When someone asks, “How much is a Google?” they might be looking for a mathematical definition of a “googol” (the number 1 followed by 100 zeros), but in the modern economic landscape, the question almost always refers to the financial valuation of Alphabet Inc., the parent company of the world’s most dominant search engine. Determining the value of such a gargantuan entity requires more than a simple look at a stock ticker; it necessitates an analysis of market capitalization, revenue streams, asset portfolios, and future growth potential in the era of artificial intelligence.

As of the current fiscal landscape, Google (Alphabet) consistently sits within the elite “Trillion Dollar Club,” a small group of tech titans whose individual valuations exceed the GDP of most nations. To understand how much Google is truly worth, we must dissect the financial machinery that powers its dominance.

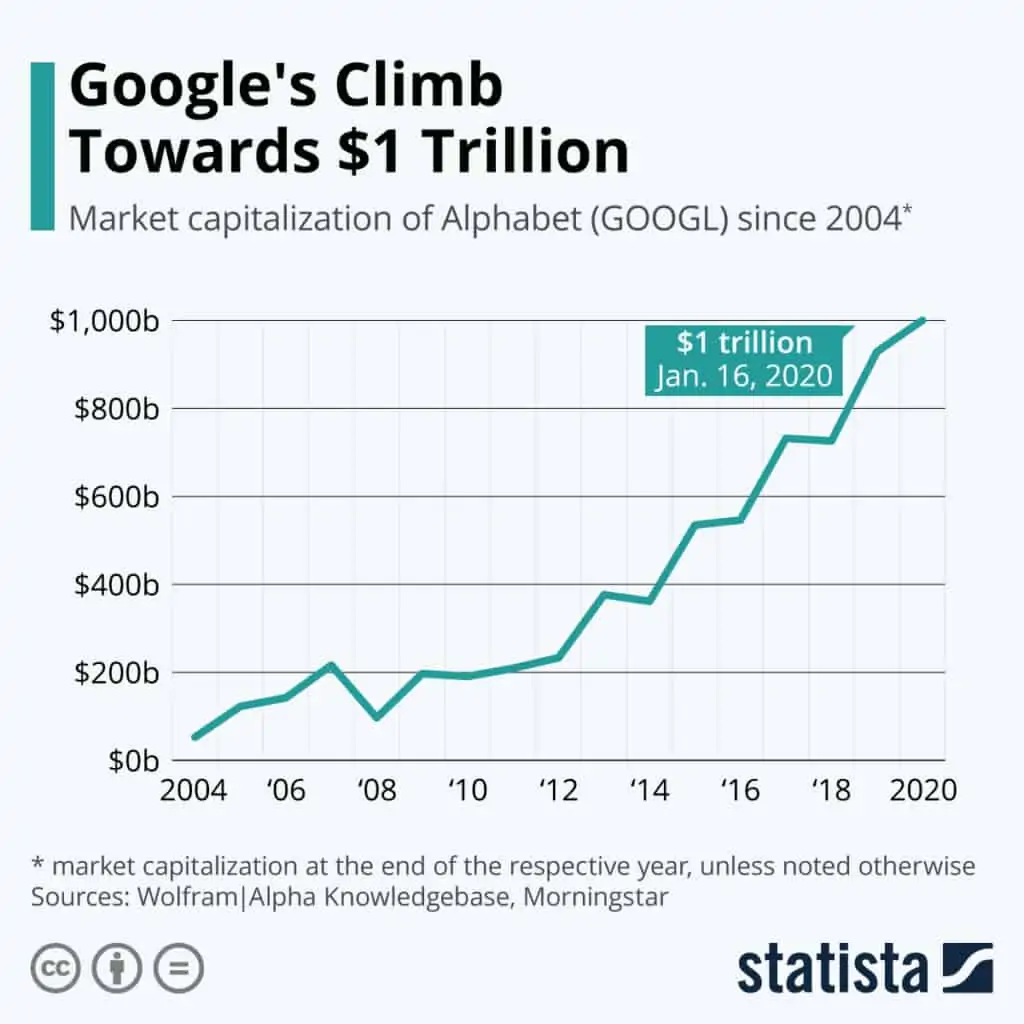

The Architecture of Alphabet’s Market Capitalization

Market capitalization is the most common metric used to answer “how much” a company is worth. It is calculated by multiplying the total number of outstanding shares by the current market price of a single share. For Alphabet Inc., this figure typically fluctuates between $1.6 trillion and $2 trillion, depending on market sentiment and quarterly earnings reports.

Market Cap vs. Enterprise Value

While market cap tells us the equity value, Enterprise Value (EV) provides a more comprehensive picture of the “takeover price.” EV accounts for the company’s total debt and subtracts its massive cash reserves. Because Alphabet maintains one of the cleanest balance sheets in corporate history—often holding over $100 billion in cash and marketable securities—its Enterprise Value is frequently lower than its market cap. This high liquidity makes the company incredibly resilient to economic downturns, allowing it to self-fund massive research and development (R&D) projects without relying on external high-interest debt.

Share Classes and Investor Influence

To understand Google’s financial structure, one must distinguish between its share classes: GOOGL (Class A) and GOOG (Class C). Class A shares carry voting rights, while Class C shares do not. There are also Class B shares, held primarily by the founders, Larry Page and Sergey Brin, which carry ten votes per share. This structure ensures that while the “value” of the company is distributed among global investors, the strategic control remains concentrated. For an investor, the “cost” of a Google share is a gateway into a diversified ecosystem that behaves more like an index fund of the internet than a single product company.

