Purchasing a vehicle is no longer a simple transaction involving a sticker price and a monthly payment. In the modern era of automotive technology, particularly regarding the transition to electric vehicles (EVs), the financial landscape has shifted toward “Total Cost of Ownership” (TCO). For prospective buyers and financial planners alike, understanding how much a Tesla costs requires a deep dive into capital expenditure, tax incentives, operational savings, and the volatile nature of asset depreciation.

Tesla, as a market leader, has fundamentally changed the pricing model of the automotive industry by adopting a direct-to-consumer approach and frequently adjusting MSRPs (Manufacturer’s Suggested Retail Prices) in response to supply chain fluctuations and interest rate shifts. To determine the true cost of a Tesla, one must look beyond the initial purchase price and analyze the broader economic ecosystem surrounding the brand.

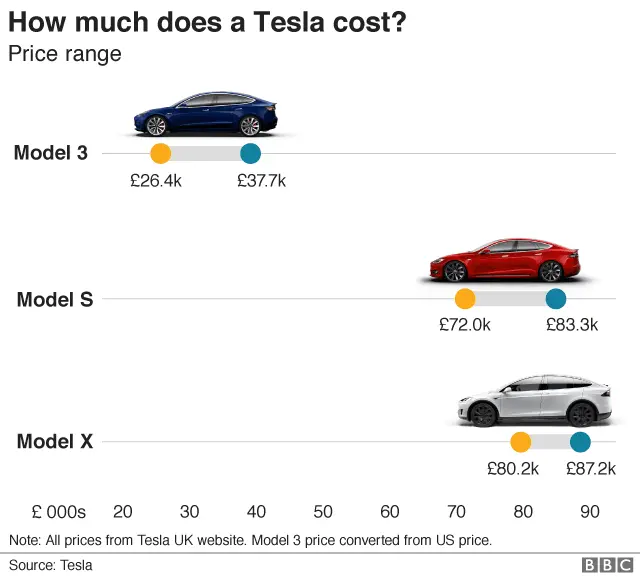

The Upfront Investment: Analyzing Current Model Pricing

The first step in any financial assessment is the initial capital outlay. Tesla’s lineup is strategically segmented to cover both the “mass-market luxury” and “high-end performance” brackets. Unlike traditional dealerships where “haggling” is the norm, Tesla’s pricing is transparent but dynamic, often changing several times within a single fiscal year.

Entry-Level Accessibility: The Model 3 and Model Y

The Model 3 (sedan) and Model Y (compact SUV) represent the core of Tesla’s volume. As of the current market cycle, the Model 3 remains the most accessible entry point into the ecosystem. The “Rear-Wheel Drive” base model typically fluctuates around the $39,000 to $42,000 range. For those requiring longer range or all-wheel drive, the Long Range and Performance variants can push the price toward the $55,000 mark.

The Model Y, which has recently held the title of the world’s best-selling vehicle, commands a premium over the Model 3, generally starting in the mid-$40,000s. Because the Model Y qualifies for specific SUV-class tax incentives that the Model 3 occasionally does not (depending on battery sourcing), the net cost of the Model Y can sometimes be lower than its smaller sibling, making it a fascinating case study in strategic purchasing.

Premium Performance: The Model S and Model X

For the high-net-worth individual or the corporate executive, the Model S (sedan) and Model X (SUV) serve as the flagship assets. These vehicles start significantly higher, often beginning in the $75,000 to $80,000 range. The “Plaid” variants—which offer supercar-level acceleration—can easily exceed $100,000. From a personal finance perspective, these models are subject to higher luxury taxes in certain jurisdictions and represent a much steeper depreciation curve than the mass-market models.

The Impact of Software and Hardware Upgrades

Beyond the physical chassis, Tesla’s “add-on” ecosystem is primarily digital. The most significant financial consideration here is “Full Self-Driving” (FSD) capability. This software suite has historically cost between $8,000 and $15,000 as a one-time purchase, or approximately $99 to $199 per month as a subscription. From an investment standpoint, the one-time purchase is a “sunk cost” that rarely yields a 100% return upon resale, making the subscription model a more fiscally conservative choice for many buyers.

Navigating Incentives and Tax Strategies

One cannot accurately calculate the cost of a Tesla without accounting for government intervention. The global push for electrification has resulted in significant subsidies that act as a direct discount on the purchase price, provided the buyer meets specific criteria.

Federal Tax Credits and the Inflation Reduction Act

In the United States, the Inflation Reduction Act (IRA) has revolutionized EV financing. Many Tesla models qualify for a federal tax credit of up to $7,500. A critical shift in recent years is the “Point of Sale” credit, which allows buyers to transfer the credit to the dealer (Tesla) to reduce the purchase price immediately at the time of delivery, rather than waiting to claim it on a tax return a year later.

