Navigating the world of loans can often feel like deciphering a complex financial puzzle. Among the many terms and conditions, “interest” stands out as perhaps the most crucial to understand. It’s the cost of borrowing money, the premium you pay for the privilege of using someone else’s capital. For many, figuring out how interest is calculated on a loan can seem daunting, but it’s a fundamental aspect of financial literacy that empowers you to make informed decisions, save money, and manage your debt effectively.

This article will demystify loan interest, breaking down its core components, exploring different calculation methods, and providing practical insights into how you can effectively manage this critical financial element. Whether you’re considering a mortgage, an auto loan, a personal loan, or managing credit card debt, a solid grasp of interest calculations is your roadmap to financial clarity.

Understanding the Fundamentals of Loan Interest

Before we dive into the ‘how,’ it’s essential to establish a strong foundation of the ‘what’ and ‘why’ behind loan interest. By understanding the basic building blocks, you’ll be better equipped to grasp the more complex calculations and implications.

What is Interest? The Cost of Borrowing

At its core, interest is the charge for the privilege of borrowing money, typically expressed as a percentage of the principal amount. From the lender’s perspective, it’s the compensation for the risk taken by lending money, the opportunity cost of not using that money elsewhere, and a profit margin. From the borrower’s perspective, it’s the additional sum paid on top of the original amount borrowed. Think of it as a rental fee for money.

Key Terminology: Principal, Interest Rate, and Loan Term

To truly understand interest, you must first be familiar with three foundational terms:

- Principal: This is the initial amount of money borrowed. If you take out a $10,000 personal loan, $10,000 is your principal. All interest calculations begin with this base figure.

- Interest Rate: Expressed as a percentage, this is the cost of borrowing the principal for a specific period, usually annually. An interest rate of 5% means you’ll pay 5% of the principal (or the outstanding balance) in interest over the course of a year. It’s crucial to distinguish between the nominal interest rate and the Annual Percentage Rate (APR), which includes all fees and charges, giving a more accurate total cost of borrowing.

- Loan Term: This refers to the duration over which the loan is to be repaid. A 30-year mortgage has a loan term of 30 years, while a 5-year auto loan has a term of 5 years. The loan term significantly impacts both your monthly payment and the total amount of interest you’ll pay over the life of the loan. A longer term often means lower monthly payments but a higher total interest paid.

Why Lenders Charge Interest: More Than Just Profit

Lenders charge interest for several sound economic reasons beyond simply making a profit. Firstly, it compensates them for the risk that the borrower might default on the loan. Secondly, it covers the opportunity cost of the money they’ve lent – they could have invested that capital elsewhere to earn a return. Thirdly, it accounts for inflation, ensuring that the value of the money repaid in the future is comparable to the value of the money lent today. Lastly, it covers the administrative costs of originating and servicing the loan. Understanding these drivers helps contextualize why interest rates vary and why certain loans carry higher rates than others.

Delving into Different Types of Interest

While the core concept of interest remains consistent, the way it’s calculated can vary significantly, leading to vastly different total costs for the borrower. The two primary types of interest you’ll encounter are simple interest and compound interest. Furthermore, rates can be fixed or variable, each presenting its own set of advantages and risks.

