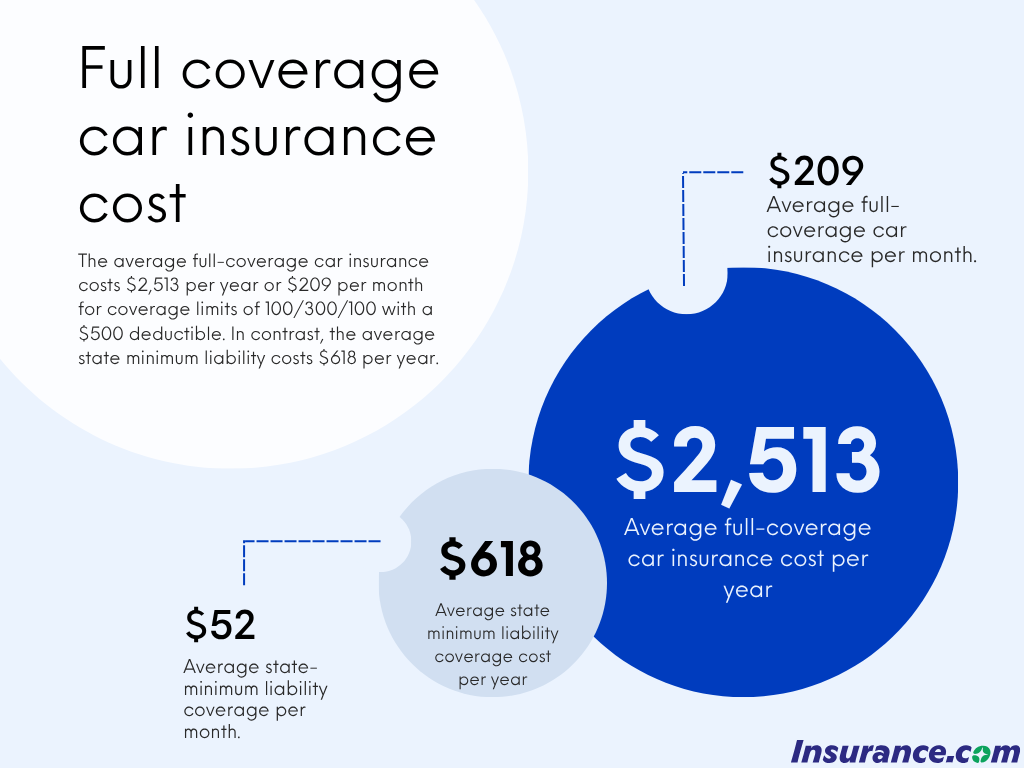

When navigating the complexities of personal finance, one of the most persistent questions for vehicle owners is: “How much is full coverage insurance a month?” While the answer is rarely a single, static figure, understanding the variables that dictate this cost is essential for effective budgeting and long-term wealth preservation. In the United States, the average monthly cost for full coverage auto insurance typically ranges from $140 to $220, or roughly $1,600 to $2,600 annually. However, these figures are merely benchmarks.

From a financial planning perspective, insurance is not just a monthly bill; it is a risk management tool designed to protect your net worth from catastrophic loss. To accurately estimate what you will pay, you must look beyond the “average” and examine the specific levers that move the needle on your premium.

Understanding the Cost Factors of Full Coverage Insurance

The term “full coverage” is actually a misnomer in the insurance industry. It generally refers to a policy that includes liability, collision, and comprehensive coverage. Because this package protects both the other driver (liability) and your own vehicle (collision/comprehensive), the premiums are significantly higher than “minimum coverage” plans.

Personal Demographics and Credit Scores

In the realm of personal finance, your habits often dictate your costs. Actuaries use demographic data to predict risk. Age is perhaps the most significant factor; drivers under 25 often face monthly premiums that are double or triple the national average due to perceived inexperience. Conversely, drivers in their 50s and 60s often enjoy the lowest rates.

More importantly for those focused on financial health, your credit-based insurance score plays a pivotal role in most states. Statistical data suggests a high correlation between financial responsibility and driving safety. Therefore, an individual with a “Poor” credit score might pay $100 to $150 more per month for full coverage than someone with an “Excellent” score, even if their driving records are identical.

Vehicle Make, Model, and Value

The asset you are insuring is the second largest variable. Insurance companies don’t just look at the price tag of the car; they look at the cost of repairs and the likelihood of theft. For example, an electric vehicle (EV) like a Tesla may have a higher monthly premium than a comparably priced gasoline sedan because the specialized components and battery packs are more expensive to replace after an accident. Similarly, high-performance sports cars command higher premiums because they are statistically more likely to be involved in high-speed collisions.

Location and Regional Risk Profiles

Where you park your car at night significantly impacts your monthly cash flow. Insurance is priced based on zip codes. Urban areas with high rates of accidents, vandalism, and theft naturally command higher premiums. Furthermore, state-specific legislation plays a role. In “no-fault” states or states with high litigation rates, such as Michigan or Florida, full coverage can easily exceed $300 a month, whereas drivers in rural states like Maine or Idaho might pay less than $100 for the exact same coverage.

