Understanding the cost of car insurance in New York is a critical component of responsible vehicle ownership. The Empire State presents a unique landscape for auto insurance, influenced by a complex interplay of state regulations, demographic factors, and individual driving profiles. This comprehensive guide will delve into the key drivers behind car insurance premiums in New York, offering insights into average costs, the factors that most significantly impact your individual rate, and strategies for securing the most affordable coverage without compromising on protection.

The Average Cost of Car Insurance in New York

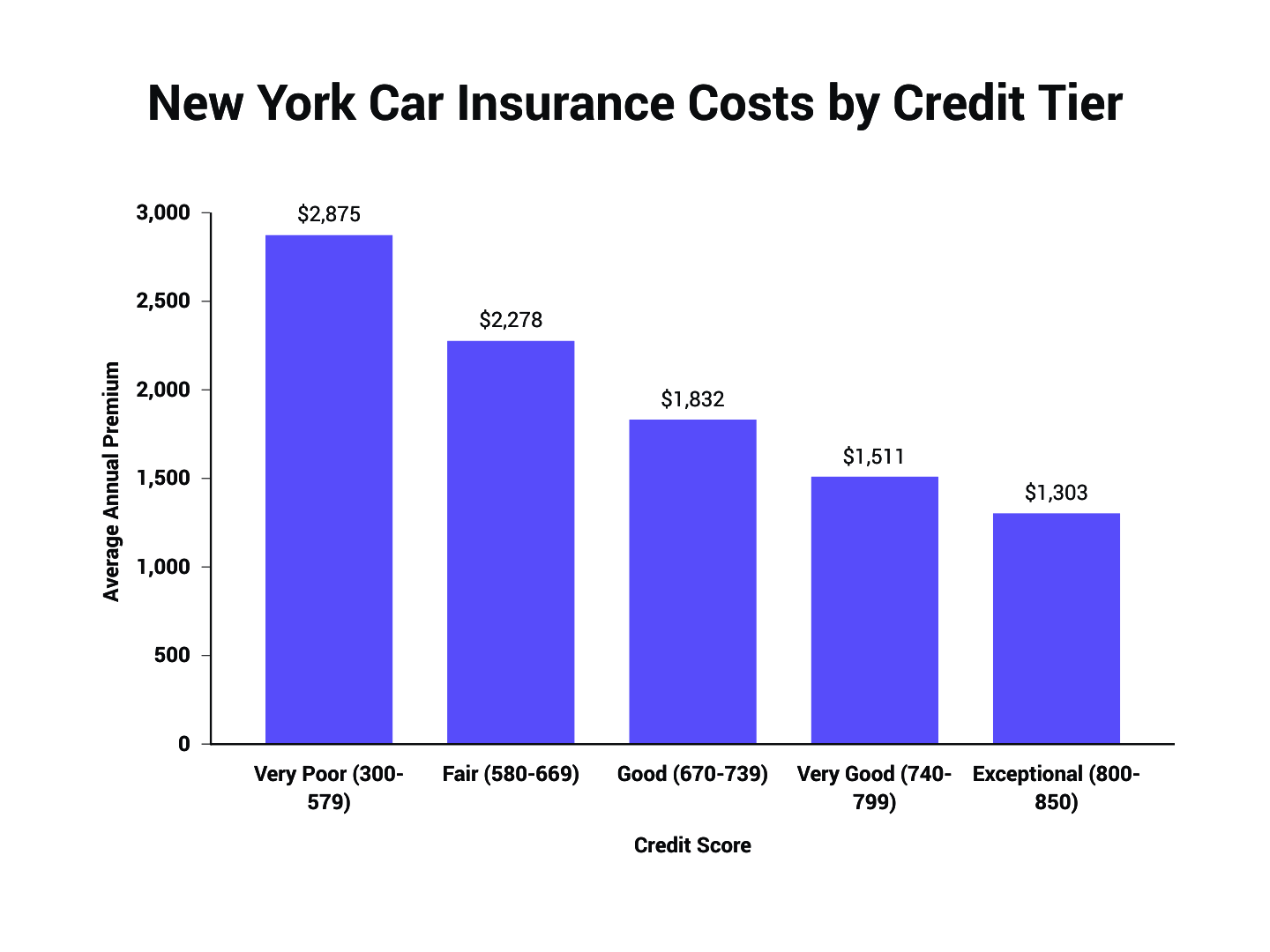

New York consistently ranks among the states with the highest average car insurance premiums in the United States. This isn’t a random occurrence; it’s a direct reflection of several inherent characteristics of the state. These include a high population density, a significant number of vehicles on the road, and a legal environment that often favors policyholders in claims. Consequently, insurers face higher potential payouts, which translates into increased costs for all drivers.

