In the dynamic landscape of modern finance, digital payment platforms like Venmo have become indispensable tools for managing personal funds, simplifying transactions, and seamlessly integrating into our daily economic lives. More than just a casual app for splitting dinner bills, Venmo serves as a crucial component of a comprehensive personal finance strategy, enabling quick, secure, and trackable money movements. Understanding how to efficiently transfer money into your Venmo account is fundamental to leveraging its full potential as a financial tool, ensuring you have ready access to funds for payments, budgeting, and everyday expenditures. This guide will walk you through the various methods of funding your Venmo balance, emphasizing the financial implications and best practices to help you manage your money wisely within this popular platform.

Understanding Venmo as a Core Financial Tool

Venmo has transcended its initial reputation as a simple peer-to-peer payment application to become a robust digital wallet that plays a significant role in many individuals’ financial ecosystems. Its convenience, speed, and social features have made it a go-to platform for a myriad of financial interactions, from splitting utility bills with roommates to paying independent contractors for side hustle work. Approaching Venmo with a financial lens allows users to maximize its benefits while mitigating potential risks.

More Than Just Payments: Your Digital Wallet

At its heart, Venmo functions as a portable digital ledger for your liquid funds. It enables instant transactions that sidestep the traditional banking delays, making it ideal for immediate payments among friends, family, and even some businesses. The ability to carry a balance directly within the app means you can hold funds ready for use without needing to constantly pull from an external bank account, thus offering a layer of financial agility. This digital wallet functionality makes Venmo an integral part of how many people manage their day-to-day cash flow, particularly for social spending and routine shared expenses.

The Financial Benefits of Using Venmo

Beyond mere convenience, Venmo offers several tangible financial benefits. For personal finance, it excels in budgeting and expense splitting. By facilitating easy division of costs—whether for groceries, rent, or a group vacation—Venmo can help individuals track and settle shared financial obligations without complex calculations or awkward conversations. The platform also offers a rudimentary transaction history, which, when regularly reviewed, can provide insights into spending patterns, aiding in a more conscious approach to budgeting. Furthermore, the cashless nature of Venmo transactions can enhance personal security by reducing the need to carry large amounts of physical cash, thus minimizing the risk of theft or loss. Its speed also means faster settlement of debts, fostering healthier financial relationships.

Safeguarding Your Funds: A Financial Security Primer

While Venmo offers immense convenience, it’s imperative to approach it with a strong understanding of financial security. Protecting your funds starts with basic but crucial steps. Always link your Venmo account to a secure, primary bank account that you monitor regularly. Enable multi-factor authentication and use a strong, unique password for your Venmo account to prevent unauthorized access. Be vigilant against phishing attempts and scams, as these can compromise your financial information. Remember that Venmo, like any digital financial tool, requires active participation in its security features to ensure your money remains safe. Regular review of your transaction history also serves as an early warning system for any suspicious activity, allowing you to react quickly to protect your financial assets.

Navigating the Funding Options: Bringing Money Into Your Venmo Account

To use Venmo effectively for sending money or making purchases, you’ll need to fund your account. Venmo offers several flexible options for transferring money in, each with its own financial implications, convenience, and potential costs. Understanding these methods is key to choosing the most financially sound approach for your needs.

