For anyone navigating the landscape of personal and business finance, understanding the tools at their disposal is paramount. Among the most ubiquitous financial instruments is the credit or charge card, and American Express (Amex) holds a unique position within this ecosystem. A seemingly simple question—”how many numbers are on an Amex card?”—unravels a deeper discussion about financial security, transaction processing, and the very architecture of modern financial tools. While the most prominent set of digits, the Primary Account Number (PAN), is indeed the face of your card, it is far from the only sequence of numbers crucial to its function and your financial well-being.

Unlike Visa or Mastercard, which typically feature 16 digits, American Express cards are renowned for their distinctive 15-digit PAN. This difference is more than just a stylistic choice; it reflects a unique operational structure that has evolved over decades. However, an Amex card is a repository of several other vital numerical identifiers, each serving a specific purpose, from validating transactions to safeguarding your financial information. This article will delve into the various numbers found on an Amex card, explore their financial significance, and provide crucial insights into protecting them to maintain robust financial security. For individuals and businesses alike, a comprehensive understanding of these digits is not merely academic; it is a fundamental aspect of intelligent financial management in today’s digital age.

The Anatomy of Your American Express Card Number: A Financial Primer

At the heart of every American Express card lies its unique identifier—a sequence of digits that enables it to function as a globally recognized financial instrument. Understanding this primary number is the first step in appreciating the sophisticated financial architecture it represents.

The Distinctive 15-Digit PAN

The most recognizable feature of an American Express card, distinguishing it immediately from most other major payment networks, is its 15-digit Primary Account Number (PAN). This number, embossed or printed on the front of the card, is not a random sequence. It is a carefully structured code that communicates vital information about the card, the issuer, and the cardholder’s account. This deliberate deviation from the more common 16-digit format used by Visa, Mastercard, and Discover is a hallmark of American Express’s proprietary system, reflecting its history as a travel and entertainment charge card provider before it fully embraced the credit card model. For a cardholder, knowing this primary identifier is crucial for making purchases, setting up recurring payments, and managing their account online.

Decoding the Digits: What Each Section Means

Every digit within the 15-digit PAN serves a specific, structured purpose, making it more than just an account number. This segmentation is a standard practice across the financial industry, albeit with network-specific variations.

- The Major Industry Identifier (MII): The very first digit of an Amex card is always a ‘3’. This is the MII, which indicates the industry category of the card issuer. For American Express, ‘3’ signifies “Travel and Entertainment”—a nod to its historical roots. This initial digit immediately tells a payment system that it’s dealing with an Amex card, initiating the appropriate processing protocols.

- The Issuer Identification Number (IIN): The subsequent three digits, combined with the MII, form the Issuer Identification Number (IIN), sometimes referred to as the Bank Identification Number (BIN). For Amex, this usually falls within the range of 34 or 37, followed by another digit (e.g., 34xx or 37xx). This IIN specifically identifies American Express as the card issuer. It’s crucial for routing transactions to the correct financial institution for authorization and settlement.

- The Account Number: Following the IIN, the next ten digits (from the 5th to the 14th digit) constitute the unique customer account number. This sequence specifically identifies the individual cardholder’s account within American Express’s vast system. This is the portion that truly personalizes the card, linking it directly to your financial relationship with Amex, including your credit history, spending limits, and reward balances.

- The Check Digit (Luhn Algorithm): The final, 15th digit is a crucial component for financial security and data integrity. This is the check digit, generated using the Luhn algorithm (also known as the “modulus 10” algorithm). This algorithm is a simple checksum formula used to validate a variety of identification numbers. Its purpose is to detect common errors, such as mistyping a digit or transposing two digits, when the card number is entered manually. While it doesn’t offer cryptographic security, it’s an effective first line of defense against accidental errors and even some forms of unsophisticated fraud attempts at the point of entry, ensuring that only valid card numbers can proceed through the payment network.