Revenue Engines: What Drives the Trillion-Dollar Valuation?

A company is worth only as much as its ability to generate future cash flows. Google’s valuation is anchored by a diverse set of “engines” that convert user attention and data into cold, hard currency.

The Advertising Hegemony: Search and YouTube

At its core, Google is an advertising powerhouse. Roughly 75% to 80% of its total revenue is derived from Google Search, YouTube ads, and the Google Network. Google Search remains a “natural monopoly,” capturing over 90% of the global search market. This dominance creates an incredibly wide “moat”—a competitive advantage that makes it nearly impossible for rivals to gain a foothold.

YouTube, acquired for a mere $1.65 billion in 2006, is now one of the most valuable media assets on the planet. If YouTube were a standalone company, analysts estimate it would be worth between $300 billion and $400 billion. Its transition from a simple video-hosting site to a subscription-based (YouTube Premium) and ad-supported behemoth is a primary driver of Alphabet’s high valuation multiples.

Google Cloud: The Path to Profitability

For years, Google Cloud was a “loss leader,” a segment where the company spent billions to compete with Amazon Web Services (AWS) and Microsoft Azure. However, in recent years, Google Cloud has pivoted to profitability. As enterprises migrate their data and operations to the cloud, this segment has become the fastest-growing part of Alphabet’s portfolio. The market values this segment highly because cloud revenue is “sticky”—once a corporation integrates Google’s infrastructure, the cost of switching is prohibitively high, ensuring a steady stream of recurring revenue.

Intrinsic Valuation and Financial Performance Metrics

To move beyond the surface-level market cap, financial analysts look at intrinsic valuation—the “true” value based on fundamental financial health. This involves looking at Price-to-Earnings (P/E) ratios, free cash flow, and operating margins.

Analyzing the P/E Ratio and Investor Sentiment

Alphabet generally trades at a P/E ratio that reflects its status as a “Growth” stock, though it is increasingly viewed as a “Value” play due to its stability. A P/E ratio essentially tells you how much investors are willing to pay for every dollar of profit. Compared to other “Magnificent Seven” stocks like Nvidia or Tesla, Google often trades at a more conservative multiple. This suggests that while the company is worth trillions, the market may occasionally undervalue its long-term potential, particularly regarding its integration of AI into its core search product.

Free Cash Flow and Capital Allocation

One of the most impressive aspects of Google’s valuation is its ability to generate Free Cash Flow (FCF). Alphabet generates tens of billions of dollars in FCF every quarter. This excess cash allows the company to engage in massive share buybacks. By reducing the number of shares outstanding, the company increases the value of each remaining share, effectively boosting the “price” of Google without needing to increase its total market cap. This strategy of “returning capital to shareholders” is a hallmark of a mature, financially healthy corporation.

The Risks and Variables of Future Valuation

No valuation is static. The “cost” of Google today is a reflection of what the market thinks it will be worth tomorrow. Several factors could either skyrocket Alphabet’s valuation or significantly erode it.

Regulatory Pressure and Antitrust Challenges

The greatest threat to Google’s valuation is not competition, but regulation. The U.S. Department of Justice (DOJ) and the European Union have repeatedly targeted Google for its dominance in search and advertising technology. There are ongoing discussions about the potential “breakup” of Alphabet. Paradoxically, some analysts argue that a breakup could actually increase the company’s total value. If YouTube, Google Cloud, and Google Search were spun off into separate companies, the sum of their parts might exceed the current $1.8 trillion market cap, as “pure-play” companies often command higher valuations than conglomerates.

The AI Arms Race: Innovation vs. Disruption

The emergence of Generative AI, spearheaded by OpenAI’s ChatGPT and Microsoft’s Bing AI, has introduced a new variable. For the first time in two decades, Google’s core Search business faces a conceptual threat. If users shift from “searching for links” to “receiving AI answers,” Google’s traditional ad model could be disrupted.

However, Google’s investment in its own AI models (like Gemini) and its proprietary TPU (Tensor Processing Unit) chips suggest that it is well-positioned to lead this transition. The valuation of Google in the next decade will depend heavily on its ability to monetize AI as effectively as it has monetized Search. If Google successfully integrates AI into its Workspace and Cloud suites, its valuation could easily challenge the $3 trillion mark currently held by Microsoft and Apple.

![]()

Conclusion: The True Value of a Global Utility

So, how much is “a Google”? On paper, it is a $1.8 trillion collection of code, data centers, and intellectual property. In reality, it is a global utility that has become inseparable from the modern economy.

Its value is not merely in the dollars it generates today, but in its role as the primary gateway to the world’s information. From a financial perspective, Google’s worth is anchored by its unmatched advertising machine, its burgeoning cloud business, and a cash reserve that provides a safety net few other companies can imagine. While regulatory hurdles and AI-driven disruption pose legitimate risks, the company’s fundamental financial health remains robust.

For investors and observers alike, “Google” represents more than just a search bar; it is a financial titan whose valuation serves as a barometer for the health of the digital age. Whether its market cap fluctuates by a few hundred billion in either direction, its intrinsic value as an architect of the internet remains a cornerstone of the global financial market.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.