In today’s fast-paced digital economy, the speed and efficiency of financial transactions are paramount. Venmo, a ubiquitous peer-to-peer payment app, has revolutionized how millions send and receive money, transforming everything from splitting dinner bills to sending rent payments. However, a common question often arises for users and businesses alike: “How long does it really take Venmo to transfer money to my bank account?” The answer, while seemingly straightforward, involves a nuanced understanding of payment processing, banking protocols, and user choices. For anyone managing personal finances, tracking online income, or overseeing business finance, grasping these timelines is critical for effective cash flow management and financial planning. This article delves into the specifics, offering a comprehensive guide to Venmo’s transfer speeds and the factors that influence them, all from the perspective of sound financial management.

Deciphering Venmo’s Transfer Speeds: Standard vs. Instant Options

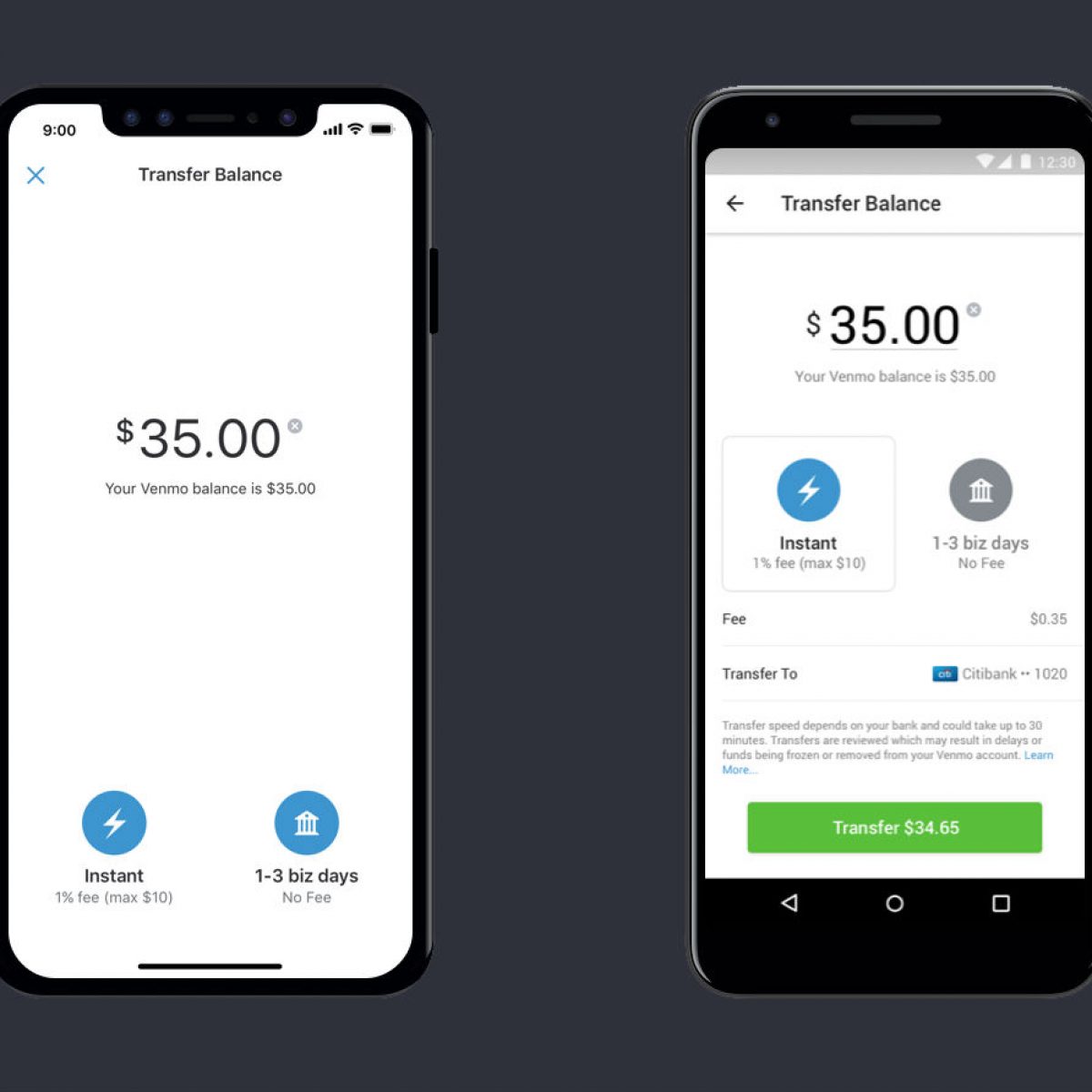

Venmo offers users two primary methods for transferring funds from their Venmo balance to an external bank account: the standard transfer and the instant transfer. Each option comes with its own set of expectations regarding speed, cost, and convenience, directly impacting your personal finance strategy.