Simple Interest: The Basics

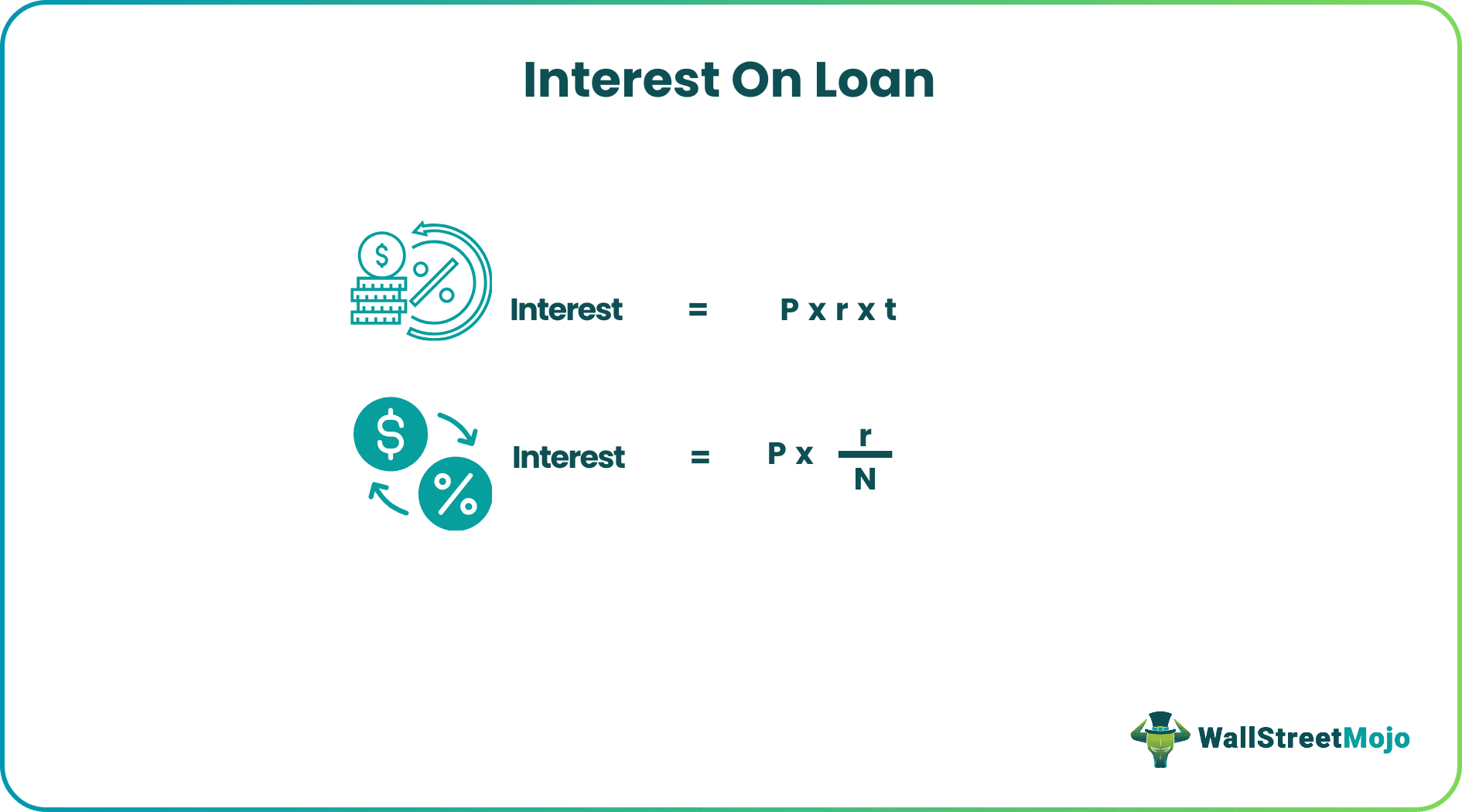

Simple interest is the most straightforward form of interest calculation. It is calculated only on the original principal amount of a loan or deposit. It does not take into account any interest that may have accrued in previous periods.

The formula for simple interest is:

Simple Interest = Principal (P) × Interest Rate (R) × Time (T)

- P: The principal amount.

- R: The annual interest rate (as a decimal).

- T: The loan term in years.

For example, if you borrow $1,000 at a simple interest rate of 5% per year for 3 years, the interest calculated each year is $1,000 × 0.05 = $50. Over 3 years, the total simple interest would be $50 × 3 = $150. Your total repayment would be $1,150. Simple interest is typically used for short-term loans, some personal loans, or specific types of bonds, but it’s less common for major consumer loans like mortgages or auto loans.

Compound Interest: The Power of Reinvestment

Compound interest is often referred to as “interest on interest.” Unlike simple interest, compound interest is calculated on the initial principal and also on all of the accumulated interest from previous periods. This means your interest balance grows not just on your original borrowing, but also on the interest that has already been added to your loan balance. This makes compound interest a powerful force, either for growth (in savings and investments) or for increasing debt (in loans).

The frequency of compounding significantly impacts the total interest paid. Interest can be compounded annually, semi-annually, quarterly, monthly, daily, or even continuously. The more frequently interest is compounded, the faster your debt grows. Most consumer loans, especially mortgages, auto loans, and credit cards, utilize compound interest.

While the full formula for compound interest can look complex, the core idea is that the interest due for each period is added to the principal, and the next period’s interest is calculated on this new, larger balance. This is why credit card debt can spiral quickly if only minimum payments are made.

Fixed vs. Variable Interest Rates

Beyond the calculation method, interest rates can also differ in their stability over the loan term:

- Fixed Interest Rate: As the name suggests, a fixed interest rate remains constant throughout the entire loan term. This provides predictability in your monthly payments, making budgeting easier and protecting you from potential rate increases. It’s common for traditional mortgages and auto loans. The downside is that you won’t benefit if market interest rates fall.