However, these credits are subject to strict “Modified Adjusted Gross Income” (MAGI) limits ($150,000 for individuals, $300,000 for joint filers) and “Manufacturer’s Suggested Retail Price” (MSRP) caps ($55,000 for sedans, $80,000 for SUVs). Navigating these caps is essential for maximizing the ROI of the purchase.

State-Level Rebates and Local Savings

Beyond federal aid, states like California, Colorado, and Massachusetts offer additional rebates ranging from $1,500 to $5,000. Furthermore, some municipal utility companies offer credits for installing home charging stations. When stacked, these incentives can reduce the “out-of-door” cost of a Tesla by over $10,000, significantly altering the financial profile of the asset.

Total Cost of Ownership (TCO) vs. Internal Combustion

The true financial “win” of owning a Tesla is found in the operating expenses. While the upfront price may be higher than a comparable gasoline vehicle, the “fuel” and maintenance costs tell a different story over a five-year horizon.

Fuel Savings and the Cost per Mile

The most immediate impact on a monthly budget is the elimination of gasoline. On average, charging a Tesla at home costs about one-third to one-fourth the price of fueling a 30-MPG internal combustion engine (ICE) vehicle. For an individual driving 15,000 miles per year, this can result in annual savings of $1,500 to $2,500, depending on local electricity rates.

It is important to note that “Supercharging” (using Tesla’s high-speed public network) is more expensive than home charging. While still generally cheaper than gas, frequent road-trippers will see a narrower margin of savings compared to those who charge primarily off-peak at home.

Maintenance and Long-Term Reliability

Tesla vehicles have significantly fewer moving parts than traditional cars. There are no oil changes, spark plugs, timing belts, or transmission flushes. This lack of mechanical complexity translates to lower scheduled maintenance costs.

The primary recurring expenses for a Tesla owner are tires, cabin air filters, and windshield wiper fluid. Because Teslas are heavy (due to the battery) and produce high torque, they tend to wear through tires faster than a standard sedan. Owners should budget for a new set of tires every 20,000 to 30,000 miles, which is a significant, albeit predictable, line item in a long-term budget.

Insurance Premiums and Depreciation Realities

One area where Tesla ownership can be more expensive than expected is insurance. Due to the high cost of proprietary parts and the specialized labor required for repairs, insurance premiums for Teslas are often 20% to 30% higher than for comparable ICE vehicles.

Depreciation is another critical factor. While Teslas once held their value better than almost any other car on the market, recent price cuts by the company have led to a more volatile used market. For a buyer looking at a 3-year holding period, the risk of a sudden MSRP drop affecting their resale value is a factor that must be weighed against the operational savings.

Financing and Leasing: Strategic Capital Deployment

Choosing how to pay for a Tesla is as much a financial strategy as choosing which model to buy. With interest rates fluctuating, the “Cash vs. Finance” debate is more relevant than ever.

Loan Structures and Interest Rate Sensitivity

Tesla offers in-house financing, but savvy buyers often find better rates through credit unions. Because Teslas are viewed as high-value assets with a long lifespan (the battery is warrantied for 8 years or 100,000+ miles), many lenders offer extended terms. However, from a wealth-building perspective, the goal should be to avoid “negative equity”—owing more on the car than it is worth—especially given the potential for MSRP adjustments mentioned earlier.

The Lease vs. Buy Dilemma

Leasing a Tesla has become increasingly popular, particularly for the Model 3 and Model Y. A lease provides a “hedge” against technological obsolescence and depreciation. If Tesla releases a revolutionary new battery or sensor suite in three years, a lessee can simply walk away and upgrade.

Furthermore, for business owners, leasing can offer tax advantages as a deductible business expense. However, it is vital to note that Tesla traditionally does not allow lessees to buy out the car at the end of the term (though this policy varies by model and region), meaning the “equity” in the vehicle is lost to the consumer.

Conclusion: The Bottom Line on Tesla Costs

So, how much does a Tesla cost? For a well-informed buyer who maximizes tax credits and home-charging benefits, a $40,000 Model 3 can effectively “cost” the same as a $30,000 Toyota Camry over a five-year period when accounting for fuel, maintenance, and incentives.

However, for the premium buyer who opts for a Model X Plaid with FSD, ignores tax credit income caps, and relies on expensive public charging, the cost is significantly higher than a comparable luxury SUV.

In the final analysis, the cost of a Tesla is not a static number—it is a variable equation. Success in this “Money” niche requires a balance of upfront capital, an understanding of government policy, and a long-term view of operational efficiency. By treating the purchase as a financial asset rather than just a mode of transportation, owners can unlock the true economic potential of the electric revolution.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.