Retirement marks a significant life transition, often bringing with it a mix of anticipation and financial considerations. For many, Social Security benefits form a crucial pillar of their retirement income strategy. However, the desire to remain active, pursue new passions, or simply supplement income can lead retirees to wonder: “How much can I make while collecting Social Security without impacting my benefits?” This question is central to sound financial planning for those nearing or in retirement, navigating the complex interplay between work, benefits, and long-term financial security.

Understanding the rules governing earned income while receiving Social Security is not just about avoiding penalties; it’s about strategically maximizing your financial well-being. The Social Security Administration (SSA) has specific regulations designed to balance the purpose of benefits as retirement income with the desire of many individuals to continue working. Misinterpreting these rules can lead to unexpected reductions in benefits, while a clear understanding can empower you to make informed decisions about your work life in retirement. This guide will demystify the earnings limit, explore strategies for optimizing your income, and help you navigate the nuances of working while collecting Social Security.

Understanding Social Security’s Earnings Limit

The core of the matter lies in what the Social Security Administration calls the “earnings test” or “retirement earnings limit.” This rule applies specifically to individuals who claim Social Security benefits before reaching their Full Retirement Age (FRA) and continue to work. Once you reach your FRA, these limits disappear, and you can earn as much as you like without any reduction in your Social Security benefits.

The Basics of the Earnings Test

The earnings test is designed to ensure that Social Security benefits primarily serve as a replacement for lost income due to retirement, rather than as a supplement for those still fully employed. If you are below your FRA and your earnings exceed a certain threshold, the SSA will withhold a portion of your benefits. It’s important to note that only earned income (wages from an employer or net earnings from self-employment) counts towards this limit. Income from investments, pensions, annuities, government retirement benefits, or other sources generally does not affect your Social Security benefits.

The thresholds are adjusted annually for inflation, meaning the specific dollar amounts change from year to year. These limits are crucial because exceeding them triggers a temporary reduction in your benefits. The SSA doesn’t “take away” your benefits permanently; rather, they withhold them for a period.

Different Rules for Different Ages

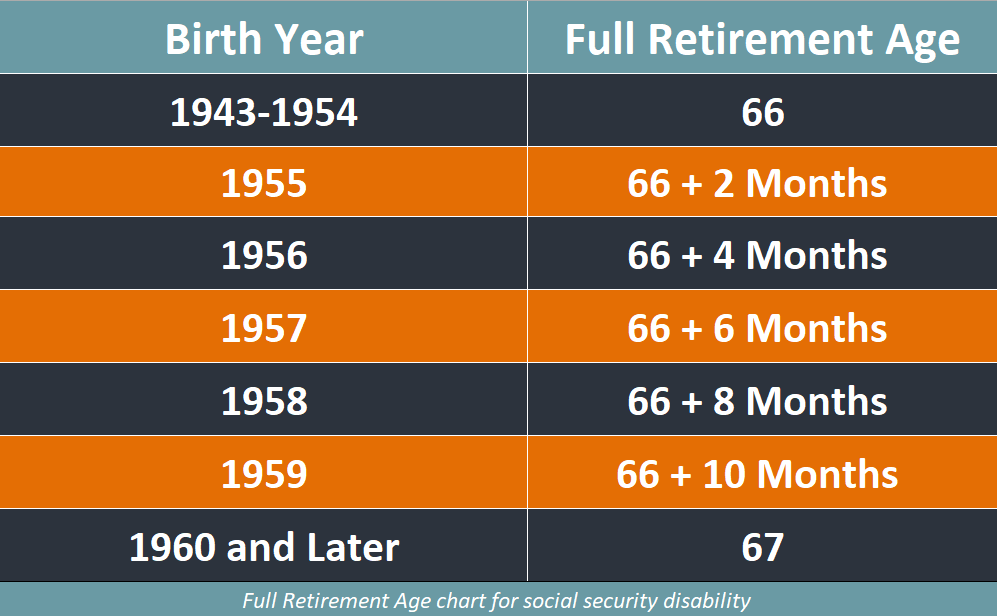

The earnings limit operates differently depending on how close you are to your Full Retirement Age (FRA). Your FRA is determined by your birth year and typically ranges from 66 to 67 years old.

