The transition from a traditional W-2 employee to a self-employed professional, freelancer, or small business owner is a milestone often marked by newfound freedom and creative control. However, with that independence comes a significant shift in financial responsibility: the burden of tax withholding shifts from an employer to you. Unlike employees who have taxes automatically deducted from every paycheck, the IRS operates on a “pay-as-you-go” system for the self-employed. This means you are required to pay estimated taxes in four installments throughout the year.

Understanding how to pay quarterly taxes is not just about staying compliant with the law; it is a fundamental component of professional cash flow management. Failing to account for these payments can lead to substantial underpayment penalties and a daunting tax bill come April. This guide explores the intricacies of estimated taxes, providing a roadmap for calculating, scheduling, and submitting your payments with confidence.

1. Determining Your Liability: Who Must Pay Quarterly?

The first step in mastering your financial obligations is determining whether the quarterly tax requirement applies to you. The Internal Revenue Service (IRS) generally requires individuals to make estimated tax payments if they expect to owe $1,000 or more in taxes when their return is filed.

Who Is Covered Under These Rules?

This requirement typically applies to sole proprietors, partners in a business, and S-corporation shareholders. If you are a freelancer, a “gig economy” worker (such as a ride-share driver or consultant), or an independent contractor receiving 1099-NEC forms, you are almost certainly responsible for quarterly payments. Additionally, if you have significant income from interest, dividends, alimony, or capital gains that isn’t subject to withholding, you may also need to pay estimated taxes even if you have a primary W-2 job.

The Safe Harbor Rule

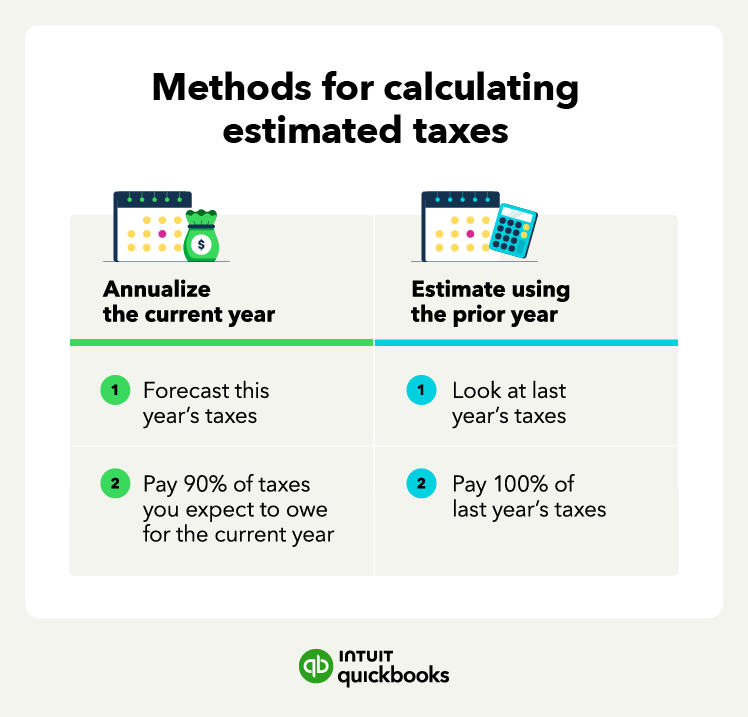

To avoid penalties, the IRS provides “safe harbor” guidelines. Generally, you will not face an underpayment penalty if you pay at least 90% of the tax shown on your current year’s return or 100% of the tax shown on your return from the prior year (whichever is smaller). For high-income earners—those with an adjusted gross income (AGI) over $150,000—the prior-year threshold increases to 110%. Understanding these benchmarks is critical for financial planning, as they provide a clear target to aim for, even if your income fluctuates significantly.

2. Calculating the Amount: The Math Behind the Payment

Calculating your quarterly taxes can feel like aiming at a moving target, especially if your income is unpredictable. However, accuracy is essential to ensure you aren’t overpaying (losing out on liquidity) or underpaying (risking penalties).

Estimating Net Income and Self-Employment Tax

The calculation begins with your estimated gross income minus your deductible business expenses. This gives you your net profit. From here, you must account for the Self-Employment (SE) tax, which currently sits at 15.3%. This rate covers Social Security (12.4%) and Medicare (2.9%). Because you act as both the employer and the employee, you are responsible for the full amount, though you can deduct the employer-equivalent portion (50%) when calculating your adjusted gross income.

Utilizing Form 1040-ES

The IRS provides a worksheet in Form 1040-ES (Estimated Tax for Individuals) specifically designed to help you navigate this math. You will factor in your expected adjusted gross income, taxable income, taxes, deductions, and credits. If you find your income varies wildly from month to month, you can use the “Annualized Income Installment Method.” This allows you to pay an amount based on what you actually earned during a specific period, which is particularly helpful for seasonal businesses or those just starting out.

Accounting for State and Local Taxes

It is a common mistake to focus solely on federal obligations. Most states that collect income tax also require quarterly estimated payments. The thresholds and deadlines often mirror federal rules, but they can vary. Ensure you consult your state’s Department of Revenue to determine their specific requirements, as state penalties for underpayment can be just as stringent as federal ones.

3. The Logistics: How and When to Submit Your Payments

Once you have calculated your liability, the next step is the physical act of payment. The IRS has modernized its systems, offering several ways to pay that range from traditional mail to instant digital transfers.

