For many Americans, Social Security represents the most significant component of their retirement income strategy. Yet, despite its importance, the specific mechanics of how the Social Security Administration (SSA) arrives at a monthly benefit amount remain a mystery to most. Understanding the “how” behind the calculation is not merely an academic exercise; it is a vital component of personal finance that allows you to make informed decisions about when to retire, how much to save in private accounts, and how to maximize your lifetime wealth.

The calculation is a multi-step process that involves indexing your lifetime earnings, determining your average monthly income over your most productive years, and applying a progressive formula to ensure the system remains a social safety net. This article provides an in-depth exploration of the Social Security calculation process, offering the insight needed to navigate your financial future.

The Foundation: Average Indexed Monthly Earnings (AIME)

The journey to your Social Security check begins with your entire work history. However, the SSA does not simply look at your last paycheck or your highest year of earnings. Instead, they look at your “Average Indexed Monthly Earnings” (AIME).

The 35-Year Rule

The first critical factor in the calculation is the timeframe. The Social Security formula is based on your 35 highest-earning years. If you have worked for 40 years, the SSA will disregard the five years where you earned the least. Conversely, if you have only worked for 25 years, the SSA will factor in 10 years of “zero” earnings. These zeros can significantly drag down your average, making it a priority for many workers to reach at least that 35-year milestone to maximize their potential payout.

Inflation Indexing (The Indexing Factor)

Because $20,000 earned in 1980 had much more purchasing power than $20,000 earned today, the SSA applies an “indexing factor” to your historical earnings. This process adjusts your past wages to reflect the general increase in wage levels that has occurred since the earnings were received.

Each year’s earnings are multiplied by an index factor based on the year you turn 60. Earnings from age 60 and later are taken at face value. Once all years are indexed, the SSA selects the 35 highest years, sums them up, and divides by 420 (the number of months in 35 years). The resulting figure is your AIME, the baseline for the rest of the calculation.

The Calculation Formula: Primary Insurance Amount (PIA)

Once your AIME is established, the SSA applies a specific formula to determine your Primary Insurance Amount (PIA). The PIA is the base amount you would receive if you chose to begin receiving benefits at your Full Retirement Age (FRA).

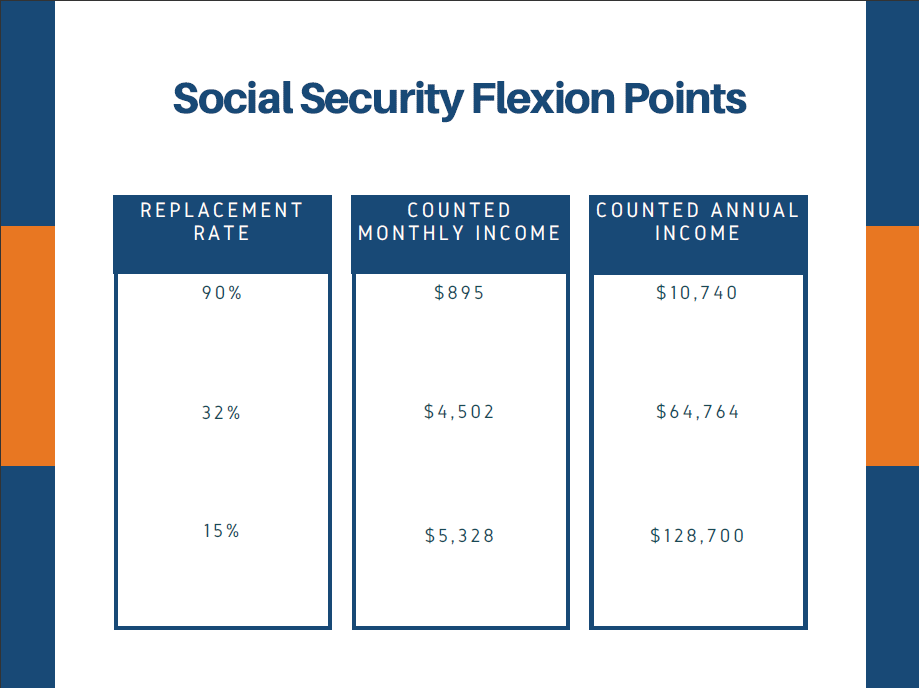

The “Bend Points” Explained

The Social Security formula is intentionally progressive, meaning it replaces a higher percentage of income for lower-earning workers than for higher-earning workers. This is achieved through “bend points,” which are dollar thresholds updated annually by the SSA.

For a worker reaching age 62 in 2024, the PIA formula looks like this:

- 90% of the first $1,174 of AIME.

