Inflation, a term frequently debated in economic headlines and kitchen table conversations, is far more than just a buzzword. It represents a fundamental shift in the economic landscape, silently yet powerfully influencing the purchasing power of every dollar you earn, save, and spend. For individuals, families, and businesses alike, grasping “how much is inflation” and its multifaceted implications is paramount to financial well-being and strategic planning.

At its core, inflation signifies the rate at which the general price level of goods and services is rising, and consequently, the purchasing power of currency is falling. Imagine a loaf of bread that cost $2 a few years ago now costing $3. That increase is a direct manifestation of inflation. While a moderate and predictable level of inflation is often viewed as a sign of a healthy, growing economy, unchecked or volatile inflation can erode savings, complicate investment strategies, and squeeze household budgets, making it harder to afford daily necessities and plan for the future.

This article delves deep into the mechanics of inflation, exploring how it’s measured, what drives it, and most importantly, its tangible effects on your personal finances. We will equip you with the knowledge to understand this critical economic phenomenon and outline practical strategies to navigate an inflationary environment, ensuring your financial future remains as robust as possible.

Decoding Inflation: What It Is and How It’s Measured

To effectively manage its impact, one must first understand what inflation truly is and how economists quantify its presence and severity. It’s not merely about isolated price hikes but a sustained, broad-based increase across various sectors.

The Core Concept: A Decline in Purchasing Power

At its most fundamental level, inflation means that the same amount of money buys fewer goods and services than it did before. Your $100 bill, while still a $100 bill, has less “stuff-buying power” today than it did last year. This erosion of purchasing power is why understanding inflation is crucial for anyone managing money.

Consider the daily essentials: groceries, fuel, housing, and utilities. When these prices climb consistently, every household feels the pinch. Families might find themselves making difficult choices, cutting back on discretionary spending, or even struggling to meet basic needs. For businesses, rising input costs can compress profit margins, potentially leading to higher consumer prices or reduced output. It’s a domino effect that permeates every corner of the economy.

Key Inflationary Metrics and Their Significance

Economists use several key metrics to measure inflation, each offering a slightly different perspective on price changes within the economy. Understanding these indices helps paint a clearer picture of the inflationary landscape.

-

Consumer Price Index (CPI): This is perhaps the most widely recognized measure of inflation. The CPI measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. This basket includes everything from food and energy to healthcare, housing, and transportation. The CPI is often used to adjust Social Security benefits, pension payments, and even wage agreements, making its fluctuations directly relevant to millions of individuals. A higher-than-expected CPI report can trigger market reactions and influence central bank decisions.

-

Producer Price Index (PPI): While CPI measures prices from the consumer’s perspective, the PPI measures the average change over time in the selling prices received by domestic producers for their output. It tracks prices at different stages of production, from raw materials to finished goods. The PPI is often considered a leading indicator of inflation, as increases in producer prices tend to be passed on to consumers eventually. If businesses face higher costs for raw materials, they are likely to raise their retail prices to maintain profit margins.

-

Personal Consumption Expenditures (PCE) Price Index: The PCE price index is the primary inflation measure used by the U.S. Federal Reserve for its monetary policy decisions. It measures the prices of goods and services purchased by consumers. While similar to CPI, PCE has some key differences: it uses a broader range of expenditures, accounts for consumer substitutions (e.g., if chicken prices rise, consumers might buy more beef), and uses a different weighting system. Many economists believe PCE offers a more comprehensive and stable measure of underlying inflation.

Distinguishing Between Inflation and Deflation/Disinflation

It’s important to differentiate inflation from related concepts like deflation and disinflation, as their implications for your finances are vastly different.

-

Deflation: This is the opposite of inflation – a general decline in prices for goods and services. While it might sound appealing to consumers initially, sustained deflation can be detrimental to an economy. It can lead to reduced corporate profits, wage cuts, unemployment, and a reluctance to spend or invest as consumers delay purchases in anticipation of even lower prices, creating a vicious cycle of economic contraction.

-

Disinflation: This refers to a slowing down of the rate of inflation. Prices are still rising, but at a slower pace than before. For example, if inflation drops from 5% to 2%, that’s disinflation. It’s often a desired outcome for central banks, indicating that their policies to cool an overheated economy are having the intended effect without pushing the economy into deflation.