State-Mandated Minimums and Their Impact

New York, like all states, has mandatory minimum insurance requirements that every driver must meet. These minimums dictate the least amount of liability coverage you are legally permitted to carry. As of current regulations, New York requires:

- $25,000 bodily injury liability per person: This covers medical expenses and lost wages for individuals injured in an accident you cause.

- $50,000 bodily injury liability per accident: This is the maximum amount your insurance will pay out for all bodily injuries in a single accident.

- $25,000 property damage liability per accident: This covers the cost of damage to other people’s property (vehicles, fences, buildings, etc.) in an accident you cause.

- $50,000/$100,000/$25,000 in Uninsured/Underinsured Motorist (UM/UIM) coverage: This is crucial for protecting you if you’re involved in an accident with a driver who has no insurance or insufficient insurance.

While these minimums provide a baseline of legal compliance, they are often insufficient for true financial protection in the event of a serious accident. The average cost of car insurance in New York reflects not just the risk associated with the state’s driving environment but also the general tendency for drivers to opt for higher levels of coverage than the bare minimum to adequately safeguard their assets. Therefore, the “average” cost you’ll encounter often assumes coverage exceeding these basic requirements, leaning towards more robust protection.

Factors Influencing Your Specific Premium

While state averages provide a benchmark, your individual car insurance premium in New York will be uniquely determined by a multitude of personal and vehicle-specific factors. Insurers use these data points to assess your risk profile and calculate the likelihood of you filing a claim.

Your Driving Record: The Cornerstone of Your Premium

Perhaps the most significant factor influencing your car insurance cost is your driving record. Insurers view a clean record—free of accidents, speeding tickets, DUIs, and other traffic violations—as indicative of a low-risk driver. Conversely, a history of infractions signals a higher risk, leading to substantially increased premiums. Even minor violations can have a cumulative effect over time.

Accidents and Violations

The severity and recency of accidents and violations play a crucial role. A minor speeding ticket from five years ago will have less impact than a recent at-fault accident or a DUI conviction. Insurers typically look back at your driving history for three to seven years, with more recent events carrying greater weight. In New York, points assessed on your license for moving violations can also directly translate into higher insurance costs, as they are a clear indicator of risky driving behavior.

Deductibles and Their Trade-Off

Your chosen deductibles also play a significant role in determining your premium. A deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in for a claim. Opting for higher deductibles on collision and comprehensive coverage will generally result in lower monthly premiums. However, it’s essential to choose a deductible that you can comfortably afford to pay in the event of a claim. A common trade-off is the balance between immediate savings on premiums and the potential for a larger out-of-pocket expense down the line.

Your Personal Profile: Demographics and Lifestyle

Beyond your driving behavior, several personal characteristics contribute to your insurance premium. These are often based on statistical data that insurers use to predict risk.

Age and Gender

Statistically, younger drivers, particularly those under the age of 25, tend to have higher car insurance rates. This is due to a higher incidence of accidents among this demographic. As drivers gain experience and mature, their premiums typically decrease. While gender has historically been a factor in some states, its influence is becoming less pronounced, with some insurers in New York no longer differentiating rates based on gender, while others still do.

Marital Status

Married individuals often receive slightly lower insurance rates than single individuals. This is often attributed to statistical data suggesting that married drivers tend to be more responsible and less prone to accidents.

Location (ZIP Code)

Your specific geographic location within New York has a substantial impact on your insurance costs. Urban areas with higher population density, more traffic congestion, and a greater incidence of vehicle theft and vandalism will generally have higher premiums compared to rural areas. Even within the same city, your specific ZIP code can influence rates due to localized factors like accident frequency and crime rates.

