In the bustling landscape of digital payments, Venmo has carved out a significant niche, becoming synonymous with quick and convenient peer-to-peer (P2P) money transfers. Whether it’s splitting a dinner bill, collecting rent from roommates, or sending a quick gift, Venmo’s ease of use has made it a go-to financial tool for millions. However, as with any financial service, a common and crucial question looms in the minds of users: “How much does Venmo charge?” Understanding Venmo’s fee structure is not just about avoiding unexpected costs; it’s a vital component of smart personal and business finance, ensuring that the convenience doesn’t come at an unforeseen premium.

For the most part, Venmo proudly promotes its core service as free, and indeed, many common transactions incur no charge. But like an iceberg, a significant portion of its fee structure lies beneath the surface, applicable only in specific scenarios that, if ignored, can incrementally chip away at your financial goals. This comprehensive guide will demystify Venmo’s charges, highlight cost-saving strategies, and place its fee model within the broader context of modern financial tools, empowering you to use the platform both effectively and economically.

Understanding Venmo’s Core Services and Free Transactions

At its heart, Venmo is designed to make sending and receiving money among friends and family effortless and, crucially, free for its most basic functions. This “free” model is what has largely fueled its widespread adoption and integrated it into the daily financial habits of a generation.

Standard Peer-to-Peer Payments

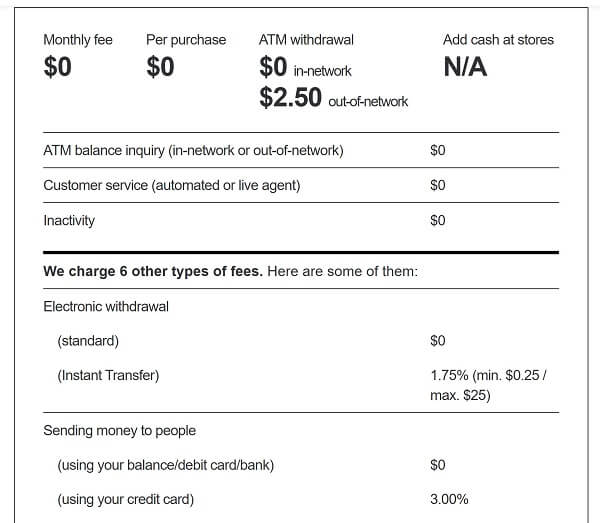

The foundational promise of Venmo is its free P2P payments. When you send money to another Venmo user using funds from your linked bank account, your Venmo balance, or a debit card, you will not incur any transaction fees. This covers the vast majority of personal transactions, such as splitting a restaurant tab, contributing to a group gift, or sending money to a family member. It’s this seamless, no-cost transfer mechanism that allows for spontaneous financial interactions without the friction of traditional banking. The convenience here is paramount, allowing users to settle debts and share expenses without worrying about small charges adding up.

Receiving Money

On the flip side, receiving money into your Venmo balance is always free, regardless of how the sender funded the payment. Whether a friend sent you money from their Venmo balance, bank account, or even a credit card, the amount you receive will be the full sum sent. This principle extends to payments from business profiles as well; while the sender (if a business) might pay a fee, the recipient’s balance reflects the gross amount. This makes Venmo a popular way for individuals to collect money without any personal cost.

Venmo Debit Card and Credit Card Usage

Venmo has expanded its offerings beyond simple P2P transfers, introducing its own debit and credit cards.

- Venmo Debit Card: This card allows you to spend your Venmo balance anywhere Mastercard is accepted. Using the Venmo Debit Card for purchases incurs no fees from Venmo itself. It functions much like any other debit card, drawing directly from your Venmo balance. If your balance runs low, you can typically set it to draw from a linked bank account, still without Venmo fees for the transaction itself, though standard bank fees might apply for overdrafts if not managed.

- Venmo Credit Card: This card is a more traditional credit product, offering rewards on purchases. While using the Venmo Credit Card for purchases doesn’t incur Venmo transaction fees for the purchase itself, it operates under the standard credit card model with potential interest charges if balances aren’t paid in full, and specific fees like late payment fees or cash advance fees (which we’ll touch upon later). It’s important to differentiate the fees associated with the credit card product from the P2P app’s transaction fees.