The Standard Transfer: A Reliable, Cost-Free Option

The standard transfer is Venmo’s default and most commonly used method for moving money to a linked bank account. This option is entirely free of charge, making it an attractive choice for those who are not in an immediate rush to access their funds. Typically, a standard transfer will take 1 to 3 business days to complete.

“Business days” are a crucial distinction here. They refer to weekdays (Monday through Friday), excluding federal holidays. If you initiate a standard transfer on a Friday evening, for example, the processing won’t begin until the following Monday, and the funds might not appear in your bank account until Wednesday or Thursday of the next week. This timeline is heavily influenced by the Automated Clearing House (ACH) network, the electronic system that facilitates most bank-to-bank transfers in the United States. While reliable, the ACH network operates in batches and has specific cut-off times, leading to the observed multi-day processing window. For individuals managing their budgets or expecting online income, understanding this lag is essential for avoiding overdrafts or liquidity issues.

The Instant Transfer: Paying for Immediate Access

For those moments when immediate access to funds is critical – perhaps to cover an unexpected expense, make a quick investment, or pay a pressing bill – Venmo offers the instant transfer option. As the name suggests, this method aims to deposit money into your linked debit card-eligible bank account (or even a pre-approved prepaid debit card) within minutes, typically within 30 minutes.

The trade-off for this speed is a fee. Venmo charges a percentage of the transferred amount for instant transfers, typically 1.75% of the transfer amount, with a minimum fee of $0.25 and a maximum fee of $25.00. While this fee can seem negligible for smaller amounts, it can add up quickly for larger transfers. From a personal finance standpoint, it’s a direct cost to consider. Weighing the urgency of your need against this transaction cost is a fundamental aspect of financial decision-making. Is the immediate availability of funds worth the fee, or can you plan ahead and utilize the free standard transfer? This choice often comes down to individual financial situations and cash flow demands.

The Underlying Mechanism: How Banks Communicate

Regardless of whether you choose a standard or instant transfer, the underlying infrastructure relies on sophisticated banking communication systems. Standard transfers predominantly use the ACH network, which is a batch processing system. Banks collect transfer requests throughout the day and process them in large groups, leading to the 1-3 business day window. Instant transfers, conversely, leverage debit card networks, which are designed for real-time authorization and settlement, similar to how point-of-sale transactions work. This allows for much faster fund availability, albeit with associated network fees that Venmo passes on to the user. Understanding these mechanisms helps demystify why transfers take the time they do and highlights the inherent costs associated with financial infrastructure that enables such rapid money movement.

Key Factors Influencing Your Venmo Transfer Timeline

While Venmo provides general timelines, several factors can influence the actual speed at which funds arrive in your bank account. Being aware of these variables is crucial for anyone relying on Venmo for managing personal finances, investing online income, or handling business expenses.

Your Linked Bank Account’s Processing Policies

The bank you use plays a significant role in the transfer timeline. While Venmo initiates the transfer swiftly, your bank has its own internal processing policies and cut-off times. Some banks may process incoming ACH transfers several times a day, while others might only do so once a day. Similarly, banks have varying schedules for making deposited funds available to customers. Even after a transfer “completes” from Venmo’s perspective, your bank might hold the funds for a few hours or even a day before they reflect in your available balance. This is particularly relevant for standard transfers. For instant transfers, while the funds are usually sent immediately, minor delays can still occur if your bank’s system is experiencing heavy traffic or undergoes maintenance.

The Impact of Weekends and Banking Holidays

One of the most common reasons for perceived delays in standard transfers is the timing relative to weekends and banking holidays. As mentioned, the 1-3 “business days” metric explicitly excludes Saturdays, Sundays, and federal holidays. If you initiate a transfer on a Thursday, funds might not arrive until Monday or Tuesday. A transfer initiated before a long holiday weekend (e.g., Thanksgiving) could take even longer, potentially extending to five or more calendar days. For individuals and small businesses managing payroll or recurring payments, factoring in these non-business days is paramount to prevent shortfalls or missed deadlines. Financial planning must always account for these calendar-based nuances.

Venmo Account Verification Status and Transaction Limits

Venmo has various security measures and limits in place, which can sometimes affect transfer speeds. Unverified accounts, for instance, often have lower weekly transfer limits and may be subject to additional scrutiny, potentially causing minor delays. To expedite transfers and access higher limits, it’s always recommended to fully verify your Venmo account by linking and confirming a bank account, providing your social security number, and verifying your identity. An account that is not fully verified might trigger security reviews for larger transfers, impacting the timeline. Understanding these limits is critical for managing larger online income deposits or substantial personal finance movements.

Security Reviews and Transaction Holds

In its commitment to prevent fraud and maintain the security of its platform, Venmo occasionally places holds on transfers for review. This can happen if a transaction is flagged as unusual or suspicious, if there’s a significant change in your transfer patterns, or if the amount is particularly large. While these reviews are for your protection, they can undeniably cause delays. If a hold occurs, Venmo typically notifies the user and may request additional information. While frustrating, these security protocols are a standard part of financial tools designed to safeguard funds against illicit activities, aligning with broader financial security best practices.

