Navigating the intersection of work and Social Security benefits can be one of the most complex financial planning challenges for pre-retirees and retirees alike. Many individuals wish to supplement their Social Security income with continued employment, either out of necessity or a desire to remain active and engaged. The crucial question, however, is often: “How much can I earn while receiving Social Security without impacting my benefits?” The answer isn’t always straightforward, as it depends on your age, the type of income you earn, and the specific rules governing Social Security’s earnings test. This guide will delve into these regulations, offering insights and strategies to help you maximize your income while understanding the implications for your Social Security benefits.

Understanding Social Security’s Earnings Test

The Social Security Administration (SSA) implements an “earnings test” that can temporarily reduce benefits for individuals who continue to work while receiving Social Security, particularly before they reach their full retirement age (FRA). This test is designed to balance the system, ensuring that benefits are primarily directed towards those who have fully exited the workforce or are past the age where significant employment is expected.

What is the Social Security Earnings Test?

The earnings test is a mechanism by which the SSA subtracts a portion of your Social Security benefits if your earnings exceed specific annual limits. It’s important to understand that this is not a permanent reduction of your lifetime benefits. Any benefits withheld due to the earnings test are usually credited back to you in the form of higher monthly benefits once you reach your full retirement age. The primary purpose is to ensure that benefits align with the intent of Social Security—providing income replacement for retirement, disability, or survivorship.

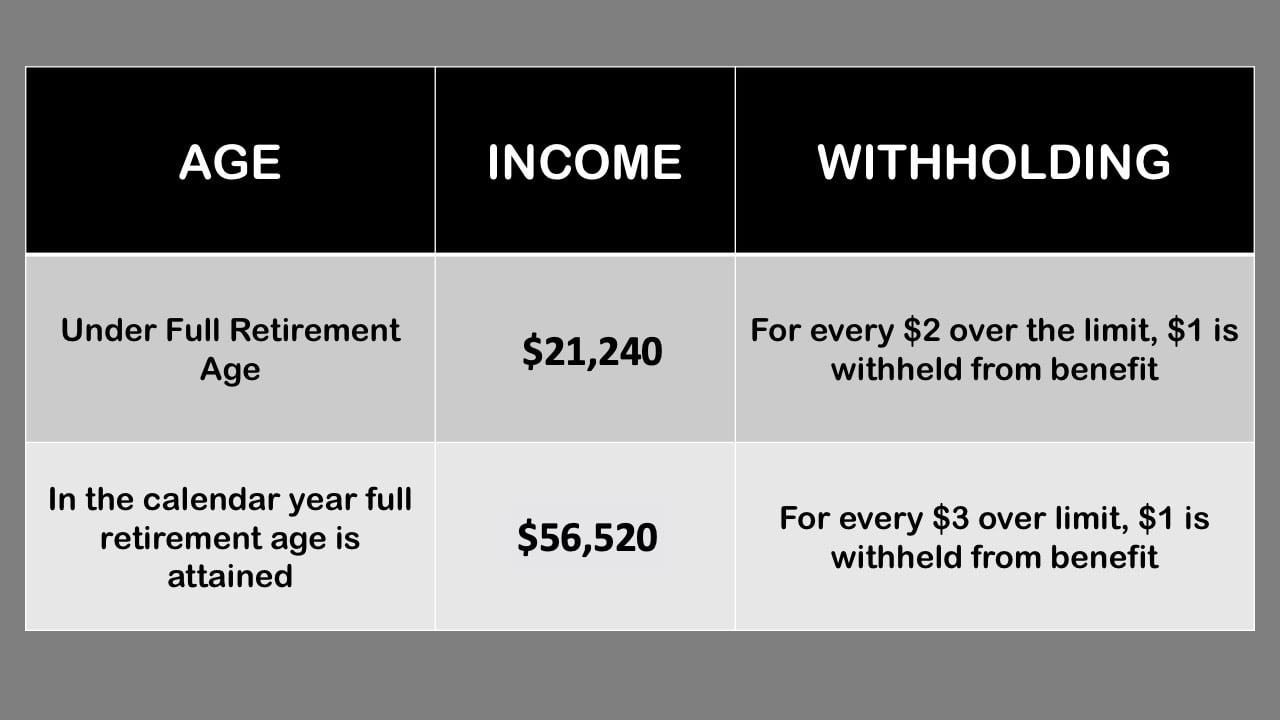

The Annual Earnings Limit Thresholds

The SSA sets different annual earnings limits based on your age relative to your full retirement age (FRA). Full retirement age varies depending on your birth year, ranging from 66 for those born between 1943 and 1954, gradually increasing to 67 for those born in 1960 or later.