- Variable (Adjustable) Interest Rate: A variable interest rate fluctuates based on an underlying benchmark rate (like the prime rate or LIBOR, now often SOFR). This means your monthly payments can go up or down over the life of the loan. Variable rates might start lower than fixed rates, offering initial savings, but they come with the risk of increasing payments if market rates rise. Adjustable-Rate Mortgages (ARMs) are a common example.

Practical Methods for Calculating Loan Interest

Understanding the theory is one thing, but figuring out the actual numbers for your specific loan is where the rubber meets the road. While complex compound interest scenarios often require specialized tools, there are practical ways to estimate or calculate interest.

Manual Calculation for Simple Interest

For simple interest loans, the calculation is straightforward. Let’s say you take a short-term personal loan of $5,000 at a 6% annual simple interest rate for 2 years.

- P = $5,000

- R = 0.06 (6% as a decimal)

- T = 2 years

Interest = $5,000 × 0.06 × 2 = $600

Your total repayment would be $5,000 (principal) + $600 (interest) = $5,600. If you pay this back in 24 equal monthly installments, each payment would be $5,600 / 24 = $233.33.

Demystifying Compound Interest through Amortization

Most substantial loans (mortgages, auto loans, student loans) use compound interest with an amortization schedule. An amortization schedule is a table detailing each periodic loan payment, showing how much of the payment is applied to the interest versus the principal.

Here’s how it generally works for a level payment loan:

- Calculate the monthly interest: For each payment period, interest is calculated on the outstanding principal balance at the beginning of that period. If your annual rate is 6%, your monthly rate is 6% / 12 = 0.5% (or 0.005 as a decimal).

- Apply payment: Your fixed monthly payment is then applied. First, the calculated interest for that month is deducted.

- Reduce principal: The remaining portion of your monthly payment goes towards reducing the principal balance.

- New principal: The next month’s interest is then calculated on this new, lower principal balance.

In the early stages of an amortized loan, a larger portion of your payment goes towards interest because the principal balance is at its highest. As the principal is gradually paid down, a larger portion of subsequent payments goes towards the principal, and less towards interest. This is why paying extra principal early in a loan term can save you a significant amount in total interest over the life of the loan. While manual amortization is tedious, understanding this principle is crucial.

Leveraging Online Calculators and Spreadsheet Tools

For complex compound interest calculations, particularly those involving amortization, online loan calculators and spreadsheet software are indispensable.

- Online Loan Calculators: A quick search for “mortgage calculator,” “auto loan calculator,” or “personal loan interest calculator” will yield numerous free tools. You typically input the principal, interest rate, and loan term, and the calculator will instantly provide your estimated monthly payment, total interest paid, and often a full amortization schedule. These are invaluable for comparing different loan scenarios.

- Spreadsheet Software (Excel, Google Sheets): For those who prefer to build their own models or analyze various “what-if” scenarios, spreadsheet software is powerful.

- PMT function: The

PMT(rate, nper, pv)function calculates the payment for a loan based on constant payments and a constant interest rate.rate: The interest rate per period (e.g., annual rate / 12 for monthly).nper: The total number of payments (e.g., years * 12 for monthly).pv: The present value or principal of the loan.

- IPMT function: Calculates the interest portion of a given payment.

- PPMT function: Calculates the principal portion of a given payment.

- PMT function: The

These functions allow you to construct a custom amortization schedule, visualize the principal and interest breakdown over time, and even model the impact of extra payments.

Factors Influencing Your Interest Rate and Total Cost

The rate you ultimately qualify for and the total interest you pay aren’t arbitrary; they are the result of several interconnected factors. Understanding these influences can help you strategize for more favorable loan terms.

The Role of Your Credit Score

Your credit score is arguably the single most impactful factor in determining the interest rate you’ll be offered. Lenders use credit scores to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score (typically 700+) indicates a lower risk to the lender, resulting in access to lower interest rates. Conversely, a lower credit score signals higher risk, leading to higher interest rates to compensate the lender for that increased risk. Improving your credit score before applying for a loan can save you thousands over the life of the loan.

Loan Term and Its Impact

As briefly mentioned, the loan term (how long you have to repay the loan) significantly affects both your monthly payment and the total interest paid.

- Shorter Loan Term: Generally results in higher monthly payments but less total interest paid over the life of the loan. This is because the principal is paid off faster, giving less time for interest to accrue.

- Longer Loan Term: Leads to lower monthly payments, making the loan more affordable on a monthly basis. However, because you’re borrowing the money for a longer period, you end up paying substantially more in total interest.