When Venmo Charges a Fee: Identifying Cost Triggers

While many services are free, Venmo, like any robust financial platform, needs to generate revenue to cover operational costs, maintain security, innovate, and provide customer support. This is where specific charges come into play, primarily linked to methods that involve higher processing costs for Venmo or offer enhanced convenience. Knowing these specific triggers is crucial for optimizing your Venmo usage for cost-efficiency.

Instant Transfers to Bank Accounts

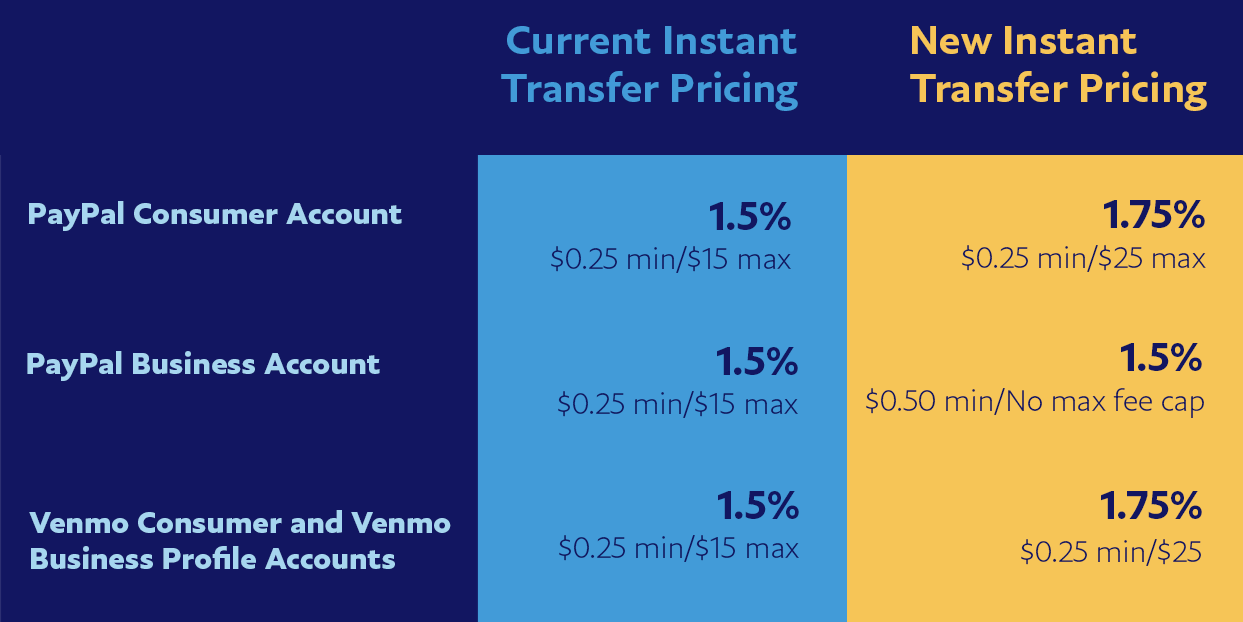

One of the most common scenarios where Venmo levies a fee is for instant transfers of your Venmo balance to a linked bank account or eligible debit card. While standard transfers, which typically take 1 to 3 business days to process, are free, the instant gratification of immediate access to your funds comes at a cost.

- Fee Structure: Venmo charges 1.75% of the transferred amount, with a minimum fee of $0.25 and a maximum fee of $25.

- Example: If you transfer $100 instantly, the fee would be $1.75. If you transfer $500, the fee would be $8.75. If you transfer $20,000, the fee would hit its $25 cap.

This fee reflects the real-time processing costs and the value of immediate liquidity that Venmo provides, bypassing the standard Automated Clearing House (ACH) network’s processing times. For users who frequently need immediate access to their funds, this fee becomes a recurring consideration.

- Example: If you transfer $100 instantly, the fee would be $1.75. If you transfer $500, the fee would be $8.75. If you transfer $20,000, the fee would hit its $25 cap.

Credit Card Funding for P2P Payments

This is a significant fee trigger for many users. While using a debit card or bank account to send money is free, Venmo charges a fee when you use a linked credit card to fund a P2P payment.

- Fee Structure: There is a 3% fee for sending money to friends and family using a credit card.