The Driving Forces Behind Inflation

Inflation isn’t a random occurrence; it’s a complex economic phenomenon driven by a confluence of factors. Understanding these drivers is crucial for anticipating its trajectory and making informed financial decisions.

Demand-Pull Inflation: Too Much Money Chasing Too Few Goods

One of the primary causes of inflation is strong consumer demand outstripping the economy’s ability to produce goods and services. This is known as “demand-pull” inflation. When there’s an abundance of money in the economy (perhaps due to government stimulus, low interest rates, or increased wages) and people are eager to spend, but the supply of goods and services struggles to keep pace, prices get bid up.

Think of it during a housing boom: many buyers with access to cheap credit are competing for a limited number of homes, inevitably driving up prices. Similarly, broad economic growth, robust employment, and increased consumer confidence can collectively fuel demand, leading to upward pressure on prices across various sectors.

Cost-Push Inflation: Rising Production Expenses

Another significant driver is “cost-push” inflation, which occurs when the cost of producing goods and services increases, and these higher costs are then passed on to consumers in the form of higher prices. This can stem from several sources:

- Rising Raw Material Costs: An increase in the price of essential commodities like oil, natural gas, or agricultural products can impact a wide range of industries. For example, higher oil prices affect transportation costs for virtually all goods.

- Wage Increases: When labor markets are tight and workers demand higher wages, businesses may respond by increasing prices to maintain their profit margins. This can sometimes lead to a “wage-price spiral” where rising wages lead to higher prices, which in turn leads to demands for even higher wages.

- Supply Chain Disruptions: Events like pandemics, natural disasters, or geopolitical conflicts can disrupt global supply chains, making it harder and more expensive to source components and transport goods. This scarcity and increased logistical cost directly contribute to higher consumer prices.

The Role of Monetary Policy and Expectations

Central banks, like the U.S. Federal Reserve, play a crucial role in managing inflation through monetary policy. Their primary tool is adjusting interest rates.

- Lowering Interest Rates: When the economy is sluggish, central banks may lower interest rates to encourage borrowing and spending, stimulating demand. However, if rates remain too low for too long, it can lead to excessive demand and inflationary pressures.

- Raising Interest Rates: To combat inflation, central banks typically raise interest rates. This makes borrowing more expensive, discouraging spending and investment, thereby cooling demand and alleviating price pressures. However, tightening too aggressively can risk tipping the economy into recession.

Beyond direct policy, inflationary expectations also play a powerful role. If consumers and businesses expect prices to rise significantly in the future, they may adjust their behavior today – consumers might accelerate purchases, and businesses might raise prices pre-emptively. This self-fulfilling prophecy can embed inflation into the economy, making it harder to control.

The Tangible Impact of Inflation on Your Wallet

Understanding inflation’s causes and measurements is academic without considering its real-world consequences. For most people, inflation directly translates into a tighter grip on their wallets and a re-evaluation of their financial strategies.

Erosion of Purchasing Power and Savings

The most immediate and noticeable impact of inflation is the erosion of your purchasing power. Money sitting in a low-interest savings account, or even just under your mattress, loses value over time. If inflation is 5% and your savings account yields 1%, your real rate of return is -4%. This means your savings are effectively shrinking in value, even if the nominal dollar amount remains the same.

This effect is particularly concerning for retirement savings. If your investment portfolio doesn’t grow at a rate that at least matches inflation, you risk not having enough real wealth to maintain your desired lifestyle in retirement. Fixed-income investments like bonds can also be vulnerable, as their fixed payouts become less valuable over time.

