typically appreciates over time, a car is a depreciating asset that requires a sophisticated understanding of market dynamics to manage effectively. When you ask, “How much is my car worth?” you are not just asking for a number; you are performing a critical assessment of your personal net worth.

Understanding the precise valuation of your vehicle is the cornerstone of sound personal finance. Whether you are looking to trade in for a newer model, sell privately to boost your investment portfolio, or simply track your assets for a balance sheet, knowing the true market value of your car allows you to make informed, data-driven decisions.

Understanding Your Car as a Depreciating Asset

To master your vehicle’s worth, you must first understand the mechanics of depreciation. Depreciation is the difference between the price you paid for a vehicle and what you can get for it when you sell or trade it. In the world of personal finance, minimizing this gap is the key to reducing the “total cost of ownership.”

The Concept of Depreciation Curves

Not all cars lose value at the same rate. Generally, a new car loses about 20% of its value in the first year and roughly 60% of its value after five years. However, high-demand brands with reputations for reliability—such as Toyota or Honda—often follow a shallower depreciation curve. Conversely, luxury vehicles often suffer from “steep” depreciation because the cost of out-of-warranty repairs scares away secondary market buyers. By identifying where your car sits on this curve, you can determine the optimal financial window to exit the asset.

Why Mileage and Condition Dictate Financial Outcome

In the eyes of a financial appraiser, your car is a bundle of remaining utility. Mileage is the primary odometer of that utility. The “psychological barriers” in the used car market—such as 36,000 miles (end of bumper-to-bumper warranties) or 100,000 miles—can cause sharp drops in valuation. Maintaining the vehicle’s physical and mechanical condition is essentially “value preservation.” A car in “Excellent” condition can command a 10-15% premium over one in “Fair” condition, representing thousands of dollars in your pocket.

Leveraging Digital Valuation Tools for Accurate Financial Planning

In the modern era, determining what your car is worth has moved away from guesswork and into the realm of big data. Financial tools and online databases aggregate millions of transactions to provide a “Fair Market Value.” However, to use these tools effectively, you must understand the different types of valuations they provide.

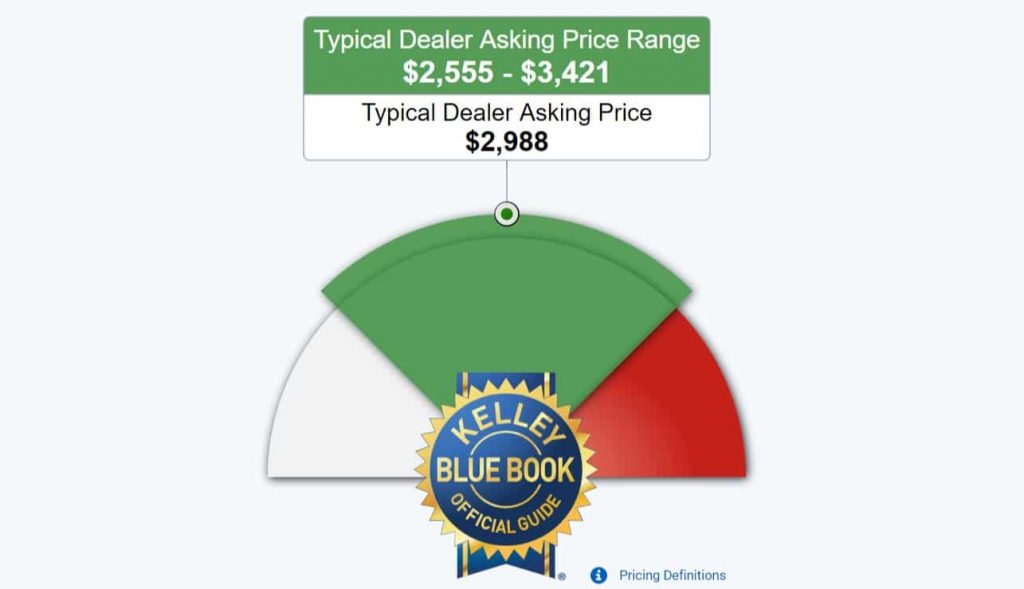

The Difference Between Trade-In, Private Party, and Retail Value

When you use a valuation tool, you will likely see three distinct figures:

- Trade-In Value: This is the lowest figure. It represents what a dealer will pay you. The “discount” you take here is essentially a convenience fee, as the dealer takes on the risk and cost of reconditioning and reselling the car.

- Private Party Value: This is the amount you can expect when selling to another individual. It is higher than trade-in because you are performing the “work” of the dealership.

- Retail Value: This is what a dealer would sell the car for on their lot. You will almost never receive this amount as a seller, but it is a vital metric for insurance purposes and replacement cost analysis.