Breaking Down the Average Monthly Premiums

To understand your monthly outflow, it is helpful to categorize the costs based on different driver profiles and coverage levels. In personal finance, granularity is the key to accurate forecasting.

National Averages vs. State Variations

While the national median for full coverage sits around $170 per month, the variance between states is staggering. For instance, a driver in New York might see a monthly bill of $250 for a standard policy, while a driver in Ohio might pay $110. When budgeting, it is vital to research your specific state’s mandatory minimums and how they interact with the optional “full coverage” components. High-traffic states and those prone to natural disasters (like hurricanes or wildfires) will always sit at the higher end of the spectrum.

The Impact of Deductible Choices on Monthly Cash Flow

One of the most direct ways to manipulate your monthly insurance cost is through your deductible—the amount you pay out of pocket before insurance kicks in. In a financial strategy, this is a trade-off between monthly fixed costs and potential emergency costs.

- Low Deductible ($250 – $500): Results in a higher monthly premium but protects you from a sudden $1,000 hit to your savings.

- High Deductible ($1,000 – $2,000): Can lower your monthly premium by 15% to 30%.

For a disciplined investor with a robust emergency fund, opting for a higher deductible and “self-insuring” the small risks can save thousands of dollars over a decade.

Comparing High-Risk vs. Low-Risk Driver Profiles

Your driving history is the ultimate “financial report card” for insurers. A single speeding ticket can increase your monthly premium by 20% for three years. A DUI or an at-fault accident can cause your monthly rate to skyrocket, sometimes doubling the cost of full coverage. On the other hand, a “clean” record for five or more years often triggers “safe driver” credits, which are essential for keeping monthly expenses at a minimum.

Strategies to Lower Monthly Insurance Expenses

Reducing your monthly premium is a form of guaranteed return on investment. If you can lower your insurance bill by $50 a month and redirect that money into an index fund, the long-term wealth creation is substantial.

Leveraging Multi-Policy and Loyalty Discounts

The most common strategy in business finance is the “bundle.” Insurance companies are willing to take a lower profit margin per policy if they can capture more of your business. Combining your auto insurance with homeowners, renters, or life insurance can result in a 10% to 25% discount on your total monthly bill. Additionally, many insurers offer “loyalty discounts” for staying with them for multiple years, though it is still important to shop around every two years to ensure the “loyalty” rate is actually the most competitive.

Telematics and Usage-Based Insurance (UBI)

For those comfortable with data sharing, telematics is a game-changer in lowering monthly costs. By using a mobile app or a device plugged into your car, insurers track your braking, acceleration, and mileage. If you are a cautious driver or work from home and don’t commute, you could see your monthly premium drop by as much as 40%. This shifts the pricing model from “group risk” to “individual behavior,” a much fairer approach for the fiscally responsible driver.

The Role of Defensive Driving and Professional Affiliations

Many drivers overlook small but effective discounts. Completing a certified defensive driving course can often shave 5% to 10% off your monthly premium. Furthermore, many insurance providers have partnerships with professional organizations, alumni associations, or large employers. Checking if your company or university offers a group discount is a low-effort way to optimize your monthly financial commitments.

Integrating Insurance into Your Long-Term Financial Plan

Insurance should not be viewed in a vacuum. It is a vital component of your broader financial architecture. The goal is not necessarily to find the cheapest insurance, but the best value that protects your assets.

Balancing Premiums with Out-of-Pocket Risk

Financial planning involves managing “ruin risk.” If you have a low net worth, paying a slightly higher monthly premium for a low deductible is often the safer financial move, as a $1,000 surprise repair could lead to high-interest credit card debt. However, as your net worth grows, your ability to absorb risk increases. At that stage, increasing your deductibles to lower your monthly fixed costs becomes a more efficient use of capital.

Periodic Rate Auditing and Comparison Shopping

The insurance market is highly dynamic. Companies change their “appetite” for certain types of risk every year. A company that was the cheapest for you when you were 25 might be the most expensive once you turn 35 or get married. Auditing your insurance every 12 to 18 months is a hallmark of good personal finance. Use independent agents or online comparison tools to ensure you aren’t overpaying for your “full coverage” peace of mind.

The Opportunity Cost of Over-Insurance vs. Under-Insurance

Finally, consider the age of your vehicle. If you are driving an older car worth less than $5,000, paying $150 a month for “full coverage” (specifically collision and comprehensive) might be a poor financial decision. You could potentially pay more in premiums over two years than the car is actually worth. In this scenario, switching to liability-only and redirecting the savings into a dedicated “car replacement fund” is often the smarter money move.

In conclusion, while the question of “how much is full coverage insurance a month” usually yields a range between $140 and $220, your specific financial reality depends on your credit, your car, and your willingness to actively manage your policy. By treating insurance as a strategic financial tool rather than a static expense, you can protect your assets while keeping your monthly overhead as lean as possible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.