In the world of personal finance and investment, numbers are the primary language. Whether you are tracking a stock market correction, negotiating a lower interest rate on a loan, or streamlining your business overhead, the ability to calculate a percentage reduction is more than just a basic math skill—it is a fundamental pillar of financial literacy. Understanding the mechanics of how values decrease allows you to make informed decisions that protect your capital and maximize your purchasing power.

When we talk about “working out a percentage reduction,” we are essentially measuring the rate of change between two points in time. In financial terms, this represents everything from the “off” price during a seasonal sale to the “drawdown” of a retirement portfolio during a bear market. Mastering this calculation empowers you to see past marketing gimmicks and focus on the raw data that dictates your net worth.

The Mathematical Foundation of Financial Reductions

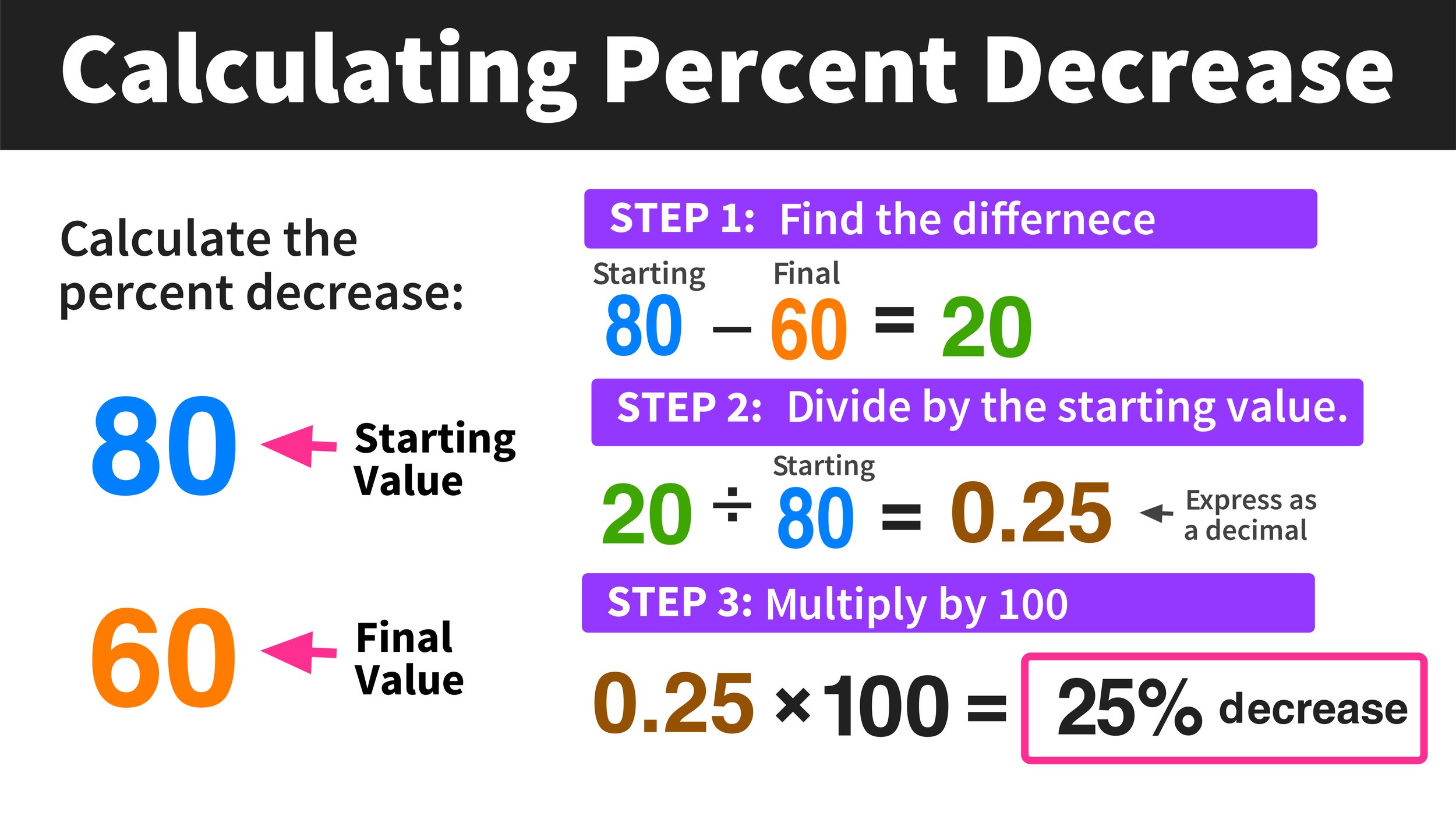

Before diving into complex investment strategies, one must master the basic formula. In finance, a percentage reduction represents the decrease from an original value to a new, lower value, expressed as a part of every hundred.

The Standard Percentage Reduction Formula

To calculate the percentage reduction, you follow a simple three-step process:

- Subtract the new value from the original value to find the “decrease.”

- Divide that decrease by the original value.

- Multiply the resulting decimal by 100 to get the percentage.

Mathematically, it looks like this:

[(Original Price - New Price) / Original Price] x 100 = % Reduction

Why the “Original Value” Matters

A common mistake in personal finance is dividing by the new value instead of the original one. For example, if a stock drops from $100 to $80, the reduction is $20. Dividing $20 by the original $100 gives you a 20% reduction. If you mistakenly divided by $80, you would get 25%, which provides a distorted view of your portfolio’s performance. In the realm of money, accuracy is the difference between a calculated risk and a costly error.

Real-World Budgeting Applications

In daily money management, applying this formula helps in auditing your recurring expenses. If you negotiate your monthly internet bill down from $90 to $75, you have achieved a 16.6% reduction. By applying this calculation across all your utility bills and subscriptions, you can quantify your “savings efficiency,” a metric that many high-net-worth individuals use to ensure their lifestyle inflation remains in check.