- Before the Year You Reach FRA: If you are collecting benefits and are under your FRA for the entire year, a certain amount of your benefits will be withheld if your earnings exceed the lower annual limit. For every $2 you earn above this limit, $1 will be deducted from your Social Security benefits. This is the most restrictive period for working beneficiaries.

- In the Year You Reach FRA: The rules ease slightly in the calendar year you reach your FRA. A higher annual earnings limit applies, and for every $3 you earn above this limit, $1 will be deducted from your benefits. Crucially, the SSA only counts earnings up to the month before you reach your FRA. From the month you reach FRA onwards, your earnings no longer impact your benefits. This offers a transitional period, allowing for more earnings without significant benefit reduction as you approach your FRA.

- Once You Reach Full Retirement Age: This is the golden milestone. Once you reach your Full Retirement Age, the earnings limit completely disappears. You can earn any amount of income from work, and your Social Security benefits will not be reduced. This is why financial planning often emphasizes understanding your FRA and coordinating it with your work plans.

Exemptions Once You Reach Full Retirement Age

The primary exemption from the earnings test is simply reaching your Full Retirement Age. At this point, the entire concept of an “earnings limit” becomes irrelevant for Social Security purposes. This allows individuals to continue working full-time or part-time, start a new business, or engage in any income-generating activity without fear of their monthly Social Security checks being reduced. This exemption is a powerful incentive for some to delay claiming benefits until their FRA, especially if they anticipate continuing to work beyond that age. It ensures that benefits received are truly supplementary to continued earnings, rather than being subject to the initial earnings test designed for early retirees.

Strategies for Maximizing Income While Receiving Benefits

Navigating the earnings limit isn’t just about adhering to rules; it’s about crafting a personalized strategy that aligns with your financial goals and desired lifestyle in retirement. Maximizing your overall income involves a careful consideration of when to claim benefits, how to structure your work, and the types of income you generate.

Timing is Everything: Deciding When to Claim

The decision of when to start collecting Social Security benefits is one of the most critical financial choices you’ll make in retirement. It’s intimately tied to how much you can make while working.

- Claiming Early (Before FRA): If you claim benefits as early as age 62, your monthly payments will be permanently reduced. Additionally, you will be subject to the earnings limit. This means if you continue to work and earn above the threshold, not only are your benefits lower due to early claiming, but they can also be temporarily withheld. This path might be suitable for those who truly need the income immediately and don’t plan to work significantly.

- Claiming at Full Retirement Age (FRA): By waiting until your FRA, you receive 100% of your primary insurance amount (PIA). More importantly, the earnings limit disappears. This offers the freedom to work as much as you want without any benefit reductions. It’s often a good strategy for those who plan to work part-time or full-time through their early to mid-60s.

- Claiming Late (After FRA, up to age 70): For every year you delay claiming benefits past your FRA, up to age 70, you earn delayed retirement credits. These credits permanently increase your monthly benefit by a significant percentage (e.g., 8% per year for those born in 1943 or later). If you can afford to delay and continue working, this is a powerful way to maximize your monthly Social Security payment for life, particularly if you have a long life expectancy. The earnings limit is irrelevant here, as it doesn’t apply after FRA.

The Power of Deferred Retirement Credits

Delayed retirement credits are a key incentive for those who can afford to wait to claim benefits. By continuing to work and deferring your Social Security application beyond your FRA, your future monthly benefits increase significantly. These credits are added for each month you delay, up to age 70. This strategy is particularly effective for individuals who are still working and earning a substantial income, as it allows them to not only avoid the earnings test but also grow their future Social Security payout. The long-term impact of these credits can be substantial, providing a higher, inflation-adjusted income stream for the rest of your life.

Understanding What Counts as “Earnings”

A critical distinction for Social Security purposes is between “earned income” and “unearned income.” Only earned income counts towards the Social Security earnings limit.