Why 15 Digits? Amex’s Unique Approach

The 15-digit format for American Express cards is a legacy decision rooted in the early days of electronic payment systems. While other networks expanded to 16 digits to accommodate a growing number of banks and account variations, Amex, which primarily issues its own cards directly, found its original 15-digit structure sufficient. From a financial perspective, this unique numbering system doesn’t inherently make Amex cards more or less secure or functional than 16-digit cards; it simply reflects a different architectural choice within the broader card payment industry. For cardholders, it primarily means recognizing this difference when entering card details online or over the phone, as systems often expect a 16-digit input by default.

Beyond the Primary Account Number: Essential Security and Identification Figures

While the 15-digit PAN is the most prominent identifier, several other numerical sequences on your Amex card play equally critical roles in facilitating transactions and, more importantly, in safeguarding your financial assets. Ignoring these numbers or failing to understand their purpose can expose you to significant financial risks.

The Card Expiration Date: More Than Just a Deadline

Every Amex card features an expiration date, typically displayed as a two-digit month and a two-digit year (e.g., 12/26 for December 2026). This isn’t merely a date for physical card replacement; it’s a vital security feature and a mechanism for financial management. From a security standpoint, the expiration date ensures that older, potentially compromised card numbers are retired from active use, prompting regular updates of card information for recurring payments. Financially, it prompts cardholders to update their information with merchants, preventing service interruptions and ensuring seamless payment processing. Furthermore, merchants are generally prohibited from processing transactions if the card has expired, adding another layer of fraud prevention. Managing your finances effectively means tracking these dates, especially for subscriptions and online services tied to your card.

The Card Identification Value (CID) and Card Security Code (CSC): Your Online and Phone Shield

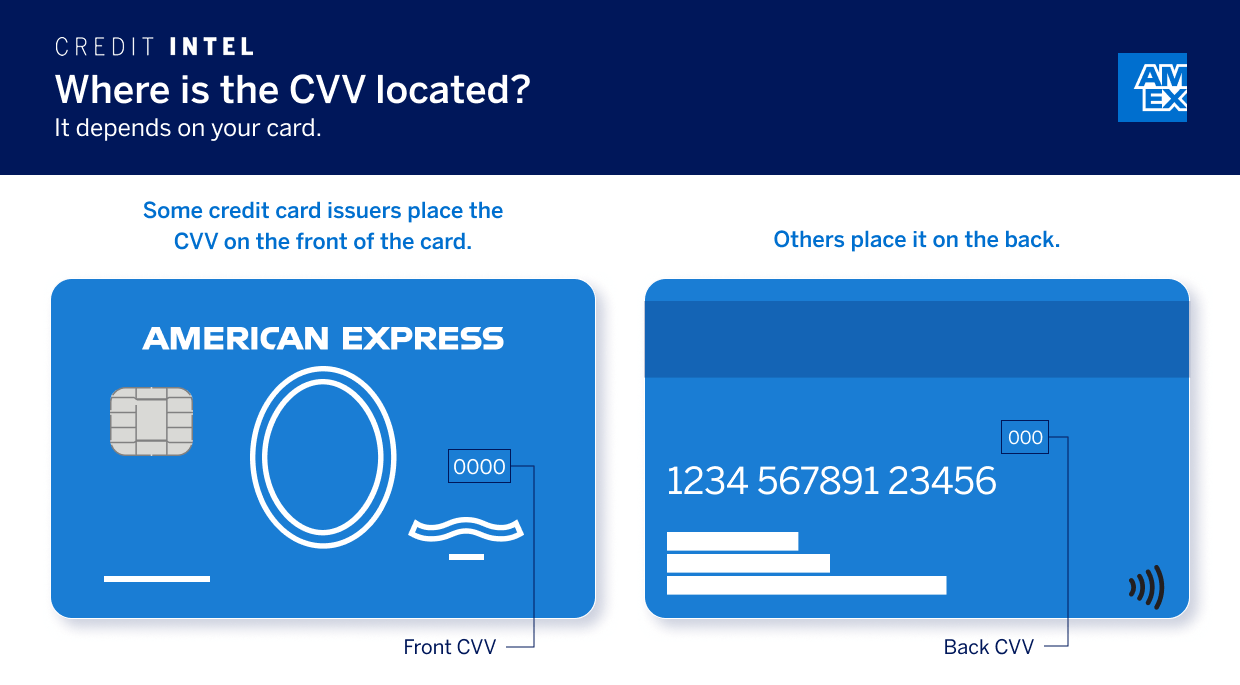

American Express utilizes a unique 4-digit security code, often referred to as the Card Identification Value (CID) or Card Security Code (CSC). Crucially, this code is not found on the magnetic stripe and is typically printed on the front of the card, above the primary account number (unlike Visa/Mastercard’s CVV2, which is usually a 3-digit code on the back). The CID is a crucial layer of defense against card-not-present fraud (CNP fraud), which occurs when the physical card isn’t presented for a transaction, such as online purchases or telephone orders.

