Understanding how your Social Security income is calculated is a crucial step in planning for your financial future. Far from being a simple fixed amount, your future benefit is a complex interplay of your earnings history, the age at which you claim benefits, and a system designed to provide a baseline of income for retirees, disabled workers, and survivors. For most Americans, Social Security represents a vital component of their retirement income, and demystifying its calculation process empowers individuals to make informed decisions about their claiming strategy and overall financial well-being. This article will delve into the intricacies of how your Social Security retirement benefit is determined, breaking down the key components and factors that influence its ultimate size.

The Foundation: Your Earnings Record

The bedrock of your Social Security benefit calculation lies in your lifetime earnings. The Social Security Administration (SSA) tracks your earnings in covered employment throughout your working life. Not all income is subject to Social Security taxes, however. Only income up to a certain annual limit – known as the Social Security wage base – is considered. This wage base adjusts annually to reflect changes in average wages in the economy. For instance, in 2023, the wage base was $160,200, meaning earnings above this amount did not contribute to your Social Security record for that year.

Identifying Your “Covered” Earnings

To be eligible for Social Security benefits, you must have earned a sufficient number of “credits” throughout your working life. For most workers, you earn one credit for every $1,640 in earnings in 2023. You can earn a maximum of four credits per year, meaning you need to earn $6,560 in 2023 to get the maximum four credits for that year. To qualify for retirement benefits, you generally need 40 credits, which translates to about 10 years of work. However, the number of credits required can vary depending on when you reach age 62, become disabled, or die. The SSA meticulously maintains your earnings history, accessible through your “my Social Security” account on their website. Regularly reviewing this record is essential to ensure accuracy. Any discrepancies, such as missing jobs or incorrect reported wages, should be promptly reported to the SSA to avoid impacting your future benefit calculation.

Averaging Your Highest Earning Years

Once your covered earnings are established, the SSA then looks at your entire earnings history to determine your Average Indexed Monthly Earnings (AIME). This involves a multi-step process. First, your annual earnings are “indexed” to account for changes in average wages over time. This means that your earnings from earlier in your career are adjusted to reflect their value in today’s economy. This indexing is crucial because it ensures that your past earnings are given fair consideration relative to more recent earnings.

After indexing, the SSA identifies your 35 highest-earning years. If you have fewer than 35 years of covered earnings, any years with zero earnings will be included in the average, thus lowering your AIME. This is why consistently working and contributing to Social Security throughout your career is so important. The SSA then sums up the indexed earnings for these 35 years and divides by 420 (the number of months in 35 years) to arrive at your AIME. This AIME is the average monthly income on which your benefit is calculated. It’s important to note that the SSA only uses earnings up to the annual wage base in each of those 35 years.

The Primary Insurance Amount (PIA): The Core Benefit

The AIME is then used to calculate your Primary Insurance Amount (PIA). The PIA represents the benefit you would receive if you claim retirement benefits at your Full Retirement Age (FRA). The calculation of your PIA is based on a progressive formula. This formula is designed to replace a larger percentage of income for lower-earning workers than for higher-earning workers, reflecting the program’s goal of providing a safety net.

Understanding the PIA Formula Brackets

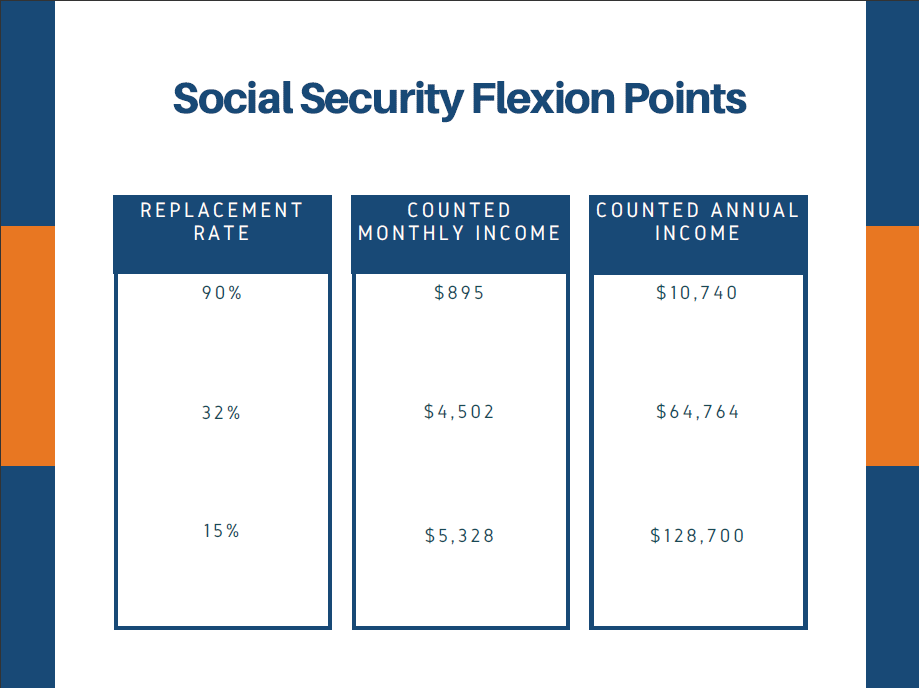

The PIA formula uses three “bend points” that divide your AIME into different portions, each subject to a different replacement rate. These bend points are adjusted annually. For example, for someone reaching age 62 in 2024, the formula works as follows:

- 90% of the first $1,174 of your AIME: This is the largest portion of your AIME, and it’s replaced at the highest rate.