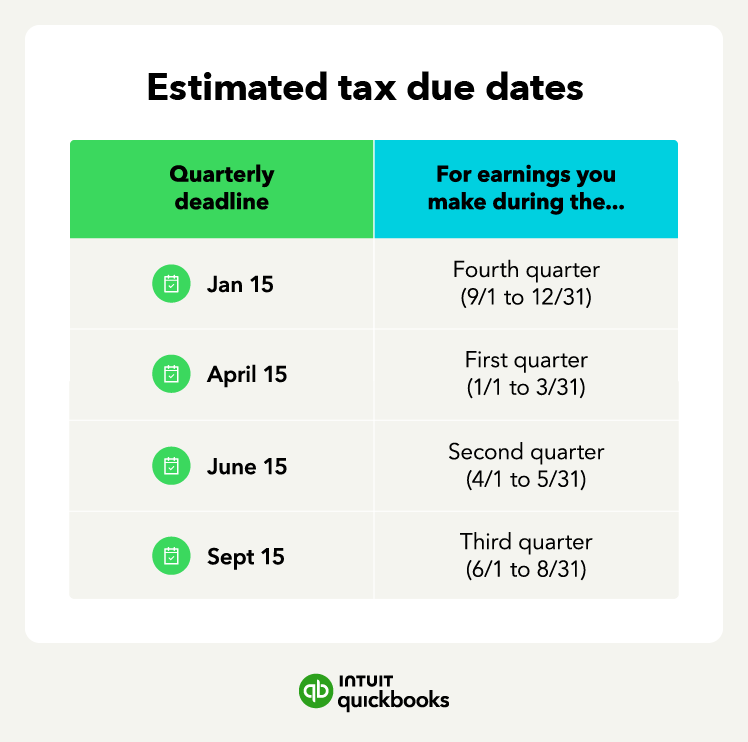

Key Deadlines to Remember

Quarterly taxes are not paid at the end of every three-month calendar quarter. Instead, the IRS follows a specific schedule:

- Q1 (Jan 1 – March 31): Due April 15

- Q2 (April 1 – May 31): Due June 15

- Q3 (June 1 – Aug 31): Due Sept 15

- Q4 (Sept 1 – Dec 31): Due Jan 15 of the following year

If these dates fall on a weekend or a legal holiday, the deadline is pushed to the next business day. Missing these deadlines by even a few days can trigger interest charges, so marking them prominently on your business calendar is a non-negotiable task.

Digital Payment Options

The most efficient way to pay is through IRS Direct Pay. This free service allows you to pay directly from your checking or savings account without any prior registration. For those who want more control and a history of their payments, the Electronic Federal Tax Payment System (EFTPS) is a robust alternative. While it requires a registration process and a mailed PIN, it allows you to schedule payments up to a year in advance—a massive benefit for those who want to “set it and forget it.”

Traditional Methods

If you prefer a paper trail, you can mail a check or money order along with the payment voucher from Form 1040-ES. While this is still a valid method, it carries the risk of mail delays or lost documents. If you choose this route, it is highly recommended to send the payment via certified mail with a return receipt requested to prove it was postmarked by the deadline.

4. Cash Flow Strategy: Managing Your Tax Reserve

The biggest challenge with quarterly taxes is not the math or the filing—it is having the cash on hand when the deadline arrives. Without a dedicated strategy, a $5,000 tax bill can cripple a small business’s operations.

The “Tax Bucket” System

The most effective way to manage this is to treat tax money as if it was never yours to begin with. Open a separate high-yield savings account specifically for taxes. Every time a client pays an invoice, immediately transfer a percentage (usually 25% to 30%) into that account. This ensures that when the quarterly deadline rolls around, the money is already set aside and has likely earned a small amount of interest in the meantime.

Adjusting for Growth

Business finance is dynamic. If you land a major contract in June, your previous estimates for Q3 and Q4 may no longer be accurate. It is wise to perform a “mid-year check-up” in July. Re-run your numbers based on your actual year-to-date earnings. Adjusting your remaining two payments upward can prevent a massive, unexpected bill when you file your annual return the following April.

5. Leveraging Financial Tools and Professional Advice

In the modern era of personal finance, you do not have to calculate these numbers on the back of a napkin. There is a vast ecosystem of tools designed to simplify the tax lives of the self-employed.

Accounting Software Integration

Platforms like QuickBooks Self-Employed, FreshBooks, and Xero offer features that automatically track your income and expenses. Many of these tools include a “tax logic” layer that estimates your quarterly liability in real-time based on your synced bank transactions. Some even allow you to pay your federal estimated taxes directly through the software interface, creating a seamless workflow between earning and reporting.

The Role of a CPA or Enrolled Agent

While software is helpful, it cannot replace the nuanced advice of a tax professional. A Certified Public Accountant (CPA) can help you identify deductions you might have missed—such as the home office deduction, health insurance premiums, or retirement account contributions (like a SEP IRA)—which directly lower your taxable income and, consequently, your quarterly payments. Engaging a professional is often an investment that pays for itself through tax savings and the avoidance of costly IRS audits.

Staying Informed on Legislative Changes

Tax laws are not static. Changes in standard deductions, tax brackets, or business-related credits can occur annually. For example, changes to the “Qualified Business Income” (QBI) deduction can significantly impact the bottom line for many freelancers. Staying engaged with reputable financial news sources or maintaining a relationship with a tax advisor ensures that your quarterly strategy evolves alongside the legal landscape.

By treating quarterly taxes as a routine business process rather than a sporadic crisis, you protect your business’s financial health. It requires discipline, a bit of math, and the right tools, but the result is a business that is not only profitable but also built on a foundation of professional financial integrity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.