When you make a purchase online or over the phone, you’ll often be prompted to enter this CID. The primary financial purpose of the CID is to verify that the person making the purchase actually possesses the physical card. Since the CID is not stored in the magnetic stripe or EMV chip data, even if a fraudster skims your card’s data, they won’t automatically have the CID. This significantly reduces the risk of unauthorized transactions and protects your financial accounts from compromise in situations where your card number alone might be stolen.

Understanding Your Statement and Customer Service Numbers

Beyond the card itself, your Amex financial statements and online account portals will display various other numbers crucial for managing your money. Your account statement typically includes an abbreviated version of your card number (e.g., last four digits) for identification, along with a unique customer ID or statement number. These numbers are vital when communicating with Amex customer service, particularly when discussing specific transactions or discrepancies. For financial tracking, understanding how your full PAN relates to the partial numbers on your statement helps reconcile expenses, monitor spending, and identify any unauthorized activity, forming a cornerstone of responsible personal and business financial management.

Protecting Your Amex Card Numbers: A Cornerstone of Financial Security

The presence of multiple numerical identifiers on your Amex card underscores the critical importance of robust financial security. Every digit, from the PAN to the CID, is a key to your financial account, and their compromise can lead to significant financial distress.

The Risks of Number Compromise: Fraud and Identity Theft

The most immediate and severe risk of your Amex card numbers being compromised is financial fraud. If a criminal obtains your PAN, expiration date, and CID, they can make unauthorized purchases online or over the phone. This can lead to substantial financial losses, even if your liability is limited by Amex’s fraud protection policies, as it still requires time and effort to resolve. Beyond direct monetary loss, the theft of your card numbers can be a gateway to broader identity theft. Criminals may use these details to attempt to open new accounts in your name, damage your credit score, or gain access to other personal information, leading to long-term financial and personal complications. Proactive vigilance is therefore not just a recommendation but a necessity for financial health.

Best Practices for Safeguarding Your Card Details

Protecting your Amex card numbers requires a multi-faceted approach, integrating caution with smart financial habits.

- Online Shopping Safety: Always ensure you are shopping on secure websites (look for “https://” in the URL and a padlock icon). Avoid storing your card details on websites unless absolutely necessary and only with trusted merchants. Be wary of phishing emails or suspicious links asking for your card information. Using strong, unique passwords for online accounts where card information is stored adds another layer of security.

- Physical Card Protection: Never let your card out of sight during transactions. Be cautious at ATMs and gas pumps, checking for skimmers. Memorize your CID if possible, and avoid writing it down. If you regularly use your card at a physical location, ensure the POS terminal is secure and the transaction process appears legitimate.

- Regular Statement Review: One of the most effective financial security measures is diligently reviewing your Amex statements (or online activity) as soon as they become available. Scrutinize every transaction for accuracy and identify any unauthorized charges immediately. Promptly report any suspicious activity to American Express. This financial discipline allows for quick detection and mitigation of potential fraud.

What to Do If Your Numbers Are Compromised

Despite best efforts, card numbers can sometimes be compromised. If you suspect your Amex card numbers have been stolen or used fraudulently:

- Contact American Express Immediately: Report the suspected fraud or theft without delay. Amex has dedicated fraud departments equipped to cancel your old card, issue a new one, and dispute unauthorized charges. Their customer service lines are usually available 24/7 for such emergencies.

- Monitor Your Account Closely: Even after reporting, continue to monitor your account for any further suspicious activity.

- Check Your Credit Report: Consider obtaining a free credit report from the major bureaus to ensure no new accounts have been opened in your name.

