Planning a cruise is often perceived as a simple purchase of a vacation package, but from a financial perspective, it is a complex exercise in budgeting and value assessment. Unlike a standard hotel stay, a cruise represents a multifaceted financial commitment that includes transportation, lodging, dining, and entertainment, often governed by dynamic pricing models. To truly answer the question, “How much does it cost for a cruise?” one must look beyond the initial sticker price and analyze the “all-in” cost of ownership for the duration of the voyage.

In this financial guide, we will break down the cost structures of modern cruising, explore the hidden variables that impact your final invoice, and provide a framework for strategic financial planning to ensure your maritime investment delivers the highest possible return on experience.

1. Decoding the Base Fare: Analyzing the Primary Financial Outlay

The base fare is the most visible component of a cruise’s cost, yet it is rarely the final amount a traveler pays. In the personal finance world, the base fare should be viewed as the “entry cost”—the minimum capital required to secure a position on the vessel. Understanding how this price is structured is essential for accurate budgeting.

Interior vs. Suite: The Real Estate of the Ocean

Cruise lines operate on a tiered pricing model similar to real estate. The cost per square foot varies significantly based on location, view, and amenities.

- Interior Cabins: Often the “loss leader” for cruise lines, these provide the lowest barrier to entry. They are ideal for budget-conscious travelers who prioritize the destination over the dwelling.

- Balcony Cabins: Representing the mid-tier market, these cabins command a premium (often 30-50% higher than interiors) but offer significantly higher psychological value.

- Suites and Luxury Enclaves: This is the high-net-worth segment of cruising. These accommodations can cost five to ten times the base fare of an interior room but often include “all-inclusive” perks that mitigate secondary spending.

Inclusions and Exclusions: Avoiding “Sticker Shock”

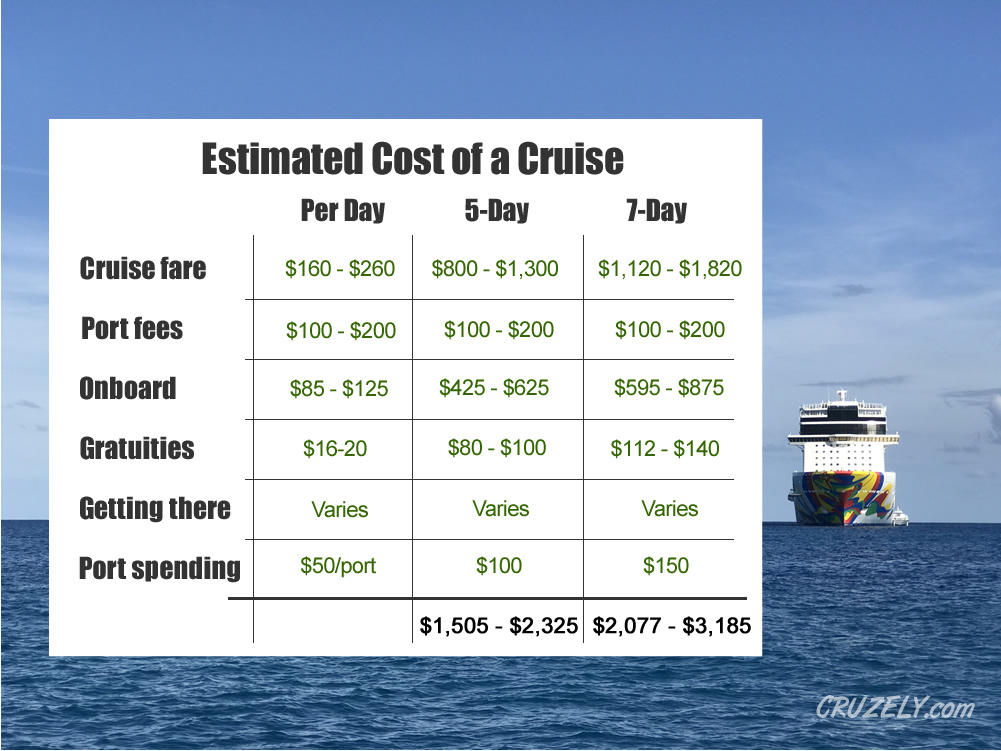

A critical step in financial due diligence is identifying what the base fare actually covers. Traditionally, a cruise fare includes your room, basic meals in the main dining room and buffet, and standard entertainment. However, the modern “Money” perspective on cruising requires a closer look at the “add-ons.” Taxes, port fees, and regulatory charges are rarely included in the initial advertised price and can add $150 to $500 per person to the total bill, depending on the itinerary.

Market Volatility and Dynamic Pricing

Cruise pricing is a masterpiece of yield management. Prices fluctuate based on supply and demand, seasonal trends (peak summer vs. shoulder season), and how far in advance the booking occurs. From a financial standpoint, booking 12 to 18 months in advance often secures the lowest price, while “last-minute” deals (within 90 days) can offer high value if the cruise line is struggling to fill inventory.

2. Beyond the Ticket: Managing Variable and Hidden Expenses

The “hidden” costs of a cruise are where many travelers find their budgets collapsing. To maintain fiscal discipline, one must account for the secondary revenue streams that cruise lines rely on to maintain their profit margins.