- 32% of your AIME between $1,174 and $7,078: This middle portion is replaced at a significantly lower rate.

- 15% of your AIME over $7,078: This top portion of your AIME is replaced at the lowest rate.

To calculate your PIA, you would multiply each portion of your AIME by its corresponding percentage and then sum the results. For instance, if your AIME was $4,000, you would calculate: (0.90 * $1,174) + (0.32 * ($4,000 – $1,174)) + (0.15 * ($4,000 – $7,078)). Since the last term would be negative, it would be calculated as 0 for this example. The result of this calculation is your PIA. This PIA is the amount you would receive if you start collecting benefits exactly at your Full Retirement Age.

The Role of Cost-of-Living Adjustments (COLAs)

Once your PIA is established, it’s important to understand that it’s not static throughout your retirement. Social Security benefits are subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help your benefit keep pace with inflation, ensuring that your purchasing power doesn’t erode over time. The annual COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If inflation increases, your Social Security benefit will typically increase the following year to reflect that rise. This mechanism is a crucial feature of the Social Security program, providing a degree of financial security against rising living costs in retirement.

Claiming Age: The Impact of Early or Delayed Retirement

While your PIA is the foundation of your benefit, the age at which you choose to start receiving Social Security retirement benefits significantly alters the monthly amount you receive. You can begin receiving retirement benefits as early as age 62, but doing so results in a permanently reduced benefit. Conversely, delaying benefits beyond your Full Retirement Age can lead to substantial increases in your monthly payments.

Early Retirement Reductions

If you claim benefits before your Full Retirement Age (FRA), your monthly benefit will be permanently reduced. The reduction is calculated based on the number of months you claim early. For each month before your FRA, your benefit is reduced by a fraction of a percent. For example, if your FRA is 67, and you claim at age 62, you would be claiming 60 months early. This would result in a reduction of approximately 30% of your PIA. This reduction is applied for the entire duration of your retirement, meaning you will receive a lower monthly payment for the rest of your life. The SSA provides detailed charts and calculators to illustrate these reductions based on your specific FRA.

Delayed Retirement Credits

On the other hand, delaying your retirement past your Full Retirement Age earns you Delayed Retirement Credits (DRCs). For each month you delay receiving benefits beyond your FRA, up to age 70, your benefit amount increases. The credit rate is typically 8% per year, meaning that if your FRA is 67 and you wait until age 70 to claim, your benefit could be as much as 24% higher than your PIA. These credits are a powerful incentive for individuals who can afford to work longer and can significantly boost their long-term retirement income. It’s important to note that DRCs stop accumulating once you reach age 70. Therefore, there is no financial advantage to delaying benefits beyond that age.

Other Factors Influencing Your Benefit

Beyond your earnings history and claiming age, several other factors can influence the amount of Social Security income you receive. These include your marital status, whether you have dependent children, and if you are also receiving other forms of Social Security benefits.

Spousal and Survivor Benefits

Social Security not only provides benefits for retired workers but also for their spouses and survivors. Spousal benefits allow a spouse to receive up to 50% of the primary earner’s PIA, provided certain conditions are met, such as being married for at least one year. Survivor benefits are paid to eligible family members, such as a widow or widower, minor children, or dependent parents, upon the death of a worker. These benefits are also calculated based on the deceased worker’s earnings record and can provide crucial financial support to families. The specific percentages and eligibility requirements for these benefits are detailed on the SSA’s website.

Windfall Elimination Provision (WEP) and Government Pension Offset (GPO)

For individuals who also receive a pension from work not covered by Social Security (such as some state or local government jobs), two provisions – the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) – can affect their Social Security benefit. The WEP can reduce the Social Security benefit of a worker who also has a pension from non-covered employment. The GPO reduces spousal and survivor benefits if the recipient also receives a pension from government work. These provisions are complex, and their application can significantly impact your net Social Security income, making it essential to understand how they might apply to your situation.

In conclusion, the calculation of your Social Security income is a multi-faceted process. It begins with your lifetime earnings, which are indexed and averaged over your 35 highest-earning years to determine your Average Indexed Monthly Earnings (AIME). This AIME is then used in a progressive formula to calculate your Primary Insurance Amount (PIA), the benefit you’d receive at your Full Retirement Age. Crucially, your claiming age—whether you opt for early retirement, wait until your FRA, or delay further—will permanently adjust your monthly benefit amount through reductions or delayed retirement credits. Understanding these core components, along with other potential influences like spousal/survivor benefits and provisions like WEP/GPO, is paramount for effectively planning your retirement and maximizing your Social Security income. Regularly checking your Social Security statement and consulting with the SSA or a financial advisor can provide personalized insights into your specific benefit calculation and claiming strategies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.