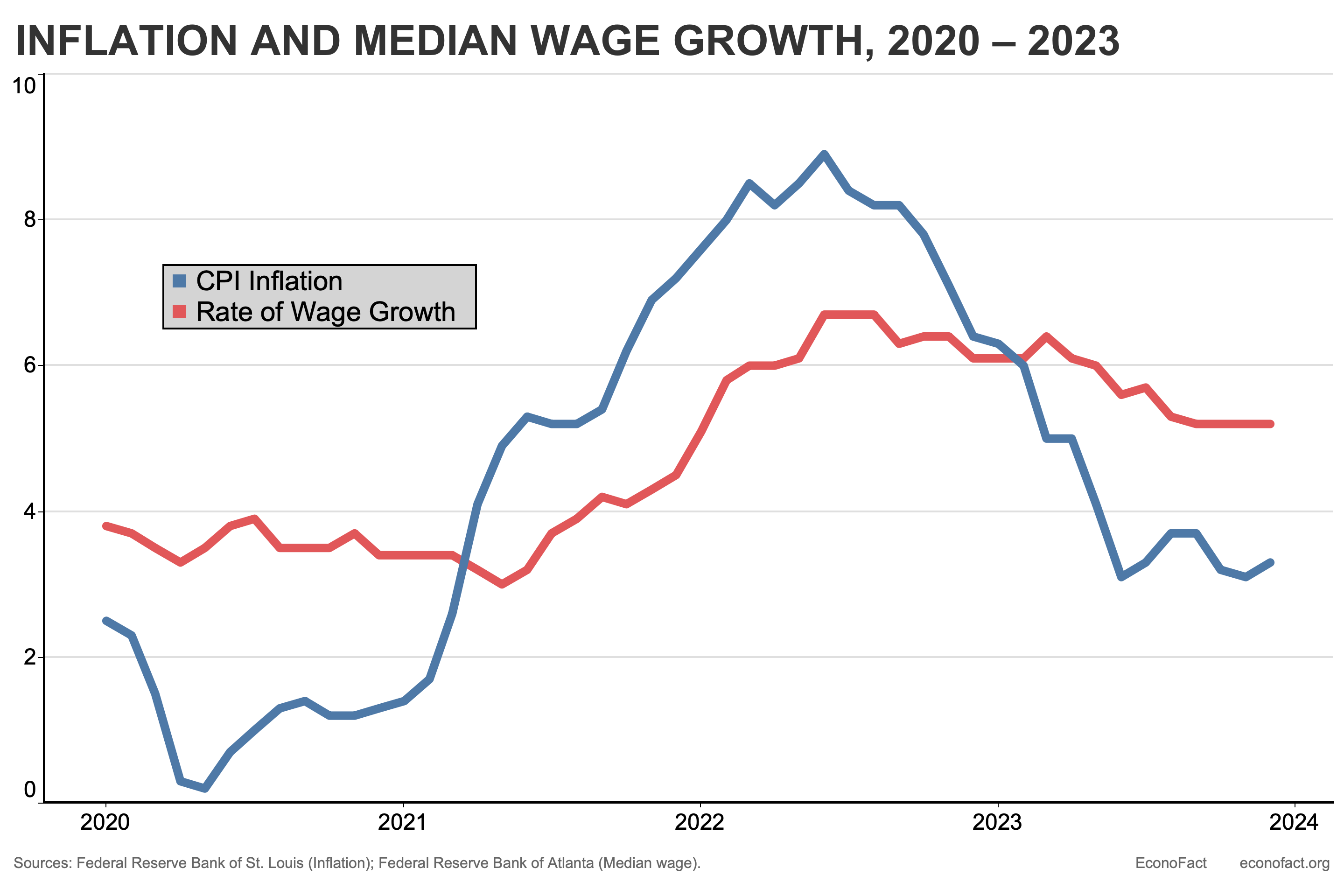

Wage Growth vs. Inflation: The Real Income Squeeze

While you might receive a pay raise, it’s important to distinguish between nominal wage growth and “real” wage growth. Nominal wage growth is the percentage increase in your paycheck. Real wage growth, however, accounts for inflation. If your wages increase by 3% but inflation is 5%, your real wages have actually decreased by 2%. You’re earning more dollars, but those dollars buy less, leaving you feeling poorer despite a higher salary.

This “real income squeeze” is a common complaint during inflationary periods, as many find their wages struggling to keep pace with the rising cost of living. Individuals on fixed incomes, such as retirees relying on pensions or Social Security (unless specifically indexed to inflation), are particularly vulnerable, as their income doesn’t adjust to the rising cost of goods and services.

Debt, Interest Rates, and Borrowing Costs

Inflation’s impact on debt is a mixed bag, depending on the type of debt and the prevailing interest rate environment.

- Fixed-Rate Debt: For those with existing fixed-rate debt, such as a 30-year fixed mortgage, inflation can ironically make the debt feel lighter over time. As wages (hopefully) rise with inflation, the fixed monthly payment represents a smaller proportion of your income in real terms. The purchasing power of the money you pay back is less than the purchasing power of the money you initially borrowed.