Navigating the Stock Market: Portfolio Drawdowns and the Math of Recovery

For investors, the percentage reduction is most commonly referred to as a “drawdown.” Understanding how to calculate this is vital for risk management and for setting “stop-loss” orders to protect your principal investment.

Calculating Market Volatility

When the market enters a period of volatility, investors often see the value of their holdings fluctuate. If your brokerage account was worth $50,000 at its peak and has since fallen to $42,000, calculating the percentage reduction ($8,000 / $50,000 = 16%) helps you determine if the dip is a standard market correction (usually 10%) or the beginning of a bear market (20% or more). This distinction is critical for deciding whether to “hold the line” or rebalance your assets into safer havens like bonds or high-yield savings accounts.

The Asymmetry of Loss and Gain

One of the most important lessons in finance is that percentage reductions are harder to recover from than they are to incur. This is known as the “Math of Recovery.” If your investment suffers a 50% reduction, you do not need a 50% gain to get back to even; you need a 100% gain.

- 10% loss requires an 11.1% gain to break even.

- 20% loss requires a 25% gain to break even.

- 50% loss requires a 100% gain to break even.

- 90% loss requires a 900% gain to break even.

Understanding this asymmetry highlights why successful investors focus so heavily on “downside protection.” By calculating and limiting your percentage reduction through diversification, you ensure that your money doesn’t have to work twice as hard just to return to its starting point.

Using Reductions to Identify Value (Buying the Dip)

On the flip side, a percentage reduction in the price of a high-quality asset can represent a “buy” signal. Savvy investors look for a “discount to intrinsic value.” If you believe a company is fundamentally worth $200 per share, but a temporary market panic has caused a 30% reduction in price to $140, you are presented with a margin of safety. In this context, calculating the reduction isn’t about tracking loss; it’s about identifying opportunity.

Strategic Debt Management and Interest Rate Reduction

Beyond investing, the concept of percentage reduction is a powerful tool in debt elimination. Whether it is a mortgage, a car loan, or credit card debt, reducing the “cost of capital” is the fastest way to increase your monthly cash flow.