- Before Full Retirement Age (FRA): If you are younger than your FRA for the entire year, a lower earnings limit applies. For every dollar you earn above this limit, your Social Security benefits will be reduced by $1 for every $2.

- In the Year You Reach Full Retirement Age: A higher earnings limit applies specifically to the months before you reach your FRA in that calendar year. The reduction rate is also different: $1 for every $3 earned above this higher limit.

- At or After Full Retirement Age: Once you reach your full retirement age, the earnings test no longer applies. You can earn any amount without having your Social Security benefits reduced.

It’s crucial to check the most current earnings limits directly with the Social Security Administration or on their official website, as these figures are adjusted annually for inflation.

How Earnings Reductions Are Calculated

The reduction in benefits is calculated based on your “countable earnings.” For employees, this is your gross wages, not including things like pensions, annuities, investment income, or interest. For self-employed individuals, it’s your net earnings from self-employment. The SSA tracks your earnings and will either reduce your monthly benefit payments directly or require you to repay any overpayments if you exceed the limits. This process, while seemingly penalizing, is merely a withholding mechanism. The withheld benefits are not lost; they are factored into a recalculation of your benefits at your FRA, resulting in a slightly higher monthly payment for the rest of your life. This adjustment is called the “Adjustment of the Reduction Factor” (ARF).

Navigating Earnings Limits Before Full Retirement Age (FRA)

For many individuals, the desire or need to work extends into the early years of Social Security receipt, long before their full retirement age. Understanding the specific earnings limits that apply during this period is critical for effective financial planning. Ignoring these limits can lead to unexpected reductions in benefits, creating financial strain.

The “Under FRA” Earnings Limit Explained

If you begin receiving Social Security retirement or survivor benefits and you are younger than your full retirement age (FRA) for the entire year, you are subject to the strictest earnings limit. The specific dollar amount of this limit changes annually, so checking the current figure is paramount. However, the rule generally states that for every dollar you earn above this annual threshold, your Social Security benefits will be reduced by $1 for every $2. For example, if the limit is $20,000 and you earn $22,000, your earnings exceed the limit by $2,000. Your benefits would then be reduced by $1,000 ($2,000 / 2). This reduction applies to your total annual benefits, potentially impacting several months’ worth of payments until the overpayment is recovered.

Strategies for Working While Under FRA

Given the $1 for $2 reduction, strategic planning is essential.

- Monitor Your Income Closely: Keep meticulous records of your gross earnings throughout the year. If you find yourself approaching the limit, you might consider adjusting your work hours, taking unpaid leave, or deferring bonuses until the next calendar year.

- Understand Your Net Impact: Factor in the potential benefit reduction when calculating your overall income. For instance, if you earn an extra $2,000 that pushes you over the limit by $1,000, you will lose $500 in Social Security benefits. Your net gain from that extra work is $1,500, not the full $2,000.

- Consider Tax Implications: Remember that your earnings are still subject to income tax and payroll taxes (Social Security and Medicare). Also, the portion of your Social Security benefits that becomes taxable can increase if your combined income (adjusted gross income + non-taxable interest + one-half of your Social Security benefits) exceeds certain thresholds.

Types of Income That Count Towards the Limit

Only “earned income” counts toward the Social Security earnings limit. This includes:

- Wages: Money you earn from an employer, before deductions for taxes or other expenses.

- Net Earnings from Self-Employment: This is your gross income from self-employment minus your allowable business deductions. The SSA uses this figure to determine your countable earnings if you own your own business. It’s crucial for self-employed individuals to accurately track their income and expenses.

Income That Doesn’t Count

Many common forms of income do not count towards the earnings limit, which is important for financial diversification:

- Pensions and Annuities: Payments from retirement plans, 401(k)s, IRAs, or other deferred compensation schemes.

- Investment Income: Interest from savings accounts, dividends from stocks, capital gains from selling assets, or rental income from properties (unless you are a real estate professional actively managing properties as your primary business).

- Government or Military Retirement Pay: These benefits are generally not subject to the earnings test.