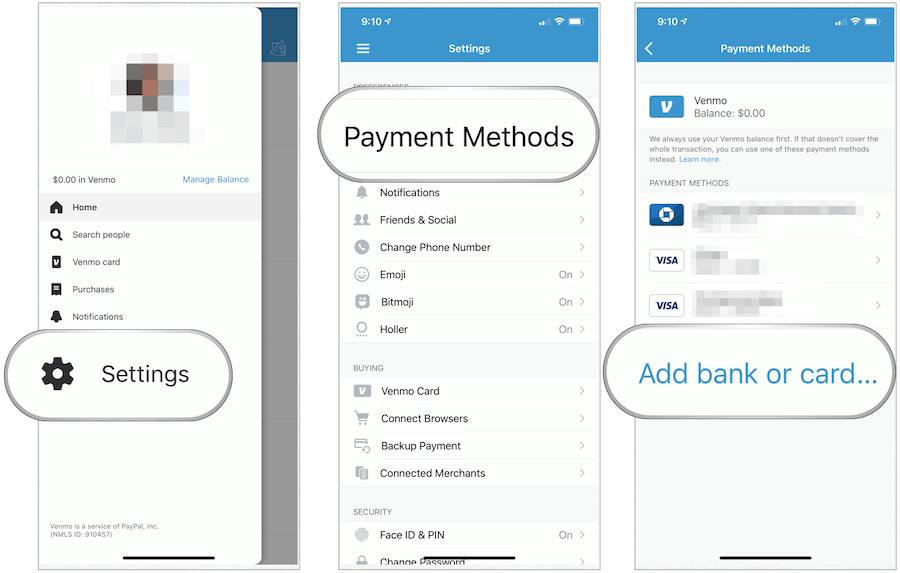

Linking Your Bank Account: The Primary Financial Conduit

The most common and financially prudent method for funding your Venmo account is by linking it directly to your checking or savings account. This process typically involves providing your bank’s routing and account numbers, which Venmo verifies through small, temporary deposits (micro-deposits) or instant bank verification through third-party services.

Once linked, your bank account serves as the default funding source for sending payments if your Venmo balance is insufficient, or for manually adding funds to your Venmo balance. This method is generally free of charge for standard transfers, making it the most cost-effective option for managing your Venmo funds. When you initiate a transfer from your bank account, you are authorizing Venmo to debit the specified amount directly from your bank, ensuring a secure and traceable financial transaction. It’s crucial to ensure your linked bank account has sufficient funds to cover any transfers, preventing overdraft fees from your bank and potential issues with Venmo.

Utilizing Debit and Credit Cards: Costs and Convenience

In addition to bank accounts, you can link debit and credit cards to your Venmo profile. These offer different levels of convenience and come with distinct financial considerations:

- Debit Card Transfers: Linking a debit card allows for quick transfers to your Venmo balance, much like a bank account transfer. This method is generally free of charge for standard transfers and provides an immediate way to fund your account using funds directly available in your bank account. It acts as a convenient intermediary, especially if you prefer not to share your bank account details directly with multiple platforms.

- Credit Card Transfers: While convenient, using a credit card to send money to friends or add funds to your Venmo balance typically incurs a 3% transaction fee. This fee is a significant financial consideration. From a personal finance perspective, using a credit card for peer-to-peer payments should be approached cautiously. While it offers immediate liquidity, the 3% fee can quickly add up, essentially making you pay for the privilege of transferring your own money. It’s generally advisable to use a credit card only when absolutely necessary (e.g., in an emergency where no other funding source is available) or if the benefits (like rewards points) outweigh the fee. For routine transactions, bank accounts or debit cards are financially superior options.

Many users link multiple cards to manage different spending categories or separate personal funds from business-related transactions, offering flexibility in how funds are drawn.

Receiving Funds from Others: A Passive Funding Stream

Beyond manually initiating transfers, your Venmo balance can also grow passively through payments you receive from other users. When someone sends you money via Venmo, those funds are automatically added to your Venmo balance. This is a common occurrence for splitting bills, getting paid for small gigs, or receiving reimbursements from friends.

These received funds instantly boost your available balance, which you can then use to pay others, make purchases via Venmo, or transfer out to your linked bank account. This seamless flow of incoming money makes Venmo an excellent tool for managing shared expenses and informal income, contributing to the platform’s role in your overall financial ecosystem.

Executing the Transfer: A Step-by-Step Financial Transaction Guide

Once you’ve linked your preferred funding sources, the process of transferring money into your Venmo account is straightforward. However, understanding each step and its financial implications is crucial for ensuring accuracy and managing your funds effectively.

Initiating a Manual Transfer from a Linked Account

To manually add funds to your Venmo balance from a linked bank account or debit card:

- Open the Venmo App: Launch the application on your mobile device.