Negotiating Interest Rates

Interest rates are essentially the “price” of borrowing money. If you have a credit card with an 18% APR and you successfully negotiate it down to 15%, you have achieved a 16.6% reduction in your cost of borrowing. While three percentage points might seem small, the cumulative effect on a $10,000 balance over several years can save thousands of dollars. Calculating these reductions allows you to prioritize which debts to pay off first—a strategy often called the “Debt Avalanche” method.

The Impact of Principal Reduction on Long-Term Interest

Making extra payments toward the principal of a loan creates a percentage reduction in the total interest paid over the life of the loan. For instance, on a 30-year mortgage, a small reduction in the principal during the first five years can lead to a massive percentage reduction in the total duration of the loan. By using a financial calculator to work out these percentages, homeowners can visualize how a 10% increase in monthly payments can lead to a 20% or 30% reduction in the total interest paid to the bank.

Debt-to-Income Ratio Optimization

Lenders use the Debt-to-Income (DTI) ratio to determine your creditworthiness. If your monthly debt payments are $2,000 and your income is $5,000, your DTI is 40%. By paying off a loan and reducing your monthly debt to $1,500, you have achieved a 25% reduction in your DTI. This percentage shift can move you from a “high-risk” borrower to a “prime” borrower, unlocking lower interest rates for future financing.

Business Finance: Optimizing Profit Margins through Cost Reduction

For entrepreneurs and small business owners, working out percentage reductions is a daily necessity for maintaining healthy profit margins. Efficiency is often found in the small percentages.

Identifying Overhead Inefficiencies

In business, “lean” operations are built on the continuous reduction of waste. By calculating the percentage reduction in “Cost of Goods Sold” (COGS), a business can significantly boost its net profit without increasing sales. If a manufacturer finds a new supplier that reduces raw material costs from $10.00 per unit to $8.50 per unit, that 15% reduction in cost flows directly to the bottom line.

Seasonal Discounting and Revenue Impact

Retail businesses must constantly work out percentage reductions for clearance sales. However, it is vital to calculate the “Breakeven Increase in Volume.” If you reduce your prices by 20%, you must calculate how many more units you need to sell to maintain the same gross profit. This ensures that a “reduction” in price doesn’t lead to a “reduction” in business viability.

Tax Liability and Credits

Tax planning is perhaps the most complex area of financial reduction. Tax credits offer a dollar-for-dollar reduction in the tax you owe, while deductions reduce your taxable income. Working out the percentage reduction in your “Effective Tax Rate” is the goal of every sophisticated wealth management plan. Moving from a 35% effective tax rate to a 28% rate via strategic investments (like municipal bonds or 401k contributions) represents a significant increase in spendable wealth.

Leveraging Tools and Automation for Financial Accuracy

While manual calculation is a great skill, the modern financial landscape offers tools that make tracking percentage reductions effortless. Using technology ensures that human error doesn’t lead to financial miscalculations.

Mastering Excel and Google Sheets for Finance

The most powerful tool in any financier’s arsenal is the spreadsheet. To calculate percentage reduction in Excel, you simply use the formula =(B1-A1)/A1, where A1 is the original price and B1 is the new price (note: this will give a negative number, indicating a decrease). Automating these calculations across a monthly budget or an investment tracker allows you to see real-time shifts in your financial health.

Utilizing Fintech Apps and Personal Finance Dashboards

Apps like Mint, You Need A Budget (YNAB), or Personal Capital do the math for you. They track your spending categories and alert you when there is a significant percentage reduction in your net worth or an increase in your spending. These tools are invaluable for maintaining a “macro” view of your money, allowing you to focus on strategy rather than arithmetic.

The Role of Financial Advisors

For high-stakes decisions—such as estate planning or corporate restructuring—it is often wise to consult with a financial advisor or CPA. They use professional-grade software to calculate “percentage of risk” and “tax drag,” ensuring that every reduction in your portfolio is calculated with precision. They help you understand that in the world of money, it isn’t just about how much you make, but how much you keep after every percentage reduction is accounted for.

By mastering the simple yet profound math of percentage reduction, you gain a clearer lens through which to view your financial world. Whether you are cutting costs, surviving a market dip, or paying down debt, the percentage is the pulse of your progress. Keep calculating, keep reducing your liabilities, and watch your wealth grow in proportion.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.