Gratuities and Service Charges

Most major cruise lines automatically apply a daily gratuity or service charge to your onboard account. This typically ranges from $16 to $23 per person, per day. For a family of four on a seven-night cruise, this represents an additional $450 to $650 expense that is often overlooked in initial estimates. From a personal finance perspective, it is best to pre-pay these fees to “lock in” the cost and avoid a large bill on the final morning of the trip.

Shore Excursions and Ports of Call

The cruise is merely the vessel; the destinations are the product. Shore excursions can range from $50 for a basic city tour to over $500 for a private helicopter excursion or specialized adventure. If you do not budget for excursions, you risk “port paralysis,” where the cost of leaving the ship exceeds your liquid budget for the day. A savvy financial move is to research third-party excursion providers, which often offer identical experiences for 20-30% less than the cruise line’s proprietary tours.

Premium Amenities: Dining and Beverage Packages

The “upsell” is a core component of the cruise business model. Specialty dining (steakhouses, sushi, French bistros) usually carries a cover charge of $35 to $90 per person. Similarly, beverage packages—covering alcohol, specialty coffees, and bottled water—can cost $60 to $110 per day.

Before purchasing a beverage package, perform a “break-even analysis.” If you do not consume at least five to seven alcoholic beverages daily, paying “a la carte” is almost always the more fiscally responsible choice.

3. Strategic Financial Planning: Maximizing Value and ROI

Investing in a cruise requires the same level of scrutiny as any other significant discretionary expenditure. By applying financial strategies, you can reduce your total cost of ownership without sacrificing the quality of the experience.

Timing the Market: The Economics of the “Shoulder Season”

The “when” of your cruise is just as important as the “where.” Cruising during the “shoulder seasons”—the periods just before or after peak travel times—can result in savings of 40% or more. For example, cruising the Caribbean in September (hurricane season, requiring insurance) or Alaska in May (cooler weather) offers the same ship and same amenities for a fraction of the July price.

Travel Insurance: Protecting Your Financial Asset

In the context of personal finance, a cruise is a pre-paid asset. If you are forced to cancel, that asset can depreciate to zero instantly without protection. Travel insurance should be viewed as a mandatory “hedging” strategy. Look for policies that include “Cancel for Any Reason” (CFAR) and robust medical evacuation coverage. While this adds 5-10% to your total cost, it protects you against the total loss of your investment.

Loyalty Programs and Financial Arbitrage

Most cruise lines have tiered loyalty programs that offer “dividends” in the form of free laundry, internet minutes, or even free cruises after a certain number of nights. Additionally, using co-branded credit cards or purchasing “Onboard Credit” (OBC) through shareholder benefits (if you own a certain amount of the cruise line’s parent company stock, such as Carnival Corp or Royal Caribbean Group) can provide an immediate return on your spending.

4. The Total Cost of Ownership: Estimating Your All-In Budget

To provide a clear financial picture, we must categorize cruises into different “spend profiles.” This allows you to align your vacation goals with your financial reality.

The Budget Traveler Profile

- Target Spend: $100–$150 per person, per day.

- Strategy: Booking interior cabins, sticking to included dining, and self-guiding at ports of call. This traveler avoids the beverage package and focuses on the “transportation and lodging” value of the cruise.

- Total for 7 days: ~$1,050 per person.

The Mid-Tier Voyager Profile

- Target Spend: $250–$400 per person, per day.

- Strategy: Balcony cabin, one or two specialty dinners, a mid-range beverage package, and cruise-line-sponsored excursions. This is the most common profile and represents a balance of luxury and cost-consciousness.

- Total for 7 days: ~$2,450 per person.

The Ultra-Luxury/All-Inclusive Profile

- Target Spend: $600–$1,000+ per person, per day.

- Strategy: Booking with luxury lines (e.g., Silversea, Regent Seven Seas). While the initial price is high, the “all-in” cost is often more predictable because airfare, excursions, fine wines, and tips are included in the fare. For a high-net-worth individual, this simplifies the accounting and provides a more seamless experience.

- Total for 7 days: ~$5,600+ per person.

Factoring in Pre- and Post-Cruise Logistics

A common financial mistake is forgetting the costs required to actually get to the ship. Airfare, a pre-cruise hotel stay (strongly recommended to avoid missing the ship due to flight delays), and transfers to the port can add $500 to $1,500 to the total project cost. In a holistic budget, these are “non-negotiable” capital expenditures that must be sidelined before the first cruise payment is made.

Conclusion: Is a Cruise a Sound Financial Investment in Leisure?

When analyzed through the lens of personal finance, a cruise offers a unique “bundled value” that is hard to replicate with land-based travel. By consolidating food, transport, and lodging into a single transaction, travelers can achieve a high degree of cost certainty—provided they are disciplined regarding onboard spending.

Ultimately, the cost of a cruise is not just the number on the booking confirmation. It is the sum of the base fare, taxes, gratituties, and discretionary spending, mitigated by strategic timing and loyalty rewards. By approaching a cruise with a professional financial mindset, you can enjoy the vastness of the ocean while keeping your financial house in perfect order. Whether you are looking for a high-ROI budget getaway or a luxury capital outlay, understanding these cost drivers is the key to a successful voyage.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.