- Change Passwords: If your card details were stolen online, change passwords for any associated accounts.

Taking swift action can significantly limit your financial liability and prevent further damage.

The Financial Implications of Amex Card Usage and Numbering

The structured nature of Amex card numbers and their associated security features have profound implications for how financial transactions are processed and managed, impacting both individual consumers and businesses.

Understanding Transaction Processing Through Card Numbers

Every time you swipe, tap, or enter your Amex card numbers, a complex series of financial communications is initiated. The MII and IIN identify American Express as the network, routing the transaction request to their proprietary system. The account number identifies your specific account, enabling Amex to check your credit limit or available balance. The expiration date and CID (for card-not-present transactions) add layers of verification. All these numbers facilitate the authorization process, ensuring that funds are available and the transaction is legitimate before it’s approved and subsequently settled. For individuals, this means swift and secure payment. For businesses, it means reliable processing of customer payments, critical for revenue generation and cash flow management.

The Role of Card Numbers in Personal and Business Financial Tracking

For personal finance, tracking transactions linked to your unique Amex account number is fundamental to budgeting and expense management. Online banking portals and budgeting apps use these numbers (or partial numbers) to categorize spending, create financial reports, and help you stay within your financial goals. For businesses, especially those using Amex corporate cards, the specific numbering can be crucial for expense reconciliation, departmental budgeting, and tax purposes. Many accounting software solutions integrate with Amex to automatically import transactions, streamlining financial record-keeping and reducing manual data entry errors.

Amex’s Numbering in the Broader Financial Ecosystem

While Amex’s 15-digit system is unique, it operates within a larger financial ecosystem. Payment gateways, point-of-sale (POS) systems, and online merchant platforms are designed to recognize and process both 15-digit and 16-digit card numbers. This interoperability ensures that despite the numbering difference, Amex cards are widely accepted. Understanding this broader context means appreciating the seamless integration of your Amex card into a global network of financial transactions, enabling convenience and access to funds virtually anywhere. This also underscores the importance of standards and protocols in facilitating global commerce.

Maximizing Your Amex Card Benefits While Ensuring Financial Prudence

Beyond transaction functionality and security, understanding the nuances of your Amex card, including its unique numbering, contributes to more astute financial management and the maximization of benefits.

Leveraging Card Numbers for Rewards and Loyalty Programs

American Express cards are renowned for their robust rewards and loyalty programs, ranging from Membership Rewards points to airline miles and cashback. Your unique 15-digit account number is the identifier that links your spending to these benefits. Every eligible purchase processed using your card number contributes to your points balance or cashback accumulation. Smart financial planning involves strategically using your Amex card for categories that earn bonus rewards, tracking your points through your online account (identified by your card number), and redeeming them effectively to enhance your financial value. This active management turns everyday spending into tangible financial returns, whether for travel savings, statement credits, or product redemptions.

Budgeting and Debt Management with Your Amex Card

While Amex cards offer significant spending power, responsible financial management means integrating them into a disciplined budget. Your card number tracks your spending, which is then reflected in your monthly statement. Reviewing these statements meticulously allows you to monitor your expenditures against your budget, identify areas of overspending, and ensure you’re making timely payments. For charge cards, the full balance is due monthly, necessitating careful cash flow management. For credit cards, understanding your credit limit (associated with your account number) and making more than the minimum payment is crucial for avoiding interest charges and managing debt effectively. Using your Amex card prudently can also build a strong credit history, a vital component of long-term financial health.

The Importance of Financial Literacy in Card Management

Ultimately, the question “how many numbers on an Amex card?” opens the door to a broader discussion about financial literacy. Knowing the structure of your card numbers, their purpose, and the security implications empowers you to use your financial tools more safely and effectively. It’s about more than just making purchases; it’s about understanding the underlying mechanisms of credit, managing debt responsibly, protecting against fraud, and leveraging the benefits your card offers. In an increasingly complex financial world, a deep understanding of instruments like the Amex card is not just an advantage—it’s a necessity for securing and growing your financial well-being. By staying informed and adopting best practices, cardholders can maximize the utility of their American Express card while minimizing potential financial risks.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.