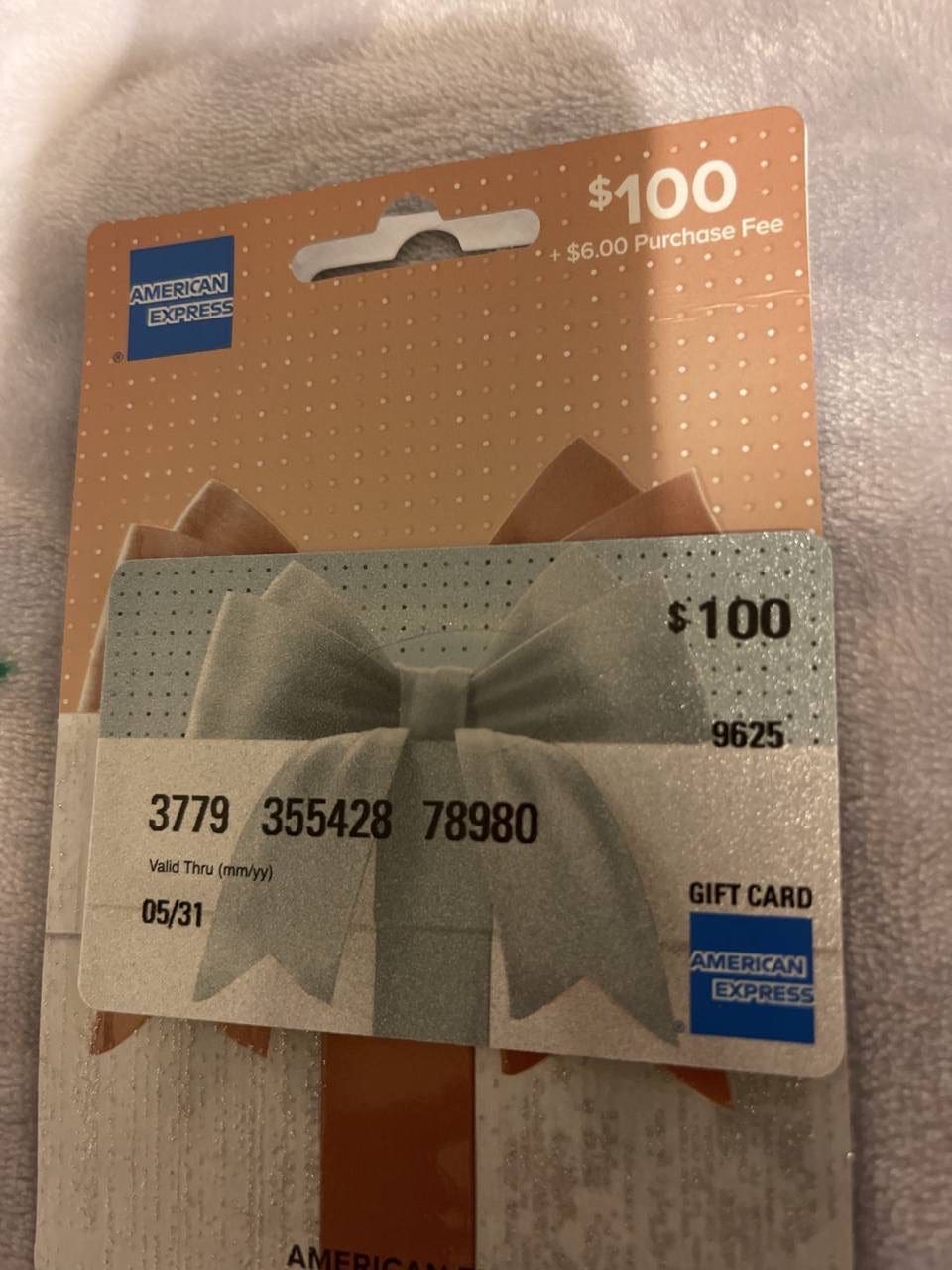

When you pull a credit card out of your wallet, you are holding a sophisticated piece of financial technology. While most global payment networks like Visa, Mastercard, and Discover have standardized a 16-digit format, American Express (Amex) has famously carved out its own path. If you have ever tried to enter your card details into an online checkout and found yourself one digit short of the usual boxes, you have likely asked: how many numbers are on an American Express card?

The answer is 15. However, the significance of those 15 digits goes far beyond a simple count. For cardholders and finance enthusiasts, understanding the architecture of an American Express card provides insight into the company’s unique position in the global financial ecosystem, its security protocols, and how it differentiates itself from other major issuers.