- Navigate to the “You” Tab: This usually displays your current Venmo balance.

- Tap “Add Money”: This option will be clearly visible, often near your balance display.

- Enter the Amount: Carefully input the exact dollar amount you wish to transfer to your Venmo balance. Double-check this figure to avoid financial discrepancies.

- Select Funding Source: Choose the linked bank account or debit card from which you want to draw the funds. Remember the 3% fee if you were to use a credit card for sending money, although for adding money to your own balance from a linked card, debit cards are generally free.

- Confirm the Transfer: Review all details – the amount, the funding source, and any applicable fees. Once you’re certain everything is correct, confirm the transfer.

The funds will typically appear in your Venmo balance within 1-3 business days for standard transfers from a bank account, while debit card transfers can sometimes be faster. Venmo does not currently support adding money to your balance directly from a linked credit card.

Understanding Transfer Limits and Financial Planning

Venmo imposes certain financial limits on transactions, including how much money you can add to your balance, send, or withdraw within a given period. These limits are in place for security and regulatory compliance.

- Weekly Transfer Limits: New and unverified Venmo accounts typically have lower weekly limits for adding funds or sending money. These limits are usually in the hundreds of dollars.

- Verified Accounts: To increase your transaction limits significantly, Venmo requires users to verify their identity by providing information such as their date of birth, mailing address, and the last four digits of their Social Security number (KYC – Know Your Customer regulations). Verified accounts often have weekly limits reaching several thousands of dollars.

For effective financial planning, especially if you anticipate needing to transfer larger sums, it’s essential to understand and, if necessary, verify your Venmo account to increase these limits. This prevents unexpected delays or restrictions when you need to access or move your money. Always plan large transfers in advance, considering the standard processing times and your account’s current limits to maintain smooth cash flow.

Reviewing and Confirming Your Financial Commitment

The final step in any financial transaction, including transferring money to Venmo, is a thorough review and confirmation. Before tapping “Confirm,” take a moment to double-check:

- The Amount: Is the entered sum exactly what you intended to transfer? A misplaced decimal or incorrect digit can lead to significant financial inconvenience.

- The Funding Source: Are you drawing from the correct bank account or debit card? Confirming the source prevents accidental withdrawals from an account you might have designated for other purposes.

- Any Applicable Fees: While adding money from a bank account or debit card is typically free, being aware of any potential fees (like a credit card fee if you were sending directly, though not for adding to balance) ensures you understand the true cost of the transaction.

Mistakes in financial transfers can be difficult and time-consuming to rectify, potentially leading to financial loss or delays. A careful review process is your best defense against such errors, ensuring your money is transferred accurately and securely.

Maximizing Venmo for Your Personal Finance Ecosystem

Integrating Venmo strategically into your personal finance ecosystem extends beyond simply transferring money in. It involves understanding how its features can support your broader financial goals, from managing daily expenses to facilitating income streams.

Strategic Spending from Your Venmo Balance

Once funds are in your Venmo balance, you have several avenues for spending:

- Paying Friends and Family: This is Venmo’s primary use, perfect for splitting costs for social activities, group purchases, or personal reimbursements.

- Making Purchases: Many online and physical retailers now accept Venmo as a payment method, allowing you to use your balance directly for shopping.

- Venmo Debit Card/Credit Card: For even greater flexibility, Venmo offers a physical debit card (linked to your Venmo balance) and a credit card. The debit card allows you to spend your Venmo balance anywhere Mastercard is accepted, effectively turning your digital balance into spendable cash for everyday transactions. The Venmo Credit Card offers rewards and can be managed directly within the app, integrating credit spending into your Venmo financial view.

Strategically using your Venmo balance for certain categories of spending can simplify budgeting, especially for discretionary spending or social engagements.

Transferring Funds Out: Liquidity and Accessing Your Money

Just as important as getting money into Venmo is knowing how to get it out when you need to access your funds in your traditional bank account. Venmo offers two primary options:

- Standard Transfer: This option is typically free and takes 1-3 business days for the funds to arrive in your linked bank account. This is the most common and financially sound method for moving money from Venmo for bills or savings that aren’t time-sensitive.