- Example: If you send $100 to a friend using your credit card, Venmo will charge you an additional $3. You’ll likely see the transaction on your credit card statement as $103.

This fee is directly related to the interchange fees that credit card networks charge to process transactions. Venmo passes this cost on to the user, as accepting credit card payments is more expensive for them than debit card or bank transfers. It’s an important distinction often overlooked by users who primarily link their credit cards for convenience.

- Example: If you send $100 to a friend using your credit card, Venmo will charge you an additional $3. You’ll likely see the transaction on your credit card statement as $103.

Business Profiles and Goods & Services Transactions

As Venmo has expanded into enabling small businesses and freelancers to accept payments, a fee structure has been implemented for commercial transactions. These fees are designed to cover the additional processing costs, fraud protection, and features associated with business accounts.

- For Payments Marked as Goods & Services: When a sender specifically marks a payment as “goods and services” (a feature intended for buyer and seller protection), the recipient (seller) is charged a fee.

- For Payments to Business Profiles: When you receive a payment through a Venmo Business Profile, the business automatically incurs a fee.

- Fee Structure: Currently, the fee for receiving payments for goods and services or through a business profile is 1.9% + $0.10 per transaction.

- Example: If a customer pays your business $50 through Venmo, you would receive $50 minus the fee ($0.95 + $0.10 = $1.05), so your net would be $48.95.

This fee is crucial for small businesses to factor into their pricing and revenue calculations. It’s Venmo’s way of monetizing its platform for commercial use, offering payment processing capabilities that rival traditional merchant services at competitive rates for smaller transactions.

- Example: If a customer pays your business $50 through Venmo, you would receive $50 minus the fee ($0.95 + $0.10 = $1.05), so your net would be $48.95.

Venmo Credit Card Cash Advance Fees

While not directly a P2P app fee, if you possess a Venmo Credit Card, it’s worth noting that using it for a cash advance will incur specific fees from the credit card issuer (Synchrony Bank). Cash advances typically come with higher interest rates and immediate fees, distinct from standard purchase interest. This falls under the realm of traditional credit card finance rather than Venmo’s transaction services, but it’s part of the broader financial ecosystem Venmo offers.

Navigating Venmo Like a Pro: Cost-Saving Strategies

Understanding Venmo’s fee triggers is the first step; the next is to implement strategies that minimize your costs. By making conscious choices about how you fund your payments and manage your Venmo balance, you can ensure that this convenient app remains an economically smart choice for your financial interactions.

Prioritize Bank Account & Debit Card Funding

This is the golden rule for avoiding fees on P2P payments. Always default to funding your Venmo transactions using your linked bank account or a debit card. These methods are free for sending money and should be your primary choice for personal transfers. If you consistently use a credit card for personal payments, those 3% fees can quickly accumulate, turning small conveniences into significant expenses over time.

Opt for Standard Bank Transfers

Unless you absolutely need immediate access to funds from your Venmo balance, choose the free standard transfer option to your bank account. While it requires a bit of patience (typically 1-3 business days), it completely bypasses the 1.75% instant transfer fee. For most users, planning a day or two ahead for transfers can save a substantial amount over the course of a year, especially for larger sums. Consider when you truly need the money in your bank account versus when it can wait.

Distinguish Personal vs. Business Payments

If you’re a freelancer, a small business owner, or frequently receive payments for goods or services, ensure you’re using a Venmo Business Profile for these transactions. This clearly delineates commercial activity and provides appropriate buyer/seller protections. Conversely, avoid marking personal payments as “goods and services” if they are truly just splitting costs with friends, as this unnecessarily triggers the 1.9% + $0.10 fee for the recipient. Clarity and honesty in transaction labeling benefit all parties and ensure correct fee application.

Monitor Your Venmo Balance

Keep an eye on your Venmo balance. If you frequently receive money, you can use your accumulated balance to make future payments to friends and family without incurring any funding fees. This essentially creates a free-to-use digital wallet within the Venmo ecosystem. By spending your Venmo balance first, you reduce the need to draw from linked bank accounts, debit cards, or, most importantly, credit cards for new payments.

Leverage the Venmo Debit Card

For those who regularly have a Venmo balance, the Venmo Debit Card can be a fantastic, fee-free way to spend your funds. Rather than transferring your balance to your bank account (and potentially paying an instant transfer fee), you can directly use the debit card for purchases at any merchant that accepts Mastercard. This provides immediate utility for your Venmo funds without any additional charges from Venmo itself.