Strategic Financial Management: Optimizing Your Venmo Experience

Leveraging Venmo effectively requires more than just knowing how to send and receive money; it involves strategic financial management to ensure transfers align with your personal and business financial goals.

Choosing the Optimal Transfer Method for Your Needs

The decision between a standard and an instant transfer is a core element of financial planning. If you’re managing regular income from side hustles, planning to invest, or simply moving money between your digital wallet and savings account, and you have a few days to spare, the free standard transfer is the financially prudent choice. The accumulated fees from frequent instant transfers can erode your earnings over time. However, if an emergency arises, an immediate bill needs payment, or you need instant cash flow for a critical business expense, the instant transfer, despite its fee, becomes a valuable financial tool. Always assess the urgency versus the cost.

Proactively Verifying Account Information

One of the simplest ways to ensure smooth and swift transfers is to proactively verify all your account information. This includes linking and confirming your bank account (using the micro-deposit method or instant verification) and ensuring your personal details are up-to-date. A fully verified account not only unlocks higher transfer limits but also minimizes the chances of delays due to security checks, allowing for more predictable financial transactions.

Monitoring Your Funds: Transaction Tracking and Alerts

Venmo provides a transaction history and status updates within the app. Regularly checking this section for ongoing transfers can provide peace of mind and alert you to any unexpected delays. While Venmo doesn’t offer bank-level alerts for deposits, setting up notifications from your linked bank account for incoming deposits can serve as an effective way to know the moment your Venmo funds become available. This proactive monitoring is a basic yet effective habit for managing any form of online income or digital payments.

Leveraging Venmo’s Direct Deposit and Debit Card Features

For those who frequently use Venmo or receive substantial online income through it, exploring its extended financial utility can be beneficial. Venmo now offers direct deposit functionality, allowing users to have their paychecks directly deposited into their Venmo balance. This can bypass the need for transfers altogether for funds meant to stay within the Venmo ecosystem or for immediate spending via the Venmo Debit Card. The Venmo Debit Card directly uses your Venmo balance, offering instant access to your funds without any transfer fees or waiting periods, functioning similarly to a traditional bank debit card but tied to your Venmo wallet. For many, this integrates Venmo more deeply into their daily financial toolkit, turning it into a primary spending account.

Troubleshooting Transfer Delays and Ensuring Financial Security

Even with careful planning, occasional delays can occur. Knowing how to troubleshoot these situations and, more broadly, how to maintain financial security on Venmo is paramount for any user.

What to Do When Funds Are Delayed

If a standard transfer exceeds the typical 1-3 business day window, or an instant transfer takes longer than 30 minutes, there are steps you can take:

- Check Venmo App Status: First, verify the transfer status within your Venmo app. It will indicate if the transfer is “pending,” “completed,” or if there’s an issue.

- Contact Your Bank: If Venmo shows the transfer as “completed,” but the funds aren’t in your account, contact your bank. They can confirm if a pending deposit is in their system or if there’s an internal hold.

- Contact Venmo Support: If both the Venmo app and your bank provide no clear answer, reach out to Venmo’s customer support. They can investigate the specific transaction and provide clarity on any holds or processing issues on their end. Having transaction IDs and dates ready will expedite this process.

Safeguarding Your Venmo Account and Funds

Beyond transfer speeds, maintaining the security of your Venmo account is crucial for protecting your financial assets.

- Strong, Unique Passwords: Use a complex password and enable two-factor authentication.

- Beware of Scams: Be vigilant against phishing attempts and scams. Venmo will never ask for your password or personal information via email or text.

- Only Send to Trusted Individuals: Venmo is designed for payments between friends and family. Exercise caution when sending money to strangers for goods or services, as Venmo does not offer buyer/seller protection for such transactions. This is a critical distinction from other payment platforms like PayPal, and understanding it is fundamental to responsible money management on the platform.

- Monitor Activity: Regularly review your transaction history for any unauthorized activity.

The Importance of Accurate Information for Smooth Transfers

Finally, ensuring all information is correct before initiating any transfer is a fundamental practice for preventing delays. Double-check the recipient’s Venmo username, the transfer amount, and, most importantly, that the correct bank account or debit card is linked and selected for outgoing transfers. Even a minor typo can lead to a canceled transfer or, in worse cases, funds being sent to an incorrect destination, requiring arduous and time-consuming recovery efforts. Precision in data entry is a simple yet incredibly effective way to ensure your financial transactions on Venmo proceed smoothly and without hitches.

In conclusion, while Venmo has undeniably simplified peer-to-peer payments, understanding the mechanics of its transfer options, the factors influencing their speed, and best practices for financial management empowers users to leverage the platform most effectively. By making informed choices, verifying accounts, and staying vigilant, individuals and businesses can ensure their Venmo transfers are not just fast, but also secure and financially sound.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.