Social Security remains the cornerstone of retirement planning for millions of Americans. While often viewed as a simple monthly check, the mechanics behind how much you can actually make from the Social Security Administration (SSA) are complex, involving decades of earnings history, specific filing ages, and nuanced legislative formulas. For the modern investor and retiree, understanding these variables is not just a matter of curiosity—it is a critical component of personal finance that can result in a difference of hundreds of thousands of dollars over a lifetime.

To truly answer the question of “how much can you make,” one must look beyond the average check and dive into the strategic maneuvers that optimize this guaranteed, inflation-adjusted income stream.

Understanding the Calculation: How the SSA Determines Your Benefit

The journey to determining your Social Security payout begins long before you stop working. The system is designed to replace a portion of your pre-retirement income based on your highest-earning years. However, the math is more sophisticated than a simple percentage.

The Role of Your Top 35 Years of Earnings

The SSA looks at your entire work history, but it only considers your 35 highest-earning years. These earnings are “indexed” to account for changes in average wages over time, ensuring that $20,000 earned in 1985 is weighted appropriately against $80,000 earned in 2023. If you work fewer than 35 years, the SSA enters zeros for the remaining years, which can significantly pull down your average. Conversely, if you work 40 years, your five lowest-earning years are dropped. For those looking to increase their “make” from Social Security, working a few extra years at a peak salary to replace low-earning years from their youth is a primary strategy.

How AIME and PIA Work Together

Once your top 35 years are indexed, the SSA calculates your Average Indexed Monthly Earnings (AIME). This figure is then put through a formula to determine your Primary Insurance Amount (PIA)—the base amount you would receive at your Full Retirement Age (FRA). The formula uses “bend points,” which are designed to be progressive. It replaces a higher percentage of lower earnings and a lower percentage of higher earnings. For 2024, the formula takes 90% of the first portion of your AIME, 32% of the middle portion, and 15% of the earnings above the top bend point. This structure ensures a safety net for lower earners while still rewarding higher lifetime contributions.

The Impact of Inflation and Cost-of-Living Adjustments (COLA)

One of the most valuable aspects of Social Security is the Cost-of-Living Adjustment (COLA). Unlike most private annuities or pensions, Social Security benefits are adjusted annually based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This means that how much you make will actually increase over time to protect your purchasing power against inflation. In years of high inflation, these adjustments can be substantial, providing a unique form of financial security that traditional investment portfolios may struggle to replicate.

Timing Your Claim: When to Start for Maximum Returns

Perhaps the most significant factor in determining your monthly benefit is the age at which you choose to start receiving checks. You can claim as early as age 62, but doing so comes with a permanent cost.

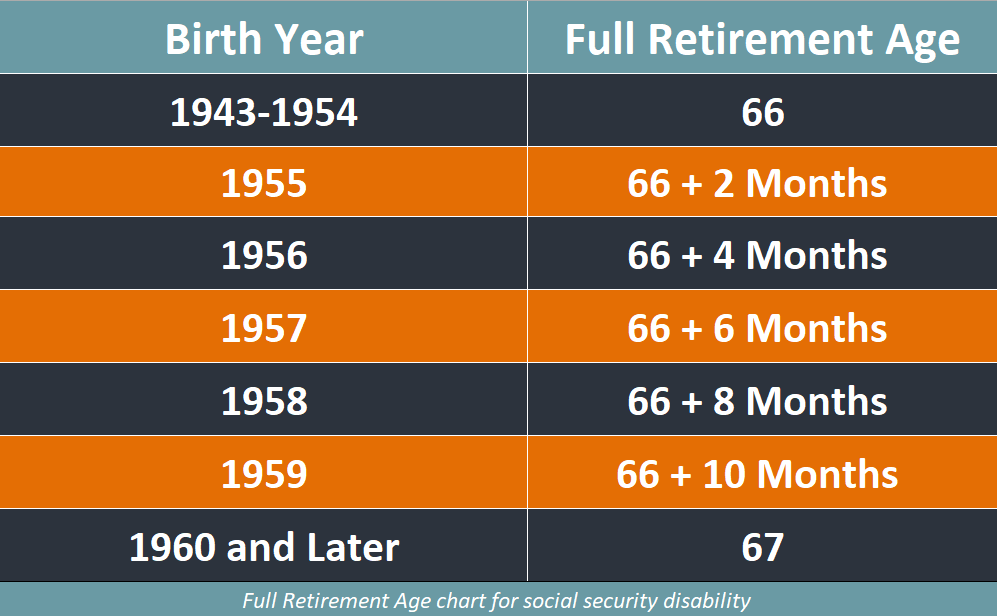

Full Retirement Age (FRA) vs. Early Filing

Your Full Retirement Age is the age at which you are entitled to 100% of your PIA. For anyone born in 1960 or later, the FRA is 67. If you choose to file early at age 62, your monthly benefit is reduced by up to 30%. This reduction is permanent. While filing early provides immediate cash flow, it lowers the “ceiling” of your lifetime income. For individuals with high longevity in their family history, filing at 62 often results in significantly less total wealth accumulated over a lifetime compared to waiting.