Understanding the 15-Digit Format: Why American Express Is Different

The most immediate difference between an American Express card and its competitors is the length of the Primary Account Number (PAN). While the 16-digit format is the industry standard for most, Amex utilizes a 15-digit sequence. This distinction is not arbitrary; it is rooted in the history of the company and the specific standards set by the International Organization for Standardization (ISO).

The ISO/IEC 7812 Standard

Credit card numbering is governed by the ISO/IEC 7812 standard, which ensures that payment systems across the world can communicate seamlessly. Under this standard, cards are allowed to have anywhere from 8 to 19 digits. American Express chose the 15-digit structure decades ago, and because they operate as both the card issuer and the payment network, they have the autonomy to maintain this unique format without needing to conform to the 16-digit preference of the banking associations that govern Visa and Mastercard.

The Breakdown of the 15 Digits

An Amex card number is not a random string of digits. It is a carefully constructed code that identifies the issuer, the currency, and the specific account.

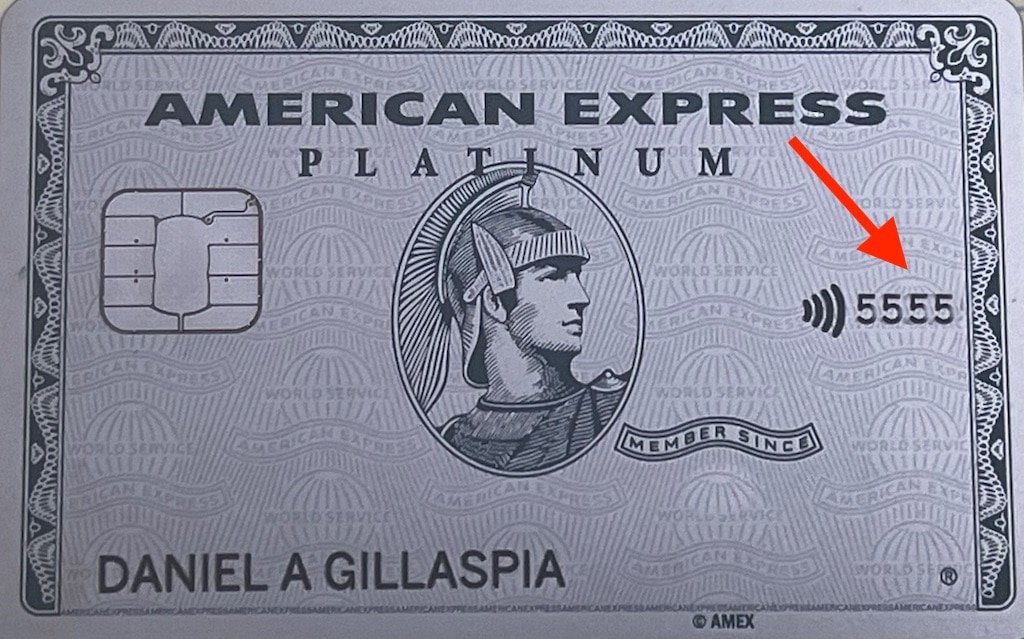

- The First Two Digits: These are known as the Major Industry Identifier (MII). For American Express, these digits almost always begin with “34” or “37.” This immediately tells any point-of-sale system that the transaction is being routed through the American Express network.

- Digits 3 and 4: These digits typically indicate the card type and the currency used for the account.

- Digits 5 through 14: This ten-digit string represents the specific account number assigned to the cardholder.

- The 15th Digit: This is the “Check Digit,” calculated using the Luhn algorithm. It serves as a mathematical verification to ensure the number is valid and hasn’t been typed incorrectly.

Security Features: The 4-Digit CID vs. the 3-Digit CVV

Beyond the 15-digit account number, American Express cards feature a secondary set of numbers that are critical for security, particularly in “Card Not Present” (CNP) transactions, such as online shopping. This is another area where Amex differs significantly from other financial tools.

Why Amex Uses a Front-Facing CID

On a Visa or Mastercard, you will find a 3-digit Card Verification Value (CVV) on the back of the card, usually on or near the signature strip. American Express, however, uses a 4-digit Card Identification Number (CID).

Crucially, the Amex CID is located on the front of the card, typically printed in small digits above the 15-digit account number. This design choice is intended to add an extra layer of security. By having a 4-digit code instead of 3, there are 10,000 possible combinations instead of 1,000, making it statistically much harder for fraudulent software to “guess” the code through brute-force attacks.