- Variable-Rate Debt and New Borrowing: However, when central banks raise interest rates to combat inflation, this directly impacts variable-rate debt (like some credit cards or adjustable-rate mortgages) and the cost of new borrowing. As rates climb, monthly payments on variable-rate loans increase, and taking out new loans for homes, cars, or businesses becomes significantly more expensive, potentially stifling economic activity and making large purchases unaffordable for some.

Strategies to Navigate and Mitigate Inflation’s Effects

While inflation can present significant financial challenges, proactive planning and strategic adjustments can help individuals and businesses protect their wealth and maintain financial stability.

Smart Investing for Inflation Protection

One of the most effective ways to combat inflation is through judicious investment. The goal is to ensure your assets grow at a rate that outpaces or at least matches the inflation rate.

- Stocks (Equities): Historically, over long periods, the stock market has been a strong hedge against inflation. Companies can often pass increased costs onto consumers, and their revenues and profits may grow in nominal terms, leading to higher stock prices. Investing in companies with strong pricing power in essential industries can be particularly beneficial.

- Real Estate: Property values and rental income often tend to rise with inflation, making real estate a potential long-term inflation hedge. Investing in rental properties or real estate investment trusts (REITs) can provide both appreciation and inflation-adjusted income streams.

- Inflation-Protected Securities (TIPS): Treasury Inflation-Protected Securities (TIPS) are bonds issued by the U.S. Treasury that are indexed to inflation. Their principal value adjusts with the Consumer Price Index (CPI), ensuring your investment keeps pace with rising prices. They offer a guaranteed real rate of return, albeit often a modest one.

- Commodities: Gold, silver, and other raw materials are sometimes considered inflation hedges, as their prices can rise during periods of high inflation. However, commodity markets can be volatile, and they don’t always move predictably with inflation. They are generally considered a more speculative part of an inflation-hedging strategy.

Budgeting and Debt Management in an Inflationary Environment

Inflation necessitates a renewed focus on personal budgeting and debt management. Every dollar counts more when its purchasing power is diminished.

- Revisit Your Budget: Scrutinize your expenditures to identify areas where you can cut back. Prioritize essential spending and critically evaluate discretionary purchases. Look for opportunities to save on recurring costs, such as switching insurance providers, optimizing utility usage, or finding cheaper alternatives for common goods.

- Prioritize Debt Repayment: Focus on paying down high-interest debt, especially variable-rate credit card balances or personal loans, as these will become more expensive when interest rates rise. Reducing debt frees up cash flow and reduces your vulnerability to rising borrowing costs.

- Seek Income Growth: Explore opportunities to increase your income. This could involve negotiating a raise at work, acquiring new skills to qualify for higher-paying roles, taking on a side hustle, or even optimizing passive income streams. Protecting your real income is paramount.

Understanding Central Bank Actions and Economic Indicators

Staying informed is a powerful tool in an inflationary environment. Pay attention to macroeconomic news and central bank announcements.

- Monitor Interest Rate Decisions: Keep an eye on announcements from central banks regarding interest rate changes. These decisions directly affect borrowing costs for mortgages, car loans, and credit cards.

- Track Key Inflation Reports: Following CPI, PPI, and PCE reports can provide insights into the current inflation landscape and help you anticipate potential policy responses.

- Consult Financial Professionals: Consider working with a financial advisor who can help you tailor an investment and financial plan specifically designed to navigate inflationary pressures and meet your unique financial goals. They can offer personalized advice on asset allocation and risk management.

Conclusion

The question “how much is inflation” extends far beyond a simple percentage; it delves into the very fabric of our economic reality and personal financial resilience. Inflation is a pervasive force that, left unaddressed, can subtly erode savings, diminish purchasing power, and complicate future planning. However, by understanding its core mechanisms, recognizing its various drivers, and acknowledging its tangible effects on our finances, we are empowered to respond proactively.

Navigating an inflationary environment demands vigilance, adaptability, and a strategic approach to money management. By implementing smart investment strategies focused on inflation protection, meticulously managing budgets and debt, and staying informed about economic indicators and central bank policies, individuals can mitigate the risks and even uncover opportunities. While inflation is a constant presence in market economies, it need not dictate your financial destiny. Instead, let your informed decisions and proactive planning pave the way for a secure and prosperous financial future, regardless of the economic climate.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.