The 8% Boost: Waiting Until Age 70

The most powerful tool for increasing your Social Security income is the Delayed Retirement Credit. For every year you wait past your FRA to claim, your benefit increases by approximately 8% per year, up to age 70. There is no incentive to wait past 70, as the credits stop accumulating. By waiting from age 67 to 70, you can increase your monthly check by 24%. In the current financial landscape, finding a guaranteed, inflation-adjusted 8% annual return is nearly impossible in the private market, making this “waiting strategy” one of the most effective personal finance moves available.

Break-Even Analysis: Is Waiting Always Better?

To maximize how much you make, you must consider the “break-even point”—the age at which the total value of higher monthly payments (from waiting) surpasses the total value of smaller payments received earlier. Generally, the break-even age is between 78 and 82. If you expect to live past this window, waiting is mathematically superior. However, personal finance is personal; factors such as immediate health needs, lack of other assets, or a desire to preserve an investment portfolio during a market downturn may lead someone to claim earlier despite the lower monthly figure.

Maximizing Your Payout Through Strategic Planning

The amount you make from Social Security isn’t just about your own work record; it also involves household dynamics and tax efficiency.

Spousal and Survivor Benefit Optimization

Married couples have access to sophisticated strategies. A spouse can claim a “spousal benefit,” which can be up to 50% of the higher-earning spouse’s PIA. If the higher earner waits until 70 to claim, they not only maximize their own check but also ensure a higher “survivor benefit” for the spouse. Upon the death of one partner, the surviving spouse can switch to the higher of the two checks. Coordinating these claims can ensure that the household’s total lifetime draw from the SSA is maximized, providing a vital buffer for the surviving partner.

The Impact of Working While Receiving Benefits

If you claim benefits before your FRA and continue to work, the SSA applies an “earnings test.” For 2024, if you earn more than $22,320, the SSA will withhold $1 in benefits for every $2 you earn above that limit. While these withheld funds are eventually added back to your benefit once you reach FRA, the immediate reduction can be a shock. For those looking to maximize their current income, it is often better to either wait until FRA to claim or keep earnings below the threshold to avoid the temporary withholding.

Tax Implications on Your Social Security Income

Crucially, what you “make” is not always what you keep. Depending on your “provisional income” (adjusted gross income + tax-exempt interest + 50% of Social Security benefits), you may owe federal income taxes on up to 85% of your benefits. High-net-worth individuals or those with significant 401(k) distributions may find that a large portion of their Social Security is taxable. Strategic withdrawals from Roth IRAs or other tax-advantaged accounts can help keep your provisional income lower, effectively increasing the net amount of Social Security that stays in your pocket.

The Future of Social Security: What to Expect

No discussion of how much you can make with Social Security is complete without addressing the long-term solvency of the program.

Solvency Concerns and Potential Legislative Changes

The Social Security Trust Funds are currently projected to be depleted by the mid-2030s. It is important to clarify that “depleted” does not mean the program disappears; rather, it means the incoming payroll taxes would only cover approximately 77% to 80% of scheduled benefits. Historically, Congress has acted to shore up the system through payroll tax increases or adjustments to the FRA. For younger workers, the “how much” might involve a slightly higher retirement age or a different tax structure, making it imperative to treat Social Security as one pillar of a diversified retirement plan, rather than the sole foundation.

Integrating Social Security into a Broader Portfolio

To maximize your total financial health, Social Security should be viewed as the “fixed income” or “bond” portion of your retirement portfolio. Because it is backed by the federal government and adjusted for inflation, it allows investors to be more aggressive with their other assets, such as equities or real estate. By knowing you have a guaranteed floor of income, you can weather market volatility more effectively.

Conclusion: Taking Control of Your Financial Future

How much you make with Social Security is ultimately a result of the choices you make throughout your career and at the point of retirement. By maximizing your earning years, strategically timing your claim, and accounting for spousal benefits and taxes, you can turn a standard government benefit into a high-performing financial asset. In the world of personal finance, Social Security remains one of the few “sure things”—and with the right strategy, it can be the difference between a modest retirement and a prosperous one.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.