- 32% of AIME between $1,174 and $7,078.

- 15% of AIME above $7,078.

The sum of these three figures is rounded down to the nearest dime to become the PIA. This structure ensures that while high earners receive a larger check in absolute terms, the “replacement rate” of their pre-retirement income is significantly lower than that of a low-wage worker.

The Maximum Taxable Earnings Limit

It is important for high-income earners to note that not all income is factored into the AIME or the PIA. Social Security taxes (FICA) are only applied up to a certain limit each year—known as the Maximum Taxable Earnings. In 2024, this limit is $168,600. Any income earned above this threshold is neither taxed for Social Security nor included in the calculation for benefits. This creates a “cap” on the maximum possible Social Security benefit anyone can receive.

The Impact of Timing: When You Choose to File

Your PIA is the amount you get if you file at exactly your Full Retirement Age (FRA). However, very few people file at that exact moment. The decision of when to claim benefits—anywhere from age 62 to 70—is one of the most consequential financial decisions a retiree can make.

Full Retirement Age (FRA)

Your FRA depends on your birth year. For those born in 1960 or later, the FRA is 67. If you file before this age, your benefits are permanently reduced. If you file after this age, your benefits are permanently increased.

Early Filing Penalties

You can begin taking Social Security as early as age 62, but there is a steep price for doing so. The SSA reduces your benefit by a fraction of a percent for each month before your FRA. For someone with an FRA of 67, filing at age 62 results in a 30% reduction in their monthly check. This reduction is permanent and will only be adjusted for future Cost-of-Living Adjustments (COLA). From a financial planning perspective, filing early is often only recommended if there are immediate liquidity needs or health concerns that suggest a shorter-than-average life expectancy.

Delayed Retirement Credits

On the other side of the spectrum, you can choose to delay benefits past your FRA. For every year you wait—up to age 70—your benefit increases by 8% per year in “delayed retirement credits.” For someone with an FRA of 67, waiting until 70 results in a 24% increase over their PIA. In the world of personal finance, a guaranteed 8% annual return is nearly impossible to find elsewhere, making the decision to delay a powerful tool for those who have other assets (like a 401k or IRA) to bridge the gap in the meantime.

Beyond the Basics: Variables That Affect Your Final Check

While the AIME and PIA form the core of the calculation, several external factors can alter the actual amount that lands in your bank account.

The Retirement Earnings Test

If you choose to collect Social Security before your Full Retirement Age while still working, your benefits may be temporarily withheld. For 2024, if you are under FRA for the entire year, the SSA deducts $1 from your benefit payments for every $2 you earn above $22,320.

It is a common misconception that this money is lost forever. Once you reach your FRA, the SSA recalculates your benefit amount to account for the months benefits were withheld, effectively “giving back” the money over time through a higher monthly check. However, for immediate cash flow management, this is a critical variable to track.

Taxation of Benefits (Provisional Income)

For many retirees, Social Security is not tax-free. Your “provisional income”—the sum of your adjusted gross income, tax-exempt interest, and 50% of your Social Security benefits—determines if you owe federal income tax on your benefits.

- If you are a single filer with provisional income between $25,000 and $34,000, you may pay tax on up to 50% of your benefits.

- Above $34,000, up to 85% of your benefits may be taxable.

Understanding these thresholds is essential for tax-bracket management in retirement, as it may influence whether you withdraw money from a Roth IRA or a traditional 401k in a given year.

Cost-of-Living Adjustments (COLA)

Social Security is one of the few retirement income sources that is indexed for inflation. Every October, the SSA announces the COLA for the following year based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While this doesn’t change the underlying calculation of your PIA, it ensures that your purchasing power remains relatively stable throughout your retirement years.

Strategic Financial Planning and the Calculation

Understanding how Social Security is calculated allows for more sophisticated wealth management. When you view Social Security as an inflation-indexed annuity, its role in your portfolio changes.

For many, Social Security serves as the “floor” for their retirement income. By knowing your PIA and the impact of filing ages, you can calculate your “gap”—the difference between your Social Security benefit and your desired retirement lifestyle. This gap determines your necessary withdrawal rate from your private investments.

Furthermore, for married couples, the calculation becomes a joint optimization problem. Strategies such as having the higher-earning spouse delay benefits until age 70 can maximize the survivor benefit for the remaining spouse, providing a form of longevity insurance that is difficult to replicate with private market products.

In conclusion, the calculation of Social Security is a complex but logical process. It rewards long-term consistency through the 35-year rule, offers a safety net through progressive bend points, and provides a significant incentive for patience through delayed retirement credits. By mastering these mechanics, you transition from a passive recipient to an active architect of your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.