The Financial Context: Why Venmo Charges Fees

Understanding why Venmo charges fees provides deeper insight into its business model and the broader economics of digital payments. These charges aren’t arbitrary; they are strategically implemented to sustain the platform and deliver value.

Sustaining a Free Service Model

Venmo’s core P2P service being free is a massive user acquisition and retention strategy. However, maintaining a secure, reliable, and constantly evolving platform costs money. Fees on specific services, like instant transfers or business transactions, allow Venmo to generate revenue without charging every user for every single transaction. This tiered approach ensures that the most basic, high-volume interactions remain free, appealing to a wide user base, while monetizing premium features or higher-cost services.

Payment Processing Costs

A significant driver of Venmo’s fees is the underlying cost of payment processing. When you use a credit card to send money, Venmo pays an “interchange fee” to the card-issuing bank and other network fees. Similarly, instant bank transfers often involve real-time payment networks that charge a premium compared to slower, batch-processed ACH transfers. Venmo passes these specific costs on to the user to avoid operating at a loss on these transactions. It’s an industry standard that digital payment processors levy fees for services that incur higher processing expenses.

Value Proposition of Speed and Convenience

The instant transfer fee is a prime example of paying for speed and convenience. In today’s fast-paced world, immediate access to funds can be critical for many users. Venmo offers a solution that bypasses the traditional banking delays, and the fee reflects the value of that immediacy. For users who prioritize speed, the fee is a small price to pay for bypassing a several-day waiting period. This is a common model across various financial services, where expedited access or enhanced features come with a premium.

Venmo’s Role in Modern Personal and Business Finance

Venmo has evolved beyond a simple app for splitting bills; it’s become an integral part of many people’s financial lives, blurring the lines between personal and informal business transactions. Understanding its fee structure is critical to harnessing its full potential within your overall financial strategy.

Convenience vs. Cost: A Constant Trade-off

The fundamental dilemma for Venmo users is the balance between convenience and cost. The app offers unparalleled ease for many transactions. However, this convenience sometimes comes with a price tag, particularly for instant gratification or specific funding methods. Smart financial management involves recognizing these trade-offs and consciously choosing options that align with your financial priorities. For some, the instant transfer fee is a worthwhile expense; for others, the three-day wait for a free transfer is perfectly acceptable.

Integrating with Budgeting

For both personal users and small businesses, Venmo fees, though sometimes small individually, can add up. If you frequently use instant transfers or credit card funding, these charges need to be accounted for in your budgeting. Small businesses, in particular, must factor in the 1.9% + $0.10 fee for commercial transactions when setting prices or evaluating profit margins. Integrating Venmo’s potential costs into your financial planning ensures that the convenience doesn’t erode your financial health.

Beyond P2P: Venmo as a Financial Ecosystem

Venmo is continually expanding its services, from the Venmo Debit and Credit Cards to crypto features and even QR code payments for in-store purchases. As it grows into a broader financial ecosystem, understanding its charges becomes even more complex but also more critical. Each new feature introduces its own set of potential fees or benefits, underscoring the need for users to stay informed about how they interact with the platform. This expansion demonstrates Venmo’s ambition to be more than just a payment app, aiming to be a holistic financial tool, with a corresponding diversified revenue model.

Conclusion

At its core, Venmo remains a remarkably convenient and largely free tool for personal peer-to-peer payments when funded correctly. However, the question “how much does Venmo charge?” is nuanced, with fees primarily triggered by actions that incur higher processing costs for the platform or offer premium benefits like immediate access to funds.

By understanding the distinct scenarios where Venmo applies fees – specifically, instant transfers (1.75%), credit card funding for P2P payments (3%), and business/goods & services transactions (1.9% + $0.10) – users can make informed decisions. Prioritizing bank account or debit card funding, opting for standard transfers when time allows, and correctly categorizing payments are simple yet effective strategies to minimize costs. In the broader context of personal and business finance, navigating Venmo’s fee structure isn’t just about saving a few dollars; it’s about exercising financial literacy and making deliberate choices that align with your economic goals, ensuring that this powerful digital tool serves you as efficiently and affordably as possible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.