- Veteran’s Benefits: Payments from the Department of Veterans Affairs.

- Disability Benefits: Payments received from private disability insurance policies.

- Gifts or Inheritances: These are not considered earned income.

Understanding this distinction allows individuals to generate income from various sources without affecting their Social Security benefits.

The “Year of Full Retirement Age” Special Rules

The year you reach your full retirement age (FRA) is a transitional period with its own unique set of rules regarding the Social Security earnings test. This year offers a more lenient approach compared to the years before FRA, providing greater flexibility for those who wish to work.

The Higher Earnings Limit in Your FRA Year

In the calendar year that you attain your full retirement age, a significantly higher annual earnings limit applies to your income earned before the month you reach your FRA. This is a crucial distinction: the higher limit only pertains to earnings in the months leading up to your FRA birthday, not for the entire year if you reach FRA early in the year. The reduction rate for exceeding this higher limit is also more favorable: for every $1 you earn above the limit, your benefits will be reduced by $1 for every $3. This means you can earn more before your benefits are impacted, and the impact is less severe per dollar earned over the limit. Again, it is essential to consult the SSA for the current year’s specific dollar amount for this higher limit.

Monthly vs. Annual Calculation

One of the most important “special rules” for the year you reach FRA is the option for a monthly earnings test. During your initial year of receiving benefits, the SSA applies a monthly earnings limit if it results in fewer withheld benefits than the annual limit. This means if you significantly reduce or stop working in the months leading up to your FRA, or during the months you start receiving benefits, you might avoid or reduce the benefit withholding, even if your total annual earnings would have exceeded the limit under the standard annual test. For example, if you worked heavily in the first few months of the year but then stopped working the month you turned FRA and started your benefits, the monthly rule might apply, allowing you to receive full benefits for the months you didn’t work, even if your early-year earnings were high. After this initial year, only the annual earnings test applies.

Planning for Your FRA Year

Careful planning can help you maximize your income and benefits during this pivotal year.

- Time Your Benefit Application: If you plan to work, consider when to start your benefits relative to when you reach your FRA. You might choose to wait until your FRA month to start benefits to avoid any earnings test reductions altogether from that point forward.

- Adjust Work Schedule: If your earnings are likely to exceed the higher limit, and especially if you’re taking advantage of the monthly calculation rule, consider adjusting your work hours or taking a hiatus in the months preceding or during your FRA month.

- Consult with the SSA: It is highly recommended to contact the Social Security Administration directly or use their online tools to get personalized estimates and understand how your specific earnings situation will be handled during your FRA year. They can help you determine the most advantageous time to start your benefits and how your earnings might affect them.

Working at or After Full Retirement Age: No Limits, But Considerations Remain

Reaching your Full Retirement Age (FRA) is a significant milestone for Social Security recipients. At this point, the rules surrounding earned income change dramatically, offering much greater freedom and financial flexibility. However, while the earnings test disappears, other financial considerations persist.

The Freedom of No Earnings Limit

Once you reach your full retirement age, the Social Security earnings test no longer applies. This means you can earn any amount of income from employment or self-employment without having your Social Security benefits reduced. This offers a substantial advantage, allowing individuals to work as much as they desire, pursue new careers, or simply enjoy their passion projects without worrying about their government benefits being impacted. This freedom removes a significant barrier for many, enabling them to supplement their retirement income freely and enhance their financial security. The SSA’s philosophy shifts from supporting early retirement to providing a safety net regardless of continued work activity once an individual reaches the age where full benefits are expected.

The Impact of Continued Work on Future Benefits

While the earnings test vanishes, continued work after FRA can still positively influence your future Social Security benefits.

- Increased Average Indexed Monthly Earnings (AIME): Social Security benefits are calculated based on your highest 35 years of inflation-adjusted earnings. If you continue to work and earn more in a year after FRA than in one of your lower-earning years within your top 35, that new higher-earning year will replace an old lower-earning year in the calculation. This can lead to a slightly higher monthly benefit amount. The SSA automatically recomputes your benefit each year if your earnings warrant it.

- Delayed Retirement Credits: Even though you are receiving benefits, you can still accrue delayed retirement credits if you were born after 1942 and chose to delay receiving your benefits until after your FRA (up to age 70). However, once you start receiving benefits, you generally stop accruing these credits. The primary benefit of working after FRA while receiving benefits is the potential for a higher AIME.