- Earned Income: This includes wages received from an employer and net earnings from self-employment. For self-employed individuals, it’s your net profit after business expenses are deducted. This is the income stream that Social Security is concerned about when determining benefit reductions for those under FRA.

- Unearned Income: This category includes a wide array of income sources that do not affect your Social Security benefits, regardless of your age or how much you earn. Examples include:

- Investment income: Dividends, interest, capital gains from selling stocks, bonds, or mutual funds.

- Pensions and annuities: Payments from traditional pension plans or purchased annuities.

- Rental income: Income from real estate properties where you are not actively involved in the day-to-day management as a business.

- IRA/401(k) withdrawals: Distributions from retirement accounts.

- Gambling winnings, inheritances, gifts.

This distinction is vital for strategic planning. Many retirees choose to supplement their income with unearned sources, knowing these will not trigger any reduction in their Social Security benefits.

Navigating the Earnings Limit: Practical Approaches

For those who are under their Full Retirement Age and wish to continue working, several practical approaches can help navigate the earnings limit and optimize their financial situation.

The “Sweet Spot” for Part-Time Work

If you are collecting benefits before your FRA and want to work, finding the “sweet spot” means earning just enough to meet your needs without exceeding the annual earnings limit. This often involves part-time work or seasonal employment. By monitoring your income throughout the year and adjusting your work hours, you can minimize or even avoid benefit reductions. For example, if the limit is $22,320 in a given year (hypothetical), aiming for annual earnings just under that amount could allow you to keep all your benefits while still earning supplementary income. Some beneficiaries may even consider adjusting their work schedule to earn more in the months after reaching their FRA within that calendar year, as only earnings before FRA count.

Rethinking Work: Shifting to Passive Income Streams

Given that unearned income does not affect Social Security benefits, many retirees strategically shift their focus towards generating passive income streams. This approach allows them to supplement their retirement funds substantially without triggering the earnings test.

- Rental Properties: Owning and managing rental properties can provide a steady stream of income. If you are not actively involved in the day-to-day business operations (e.g., you hire a property manager), this income is often considered passive.

- Dividend-Paying Stocks and Funds: Investing in companies that pay regular dividends or in dividend-focused exchange-traded funds (ETFs) can provide a reliable income source.

- Interest Income: Bonds, high-yield savings accounts, and certificates of deposit (CDs) can generate interest income.

- Annuities: Purchasing an annuity can provide guaranteed income payments for a set period or for life.

- Royalties: If you have creative works (books, music, patents), royalty income is typically passive.

These strategies allow retirees to maintain financial activity and income generation without the complexities of the Social Security earnings test.

Self-Employment Considerations

Working for yourself in retirement offers flexibility but also introduces specific considerations regarding the earnings limit. For self-employed individuals, “earnings” refer to your net profit after deducting legitimate business expenses.

- Net Earnings Calculation: It’s crucial to accurately track all business income and expenses to determine your net earnings. This figure is what the SSA uses to apply the earnings test.

- Managing Income: Self-employed individuals have more control over their income flow. This can be an advantage, as you might be able to strategically manage client work or project timelines to keep your net earnings below the limit if you are under FRA.

- The “Significant Services” Test: For self-employed individuals, the SSA also considers whether you are performing “significant services” in your business. If you are significantly involved, even if your net earnings are low, it might still count as earned income. However, if you’re only performing minimal oversight (e.g., investing capital, occasionally advising), your income might be treated as passive.

- Tax Implications: Self-employment income is subject to self-employment taxes (Social Security and Medicare taxes) in addition to income tax, which needs to be factored into your financial planning.

The Long-Term Impact: How Current Earnings Affect Future Benefits

The earnings limit isn’t just about immediate benefit reductions; it can also have long-term implications for your Social Security benefits, often in a positive way. Understanding these future adjustments is key to a holistic view of your retirement finances.