Enhancing Transaction Security

The CID is never stored in the magnetic stripe or the EMV chip. This means that if a physical card is “skimmed” at a gas station or a compromised terminal, the thief might get the 15-digit card number, but they will not have the 4-digit CID required for online purchases. In the world of personal finance, this distinction is vital. It forces a higher level of verification for digital transactions, protecting the cardholder’s balance and the issuer’s liability.

The Secondary 3-Digit Code

Interestingly, many American Express cards also have a 3-digit code on the back. While this causes confusion for some users, it is rarely used for standard retail transactions. It primarily serves as a legacy security feature for specific internal processing or older verification systems. When an online merchant asks for your “Security Code” and you are using an Amex, you should almost always provide the 4-digit code on the front.

Decoding the Logic: The Mathematics of Your Card

To the average user, the numbers on a card are just a way to pay for groceries or flights. To a financial analyst, these numbers represent a complex system of error-checking and data integrity.

The Major Industry Identifier (MII)

The financial world is divided into sectors. For example, cards starting with 1 or 2 are usually issued by airlines, while those starting with 4 are Visa cards (banking). By claiming the “3” series—specifically 34 and 37—American Express solidified its identity as a travel and entertainment (T&E) and financial services powerhouse. This specific numbering helps international payment gateways recognize the card’s routing requirements instantly, ensuring that a purchase made in Tokyo on an Amex issued in New York is processed with minimal latency.

The Luhn Algorithm: Preventing Human Error

The 15th digit of an American Express card is the result of the Luhn formula (also known as the “mod 10” algorithm). This is a simple checksum formula used to validate a variety of identification numbers.

When you type your 15-digit Amex number into a website, the site’s backend immediately runs the Luhn check. If you accidentally swapped two numbers or missed a digit, the sum will not match the check digit, and the site will tell you the card number is invalid before even attempting to contact American Express. This reduces unnecessary traffic on financial networks and provides immediate feedback to the consumer, streamlining the digital payment experience.

Practical Application: Managing Your Amex Card Digitally

In the modern era of personal finance, the physical numbers on your card are becoming secondary to how those numbers are managed in the digital space. American Express has been a leader in integrating their unique numbering system with advanced financial tools.

Using Virtual Card Numbers

One of the most effective ways to protect your 15-digit account number is through the use of virtual card numbers. Many Amex cardholders can now generate temporary, merchant-specific numbers for online shopping. These virtual numbers function as a “proxy.” Even though they are not the 15 digits printed on your physical plastic or metal card, they are linked to your account. This allows you to shop on unfamiliar websites without exposing your primary financial data.

Mobile Wallets and Tokenization

When you add your American Express card to Apple Pay, Google Pay, or Samsung Pay, the 15-digit number is not actually stored on your phone or transmitted to the merchant. Instead, a process called “tokenization” occurs.

The payment network replaces your card number with a unique “token”—a different 15-digit string—that is specific to that device. If a hacker were to breach a merchant’s database, they would only find the token, which is useless outside of that specific device-merchant relationship. This technology has revolutionized the security of personal finance, making the physical numbers on the card a fallback rather than the primary method of data exchange.

Strategic Financial Benefits: Why Amex Stands Apart

The unique numbering and structure of American Express are symbolic of its broader business model. Unlike Visa or Mastercard, which are primarily payment networks that allow banks (like Chase or Wells Fargo) to issue cards, American Express is a “closed-loop” network. They are the bank, the issuer, and the network.

Charge Cards vs. Credit Cards

Many of American Express’s most famous offerings, such as the Platinum Card®, were traditionally “charge cards” rather than “credit cards.” While credit cards have a pre-set spending limit and allow you to carry a balance with interest, charge cards were designed to be paid in full every month.

Although Amex now offers many traditional credit products and “Plan It” features that allow for carrying balances, the 15-digit numbering system remains a hallmark of their legacy. This closed-loop system allows Amex to gather more data on consumer spending habits, which in turn allows them to offer more personalized rewards, higher levels of fraud protection, and a more integrated financial management tool for the cardholder.

Building a Premium Credit Profile

For those looking to optimize their financial health, the American Express ecosystem is often seen as a destination for “premium” credit. Because of their unique 15-digit structure and their status as an independent network, Amex cards often come with different perks, such as extensive travel insurance, purchase protection, and concierge services.

Understanding the “how” and “why” of your Amex card numbers is the first step in mastering the tool itself. Whether it is the 15-digit account number that identifies you to the world, the 4-digit CID that protects your online purchases, or the tokenized digits in your mobile wallet, these numbers are the foundation of a sophisticated financial strategy. By recognizing these differences, consumers can better protect their identities and leverage their American Express cards to their full financial potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.