Tax Implications of Working After FRA

While your benefits are no longer reduced, the income you earn after FRA still has tax implications, and these can indirectly affect your Social Security benefits’ net value.

- Income Tax: All earned income, whether from wages or self-employment, is subject to federal (and often state) income taxes, regardless of your age.

- Payroll Taxes: You will continue to pay Social Security and Medicare taxes (FICA) on your earned income, even if you are receiving Social Security benefits.

- Taxability of Social Security Benefits: The most significant indirect impact is how your earned income can affect the taxability of your Social Security benefits themselves. If your “combined income” (your adjusted gross income + non-taxable interest + one-half of your Social Security benefits) exceeds certain thresholds, a portion of your Social Security benefits (up to 85%) will become subject to federal income tax. Earning more income from work after FRA means a higher combined income, which can push you past these thresholds, leading to a larger portion of your Social Security benefits being taxed. This isn’t a reduction by the SSA, but rather a tax liability on the benefits you receive.

Understanding these considerations is key to truly maximizing your financial position when working at or after your full retirement age.

Practical Tips and Financial Planning for Social Security Recipients

Navigating Social Security’s earnings limits and making informed decisions about working in retirement requires proactive planning and a clear understanding of the rules. Here are some practical tips to help you manage your finances effectively while receiving benefits.

Regularly Monitor Your Earnings

The most fundamental piece of advice is to meticulously track your gross earnings throughout the year, especially if you are working before your full retirement age.

- Employees: Keep track of your pay stubs and year-to-date earnings.

- Self-Employed Individuals: Maintain accurate records of your income and expenses to correctly calculate your net earnings from self-employment.

- Use the SSA’s Tools: The Social Security Administration provides online tools and your “My Social Security” account, where you can report estimated earnings and monitor your benefits. Reporting changes in estimated earnings promptly can help the SSA adjust your benefits in advance, preventing large overpayments that you might need to repay.

Proactive monitoring allows you to anticipate potential benefit reductions and make adjustments to your work schedule if necessary to stay below the limits or manage the impact.

Consult with a Financial Advisor

The interplay between Social Security benefits, earned income, taxes, and overall retirement planning can be incredibly complex. A qualified financial advisor who specializes in retirement planning can provide invaluable personalized guidance.

- Benefit Maximization: They can help you understand the optimal time to claim Social Security benefits based on your specific financial situation and health.

- Earnings Test Strategies: An advisor can help you develop strategies to work within or around the earnings limits, considering your income needs and long-term financial goals.

- Tax Efficiency: They can advise on how your earned income and Social Security benefits will be taxed at both federal and state levels, helping you implement strategies to minimize your overall tax burden.

- Holistic Planning: A financial advisor can integrate your Social Security income, work earnings, investments, and other assets into a comprehensive retirement plan, ensuring all pieces work together efficiently.

Understand the Long-Term Impact of Earning Reductions

While having benefits withheld due to the earnings test can be frustrating, remember that these are not permanently lost. The SSA applies an “Adjustment of the Reduction Factor” (ARF) once you reach your full retirement age. At that point, your past benefit reductions are recalculated, and your future monthly benefit amount is permanently increased to account for the months you didn’t receive benefits. This adjustment helps to mitigate the long-term impact of the earnings test, essentially ensuring you get your benefits later rather than losing them entirely. Understanding this concept can alleviate some of the immediate stress associated with benefit reductions.

Utilizing Different Income Streams

As discussed, only earned income (wages and net self-employment earnings) counts towards the Social Security earnings limit. This distinction offers a powerful opportunity for financial planning:

- Diversify Income Sources: Actively seek out income streams that are not considered “earned income.” This could include drawing down from IRAs or 401(k)s, generating income from investments (dividends, interest, capital gains), or receiving rental income from properties (if not actively managed as a business).

- Strategic Withdrawals: If you need more income but are approaching the earnings limit, consider making withdrawals from tax-deferred retirement accounts. These withdrawals will count as income for tax purposes and can affect the taxability of your Social Security benefits, but they will not reduce your Social Security benefits under the earnings test.

By carefully distinguishing between earned income and other forms of income, you can strategically manage your finances to receive the maximum allowable Social Security benefits while still supplementing your income from various sources. Successful retirement planning often involves a multi-faceted approach, balancing work, benefits, and investments to achieve financial security and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.