Recalculation of Benefits

A common misconception is that benefits withheld due to the earnings test are simply “lost.” In reality, they are not. The Social Security Administration keeps track of the months for which your benefits were withheld. Once you reach your Full Retirement Age and the earnings limit no longer applies, the SSA performs a recalculation of your benefits. They essentially “give back” the withheld benefits by increasing your monthly payment for the rest of your life. This is done by adjusting your record to remove the months where benefits were reduced due to the earnings limit, effectively allowing those months to count as if you had not claimed benefits. This recalculation can result in a higher monthly benefit payment once you reach FRA.

The Importance of Your Earnings Record

Your Social Security benefit amount is based on your highest 35 years of indexed earnings. When you continue to work in retirement, especially if you earn more than you did in some of your earlier career years (after adjusting for inflation), those new, higher earnings can replace lower-earning years in your benefit calculation. This can lead to a slight increase in your monthly Social Security benefit over time, even if you were subject to the earnings limit earlier. It underscores the importance of regularly checking your Social Security earnings statement to ensure accuracy and to see how continued work impacts your long-term benefit.

Tax Implications of Working in Retirement

Working in retirement can also affect the taxation of your Social Security benefits. If your “provisional income” (which includes your adjusted gross income, tax-exempt interest, and half of your Social Security benefits) exceeds certain thresholds, a portion of your Social Security benefits may become taxable.

- Federal Income Tax: Up to 50% or even 85% of your Social Security benefits can be subject to federal income tax, depending on your provisional income. If you continue to work and your earned income pushes your total income above these thresholds, you may find yourself paying taxes on your Social Security benefits, even if you didn’t before.

- State Income Tax: A number of states also tax Social Security benefits, though many do not. It’s essential to understand your state’s specific rules.

This added layer of complexity means that while working can boost your overall income, it’s crucial to factor in the potential tax implications to fully understand your net financial gain. Tax planning becomes an even more vital component of your retirement strategy.

Resources and Professional Guidance

Navigating the intricacies of Social Security and retirement income planning can be daunting. Fortunately, numerous resources and professional avenues are available to help you make the best decisions for your unique situation.

Utilizing the Social Security Administration (SSA) Website

The official Social Security Administration website (SSA.gov) is an invaluable resource. It offers comprehensive information on all aspects of Social Security, including the earnings test, benefit calculators, and detailed guides.

- “My Social Security” Account: Creating a “My Social Security” account allows you to view your earnings record, get personalized benefit estimates, and check the status of your application. This is essential for tracking your contributions and understanding your projected benefits.

- Benefit Calculators: The SSA website provides various calculators that can help you estimate your benefits based on different claiming ages and earnings scenarios.

- Publications and Fact Sheets: The SSA publishes numerous documents explaining specific rules and regulations in clear, accessible language, including those related to working while collecting benefits.

Regularly consulting these resources can empower you with the knowledge needed to make informed choices.

When to Consult a Financial Advisor

While the SSA website provides a wealth of information, a financial advisor, particularly one specializing in retirement planning, can offer personalized guidance tailored to your specific circumstances.

- Complex Financial Situations: If you have diverse income sources, significant assets, or a complicated family situation (e.g., spousal or survivor benefits), a financial advisor can help integrate your Social Security strategy into your broader financial plan.

- Optimizing Claiming Strategies: An advisor can help you analyze the best time to claim benefits, considering your health, life expectancy, other income sources, and spouse’s benefits.

- Tax Planning: They can assist with tax-efficient withdrawal strategies from retirement accounts and help you understand the tax implications of working in retirement on both your earned income and Social Security benefits.

- Investment Guidance: An advisor can help you set up and manage passive income streams that complement your Social Security benefits without triggering the earnings test.

- Holistic Retirement Planning: Beyond Social Security, they can help you with budgeting, estate planning, and long-term care considerations, providing a comprehensive roadmap for your retirement years.

In conclusion, understanding how much you can make while collecting Social Security is a cornerstone of intelligent retirement planning. It requires a clear grasp of the earnings limit, strategic timing of your benefit claims, and an awareness of the distinction between earned and unearned income. By proactively managing your work and income streams, and utilizing available resources and professional advice, you can ensure that your retirement years are both financially secure and personally fulfilling.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.