Using Real-Time Market Data to Your Advantage

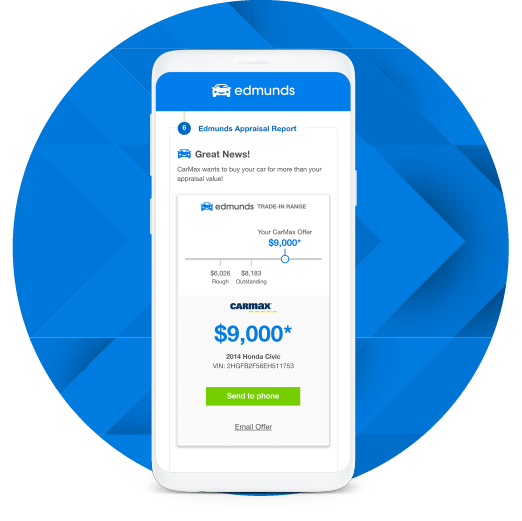

Platforms like Kelley Blue Book (KBB), Edmunds, and NADA are excellent starting points, but they are often lagging indicators. For the most accurate financial picture, look at “instant cash offers” from online retailers like Carvana or Vroom. These platforms provide a liquid, guaranteed price for your asset. In a volatile economy, these real-time offers are often more accurate than traditional book values because they reflect current inventory shortages or surpluses.

Strategic Timing: When to Sell for Maximum Return on Investment

In finance, timing is everything. The value of your car fluctuates based on external economic factors and seasonal trends. Understanding these cycles allows you to “sell high” and optimize your liquidity.

The Impact of Seasonal Market Fluctuations

The used car market is subject to predictable seasonal swings. For example, 4×4 vehicles and SUVs typically see a valuation spike in late autumn as buyers prepare for winter weather. Conversely, convertibles and sports cars command a premium in the spring. Furthermore, the “Tax Refund Season” (February through April) often sees a surge in demand for used cars, driving up prices across the board. If your goal is to maximize the cash value of your car, timing your sale to coincide with these high-demand windows is a savvy move.

Economic Indicators and the Used Car Market

Broader economic trends, such as interest rates and new car supply chain health, directly impact your car’s worth. When interest rates on new car loans are high, more consumers move into the used car market, driving up the value of your current vehicle. Similarly, if new car production is slowed by part shortages, the “scarcity value” of late-model used cars increases. Monitoring these macroeconomic indicators helps you understand if you are in a “Seller’s Market,” allowing you to hold out for a higher price.

Maximizing Residual Value: Financial Habits for Car Owners

While you cannot control the market, you can control the “residual value” of your specific asset. Treating your car as a financial instrument requires disciplined maintenance and documentation.

Maintenance Records as Financial Security

From a financial perspective, a well-documented service history is an insurance policy for your car’s value. When selling a vehicle, the burden of proof is on the seller to show the car has been maintained. A comprehensive folder of receipts and a stamped service book can translate into a significantly higher private-party sale price. It eliminates the “risk discount” that buyers bake into their offers when they are unsure of a vehicle’s history.

Smart Upgrades vs. Over-Customization

Many owners believe that aftermarket upgrades—such as custom wheels, expensive audio systems, or performance tuning—increase the car’s worth. In reality, these often have a negative Return on Investment (ROI). Most buyers and all dealerships prefer vehicles in their original factory configuration. To maintain the highest possible valuation, keep the vehicle “stock.” If you do upgrade, keep the original parts so you can revert the vehicle before sale, potentially selling the aftermarket parts separately for additional income.

Navigating the Transaction: Tax Implications and Reinvestment

The final step in the “How much is my car worth” journey is the transaction itself. This is where you convert the physical asset into liquid capital. However, the gross sale price is not your net gain; you must account for taxes and the cost of the next acquisition.

Tax Benefits of Trade-Ins vs. Private Sales

One of the most overlooked aspects of vehicle valuation is the “Tax Credit” offered in many jurisdictions. In many U.S. states, if you trade in a car at a dealership, you only pay sales tax on the difference between your old car and the new one.

Example: If you buy a $30,000 car and trade in your old car for $10,000, you only pay sales tax on $20,000. If your state tax is 8%, that’s a $800 savings. This effectively makes your $10,000 trade-in worth $10,800. When calculating your car’s worth, always factor in these tax implications to see if a private sale’s higher price actually beats the dealer’s “net” value.

Allocating Proceeds Toward Your Next Financial Goal

Once you have successfully liquidated your vehicle, the way you handle the proceeds will define your long-term financial health. Rather than automatically rolling the entire amount into a more expensive car with a larger loan, consider the opportunity cost. Could a portion of that equity be used to fund an IRA, pay off high-interest debt, or serve as a down payment on an appreciating asset? By viewing your car’s value as a component of your broader financial strategy, you transform a simple “sale” into a step toward financial independence.

Conclusion

“How much is my car worth?” is a question that sits at the intersection of market data, personal maintenance, and economic timing. By treating your vehicle not just as a mode of transportation, but as a significant financial asset, you can mitigate the effects of depreciation and maximize your return. Whether you are leveraging digital tools to find the “sweet spot” in the market or meticulously maintaining records to preserve residual value, a professional approach to vehicle valuation is an essential skill in any wealth-management toolkit. Understanding the numbers today ensures a more secure financial roadmap for tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.