- Instant Transfer: For a small fee (typically 1.75% of the transfer amount, with a minimum fee of $0.25 and a maximum fee of $25), you can transfer money to a linked debit card within minutes. This option provides immediate liquidity, making it ideal for urgent financial needs, but the fee should be weighed against the urgency. For most routine withdrawals, the standard free transfer is the better financial choice.

Understanding these options allows you to manage the liquidity of your Venmo balance, ensuring you can access your funds when and how you need them without incurring unnecessary costs.

Integrating Venmo with Broader Financial Goals

Venmo can be a powerful ally in your broader financial planning:

- Budgeting Apps: While Venmo has a basic transaction history, many users export their Venmo data or connect their Venmo account to more sophisticated budgeting applications (like Mint, YNAB, etc.). This integration provides a holistic view of your spending, incorporating your digital wallet transactions into your overall financial picture.

- Tracking Expenditures: For specific categories of spending (e.g., entertainment, dining out with friends), using Venmo consistently can help you track these expenditures more easily, aiding in adherence to budget limits.

- Small Business and Side Hustle Income: For freelancers, gig workers, or small business owners, Venmo can serve as an efficient way to receive payments from clients. While designed for personal use, its ease of use makes it a viable option for managing modest income streams, particularly when integrated with clear record-keeping for tax purposes. This requires careful financial management to distinguish personal funds from business revenue.

Common Financial Considerations and Best Practices with Venmo

To truly harness Venmo’s utility as a financial tool, it’s essential to be aware of common pitfalls and adopt best practices that safeguard your financial well-being.

Avoiding Overspending and Debt: Responsible Use of Credit Cards

As discussed, using a credit card to send money on Venmo incurs a 3% fee. Repeatedly doing so can lead to unnecessary expenses. More importantly, using a credit card to cover immediate expenses on Venmo can mask underlying financial issues, potentially leading to increased credit card debt if not managed carefully. Treat Venmo as a conduit for your existing funds, not an extension of your credit line, especially for peer-to-peer payments where the fee is applied. Prioritize funding via bank accounts or debit cards to avoid this extra cost and prevent credit card debt accumulation.

Protecting Your Financial Information and Transactions

Financial security on Venmo extends beyond just strong passwords. Always ensure you are sending money to the correct person by double-checking their username or phone number. Be cautious of requests for money from unknown individuals or unusual payment demands, as these are common tactics in financial scams. Venmo transactions are generally considered final, so exercising vigilance before confirming a payment is paramount to prevent irreversible financial loss. Regularly review your transaction history for any unauthorized activity and report suspicious behavior immediately.

Understanding Fees and Charges: The True Cost of Convenience

While Venmo is largely free for standard transactions, the fees for specific services can add up:

- Credit Card Fee: 3% for sending money.

- Instant Transfer Fee: 1.75% (min $0.25, max $25) for transferring money from Venmo to your debit card within minutes.

- Cryptocurrency Purchases: Venmo charges a fee for buying and selling cryptocurrency.

Being aware of these charges allows you to make informed financial decisions, choosing the most cost-effective options for your needs. For instance, planning ahead for transfers can help you avoid instant transfer fees, saving you money over time. Maximizing your funds means minimizing unnecessary expenses, and a clear understanding of Venmo’s fee structure is crucial for this.

Conclusion

Venmo stands as a powerful and convenient financial tool in the digital age, simplifying peer-to-peer payments and integrating seamlessly into everyday spending. By understanding how to efficiently transfer money to your Venmo account from linked bank accounts or debit cards, recognizing the financial implications of credit card use, and familiarizing yourself with transaction limits, you can leverage its full potential. However, like any financial instrument, Venmo demands responsible use, diligence in safeguarding your information, and an awareness of associated fees. By adopting these best practices, you can ensure Venmo not only serves as a convenient payment method but also as a supportive component of your overarching personal finance strategy, helping you manage your money wisely and achieve your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.