Your Vehicle: The Make, Model, and Age

The type of vehicle you drive is another critical determinant of your car insurance costs. Insurers consider various aspects of your car when calculating premiums.

Safety Features and Crash Test Ratings

Vehicles equipped with advanced safety features, such as anti-lock brakes, airbags, electronic stability control, and advanced driver-assistance systems (ADAS), can lead to lower premiums. These features reduce the likelihood of accidents and the severity of injuries. Similarly, vehicles with high safety ratings from organizations like the Insurance Institute for Highway Safety (IIHS) often benefit from lower insurance costs.

Repair Costs and Theft Likelihood

The cost of repairing a vehicle and its susceptibility to theft are also significant factors. Expensive luxury cars or those with specialized parts will generally have higher collision and comprehensive insurance costs due to higher repair expenses. Cars that are frequently targeted by thieves in New York may also incur higher theft-related premium increases.

Vehicle Age

While not always a direct driver, the age of your vehicle can influence its value and, consequently, the cost of comprehensive and collision coverage. Newer, more valuable cars will typically have higher premiums for these coverages.

Strategies for Reducing Your Car Insurance Costs in New York

While New York’s car insurance premiums can be high, numerous proactive steps can be taken to mitigate these costs without compromising on essential protection.

Shopping Around and Comparing Quotes

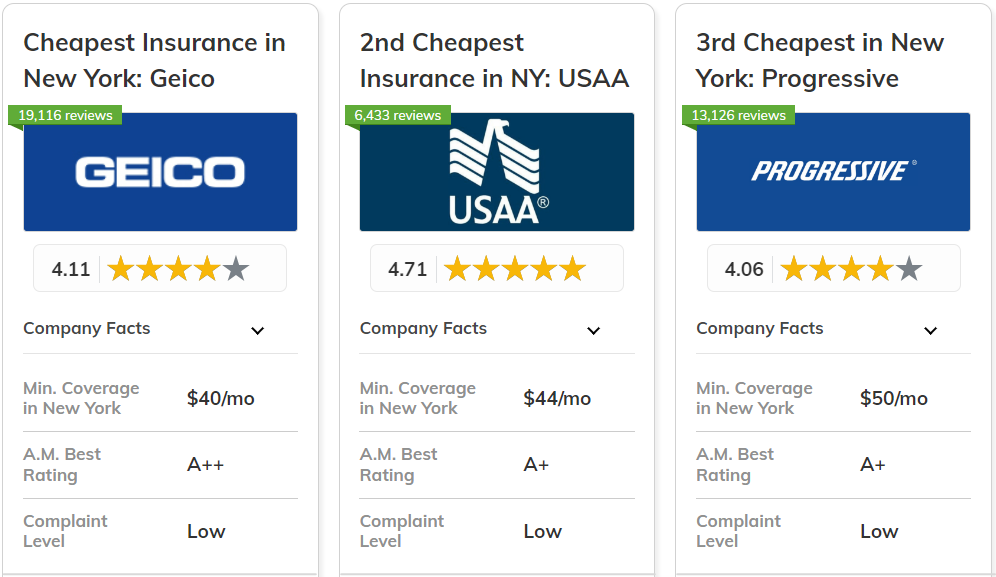

The most effective strategy for finding affordable car insurance is to actively shop around and compare quotes from multiple insurance providers. Insurers in New York have different pricing models and discount structures. What might be a competitive rate with one company could be significantly higher with another.

The Importance of Regular Comparison

It’s advisable to compare quotes at least once a year, or whenever you experience a significant life change, such as moving to a new address, purchasing a new vehicle, or having a change in your driving record. Many online comparison tools and independent insurance agents can assist you in navigating this process efficiently.

Understanding Different Policy Types

Beyond just comparing prices, it’s crucial to understand the different policy types and coverage levels offered by each insurer. Ensure you are comparing apples to apples, meaning you are looking at similar coverage limits and deductibles when evaluating quotes. Don’t be afraid to ask questions to clarify any terms or coverage details.

Maximizing Discounts

Insurance companies offer a wide array of discounts designed to reward safe driving habits, loyal customers, and specific lifestyle choices. Diligently exploring and applying for all eligible discounts can lead to substantial savings.