For example, a 15-year mortgage will have higher monthly payments but a much lower total interest cost than a 30-year mortgage for the same principal amount and interest rate.

Loan Type and Collateral

The type of loan you seek also plays a critical role in its interest rate.

- Secured Loans: These loans are backed by an asset (collateral) that the lender can seize if you default. Examples include mortgages (secured by the house) and auto loans (secured by the car). Because the lender’s risk is lower, secured loans typically come with lower interest rates.

- Unsecured Loans: These loans are not backed by collateral, such as personal loans or credit cards. Lenders face a higher risk, so these loans generally carry higher interest rates.

Different loan products also have varying risk profiles and market demand, leading to differences in typical interest rates. Student loans, for instance, often have specific government-set rates or programs.

Economic Conditions and Lender Policies

Broader economic factors, such as the Federal Reserve’s target interest rate, inflation rates, and the overall health of the economy, influence the baseline interest rates lenders charge. When the Fed raises rates, borrowing generally becomes more expensive across the board. Furthermore, individual lenders have their own internal policies, risk assessment models, and competitive pricing strategies that contribute to the specific rate they offer you. Shopping around and comparing offers from multiple lenders is crucial.

Strategies for Managing Loan Interest and Reducing Costs

Understanding how interest is figured out is powerful, but applying that knowledge to actively manage and reduce your interest costs is where the real financial benefit lies. Here are several effective strategies.

Making Extra Payments and Understanding Prepayment Penalties

One of the most effective ways to reduce the total interest paid on a loan is to pay more than your scheduled minimum payment whenever possible. Even small extra payments, especially early in the loan term, can make a significant difference. When you make an extra payment, ensure that the additional amount is applied directly to the principal balance. This reduces the base on which future interest is calculated, accelerating the payoff process and saving you money.

However, be mindful of prepayment penalties. Some loans, particularly certain mortgages or business loans, may charge a fee if you pay off the loan early or make substantial additional principal payments. Always check your loan agreement for such clauses. Most standard consumer loans, like auto loans or personal loans, do not have prepayment penalties.

Refinancing for Lower Rates

Refinancing involves taking out a new loan to pay off an existing one, ideally at a lower interest rate or with more favorable terms. This can be a smart move if market interest rates have dropped since you originally took out your loan, or if your credit score has significantly improved. A lower interest rate means less of your monthly payment goes towards interest, allowing more to reduce the principal, or it can simply lower your monthly payments.

Refinancing, however, comes with its own costs, such as application fees, appraisal fees, and closing costs (for mortgages). You need to calculate if the savings from a lower interest rate outweigh these upfront expenses. It’s most beneficial when you can secure a significantly lower rate and plan to keep the loan for a substantial period.

Debt Consolidation and Its Nuances

Debt consolidation involves combining multiple debts, often high-interest ones like credit card balances, into a single new loan with a lower overall interest rate. Common consolidation methods include personal loans, balance transfer credit cards, or home equity loans. The primary benefit is simplifying your payments and potentially reducing the total interest paid.

While tempting, debt consolidation requires discipline. If you consolidate high-interest credit card debt, for example, but then continue to accumulate new debt on those same credit cards, you could end up in a worse financial position. Ensure that a consolidation loan actually offers a lower APR than your current debts and that you commit to not incurring new debt.

The Importance of Reading Loan Disclosures and APR

Always read the fine print of any loan agreement carefully. Pay close attention to the Annual Percentage Rate (APR), which represents the true annual cost of borrowing, including the interest rate and any associated fees (origination fees, discount points, etc.). The APR provides a more comprehensive picture of the loan’s total cost compared to just the nominal interest rate. Comparing APRs across different lenders gives you a clearer, apples-to-apples comparison.

Also, look for details on payment frequency, late payment penalties, grace periods, and any other clauses that could impact your financial obligations. Understanding these disclosures empowers you to ask informed questions and negotiate better terms.

Conclusion

Figuring out interest on a loan is not merely an academic exercise; it’s a critical skill for responsible financial management. From understanding the basics of principal and interest rates to discerning the profound differences between simple and compound interest, every piece of knowledge you gain empowers you to make smarter borrowing decisions. By leveraging practical tools like online calculators and spreadsheets, and by actively implementing strategies such as making extra payments or refinancing, you can significantly reduce the cost of borrowing and accelerate your path to financial freedom.

Don’t let the complexity deter you. Take the time to analyze your loan agreements, ask questions, and continuously educate yourself. The effort you put into understanding how interest is figured out will pay dividends, literally, by saving you money and giving you greater control over your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.