Common Discounts in New York

- Good Driver Discount: For drivers with a clean record over a specified period.

- Multi-Policy Discount: Bundling your auto insurance with other policies, such as homeowners or renters insurance, from the same provider.

- Multi-Car Discount: Insuring multiple vehicles with the same company.

- Good Student Discount: For young drivers who maintain a strong academic record.

- Defensive Driving Course Discount: Completing an approved defensive driving course can lower your premium. This is particularly beneficial in New York for ticket dismissal and insurance reduction.

- Low Mileage Discount: For drivers who drive fewer miles annually.

- Vehicle Safety Features Discount: For cars equipped with anti-theft devices or advanced safety features.

- Payment Discounts: Discounts may be offered for paying your premium in full or setting up automatic payments.

Negotiating Your Premium

While not always explicitly advertised, some insurers may be open to negotiation, especially if you present them with competitive quotes from other companies. Being a loyal customer with a good payment history can also give you leverage.

Adjusting Your Coverage

Reviewing your current coverage needs and making appropriate adjustments can also lead to significant savings.

Assessing Your Needs

Carefully consider whether you still need comprehensive and collision coverage on older vehicles. If the value of your car is low, the cost of these coverages might outweigh the potential payout in the event of a total loss.

Raising Deductibles

As mentioned earlier, increasing your deductibles on comprehensive and collision coverage can lower your premiums. However, ensure you have the financial capacity to cover the higher deductible should you need to file a claim.

The Nuances of New York’s Auto Insurance Landscape

New York’s insurance market is shaped by its unique regulatory environment and the specific challenges faced by its drivers. Understanding these nuances can provide valuable context for the costs you encounter.

No-Fault Insurance Explained

New York operates under a “no-fault” insurance system. This system is designed to expedite the claims process and reduce litigation by requiring each driver’s insurance to cover their own medical expenses and lost wages up to a certain limit, regardless of who was at fault for the accident.

Benefits and Limitations

The primary benefit of no-fault insurance is that it ensures you can access necessary medical care quickly after an accident without waiting for fault to be determined. However, it’s important to understand that no-fault coverage in New York is primarily for economic losses (medical bills and lost earnings). If you sustain a serious injury, such as a fracture, permanent disability, or significant disfigurement, you may still be able to sue the at-fault driver for non-economic damages (pain and suffering). This is why maintaining adequate bodily injury liability coverage for other drivers is still essential, even under a no-fault system.

Beyond the Minimum: Why Higher Limits Matter

The mandatory minimums in New York are a starting point, but they are often insufficient to cover the full costs of a serious accident. The financial repercussions of an at-fault accident can extend far beyond the minimum liability limits.

Protecting Your Assets

If you cause an accident that results in significant bodily injury or property damage, and the damages exceed your policy limits, your personal assets—your savings, property, and even future earnings—could be at risk to cover the difference. Therefore, investing in higher liability limits provides a crucial layer of financial protection for your assets.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

The UM/UIM coverage is particularly vital in New York, where a significant number of drivers may operate without insurance or with the bare minimum. Adequate UM/UIM coverage ensures you and your passengers are protected if you’re involved in an accident with such drivers.

Conclusion: Navigating the Path to Affordable Coverage in New York

The cost of car insurance in New York is a dynamic figure, influenced by a complex web of individual factors, vehicle characteristics, and state-specific regulations. While the average premiums may appear high, a proactive and informed approach can lead to significant savings. By understanding the core components that drive insurance costs—your driving record, personal demographics, vehicle details, and chosen coverage levels—you are empowered to make informed decisions.

The key to securing affordable car insurance in New York lies in diligent research, consistent comparison shopping, and a commitment to safe driving practices. Regularly reviewing your policy, exploring all available discounts, and considering adjustments to your coverage can unlock substantial savings. Furthermore, comprehending the nuances of New York’s no-fault system and the importance of robust liability and UM/UIM coverage ensures you are not only compliant but also adequately protected against the unpredictable nature of the road. Ultimately, by being an engaged and informed consumer, you can navigate the complexities of New York’s auto insurance market and find coverage that offers both peace of mind and financial prudence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.