Tax season is often viewed with a sense of trepidation by many, yet it remains one of the most critical pillars of personal finance management. Understanding how to pay your taxes is not merely a matter of legal compliance; it is an essential skill for maintaining financial health, optimizing your cash flow, and ensuring long-term wealth preservation. Whether you are a traditional employee, a freelancer in the burgeoning gig economy, or a seasoned investor, the complexities of the tax code require a proactive and informed approach. This guide provides a detailed roadmap to navigating the tax landscape, from initial preparation to the final payment.

Understanding Your Tax Obligations and Filing Status

Before you can determine how much you owe or which forms to fill out, you must understand your specific standing within the tax system. Your filing status is the foundation upon which your entire tax return is built, affecting your tax rates and the size of your standard deduction.

Determining Your Filing Status

The IRS generally recognizes five filing statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Widow(er). Choosing the correct status is vital because it determines your tax brackets and eligibility for certain credits. For instance, the “Head of Household” status often provides more favorable tax rates and a higher standard deduction than filing as “Single,” provided you meet the criteria for maintaining a home for a qualifying person.

Identifying Taxable Income Sources

In the modern financial landscape, income often comes from diverse streams. Beyond the standard salary reported on a W-2, you must account for “unearned income” such as interest from savings accounts, dividends from stock investments, and capital gains from the sale of assets. Furthermore, the rise of side hustles means many individuals now receive 1099-NEC forms for independent contractor work. All these streams must be aggregated to determine your Adjusted Gross Income (AGI), which serves as the starting point for calculating your tax liability.

The Importance of the Tax Calendar

Missing a deadline can lead to unnecessary penalties and interest charges that eat into your savings. While April 15th is the most famous date on the financial calendar, it is not the only one. High-income earners and self-employed individuals often need to make quarterly estimated tax payments (typically in April, June, September, and January). Understanding these cycles ensures that you are not hit with an “underpayment penalty” at the end of the fiscal year.

Essential Documentation and Record-Keeping for Tax Preparation

A smooth tax filing process is rooted in meticulous organization. The difference between a stressful tax season and a seamless one often boils down to how well you tracked your financial activities throughout the year.

Gathering Income Statements (W-2s, 1099s, and K-1s)

By early February, you should have collected all relevant income documentation. For employees, this is the W-2. For freelancers and investors, this includes various 1099 forms (1099-INT for interest, 1099-DIV for dividends, 1099-B for brokerage sales). If you are a partner in a business or an investor in an S-corporation, you will also need a Schedule K-1. Ensuring you have every document before you begin filing prevents the need for filing an amended return later.

Tracking Deductions and Credits

Deductions lower your taxable income, while credits provide a dollar-for-dollar reduction of your actual tax bill. To claim these, you must have proof. This includes receipts for charitable donations, records of mortgage interest paid (Form 1098), student loan interest statements, and documentation for healthcare expenses if they exceed a certain percentage of your income. For business owners, keeping a detailed log of home office expenses, travel, and equipment purchases is non-negotiable for maximizing tax efficiency.

Digital Tools for Financial Organization

In the digital age, physical shoe-boxes of receipts are obsolete. Leveraging financial tools such as Quickbooks, Mint, or specialized receipt-scanning apps can automate the categorization of expenses. These tools allow you to generate year-end reports that can be directly imported into tax software, reducing human error and ensuring that no valid deduction is overlooked.

Step-by-Step Guide to Filing Your Tax Return

Once your documentation is in order, the next phase is the actual preparation of the return. This is where strategic decisions are made regarding how you present your finances to the government.

Choosing Between Standard Deduction and Itemizing

Every taxpayer is entitled to the standard deduction, which is a fixed dollar amount that reduces the income you’re taxed on. However, if your deductible expenses—such as state and local taxes (SALT), mortgage interest, and medical expenses—total more than the standard deduction, “itemizing” on Schedule A is the smarter financial move. As tax laws evolve, the threshold for itemizing changes, so it is important to run the numbers both ways to see which results in a lower tax liability.

Electronic Filing vs. Paper Filing

The IRS strongly encourages e-filing. Not only is it faster, with refunds typically processed within 21 days, but the software used for e-filing also performs real-time error checking. Paper filing is increasingly rare and carries a higher risk of manual entry errors and significant processing delays. For those with a simple financial profile and an income below a certain threshold, the IRS Free File program provides access to brand-name software at no cost.

Utilizing Professional Tax Software and Accountants

For individuals with complex portfolios—such as rental properties, foreign assets, or high-volume stock trading—DIY software might not be enough. In these cases, hiring a Certified Public Accountant (CPA) or an Enrolled Agent (EA) is an investment. A professional can provide nuanced advice on tax positions and represent you in the event of an audit, offering peace of mind that software alone cannot provide.

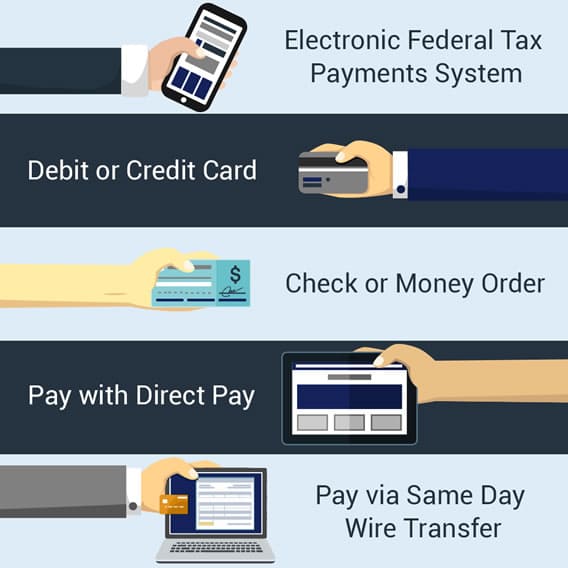

Methods and Platforms for Paying Your Tax Bill

Filing your return tells the government how much you owe; the final step is actually transferring those funds. The IRS and state tax agencies have modernized their systems to offer several payment avenues.

Direct Pay and Electronic Funds Withdrawal

The most straightforward way to pay is through “IRS Direct Pay.” This service allows you to pay your tax bill directly from your checking or savings account without any additional fees. You receive an immediate confirmation number, which serves as a vital record for your financial files. Similarly, if you file using software, you can schedule an Electronic Funds Withdrawal (EFW) to occur on a specific date, allowing you to keep your money in your high-yield savings account until the very last moment.

Credit or Debit Card Payments

While the IRS accepts credit and debit cards through third-party processors, this method requires careful consideration. These processors charge a convenience fee, often ranging from 1.8% to 2.5%. From a personal finance perspective, this is only advisable if you are trying to meet a minimum spend requirement for a significant credit card sign-up bonus or if the “cash back” rewards outweigh the processing fee. Otherwise, direct bank transfers remain the most cost-effective method.

Setting Up Installment Agreements and Payment Plans

If you find yourself in a position where you cannot pay your tax bill in full, the worst thing you can do is ignore the debt. The IRS offers “Installment Agreements” that allow you to pay your balance over time (up to 72 months in many cases). While interest and late-payment penalties still apply, setting up a formal plan prevents the IRS from taking more aggressive collection actions, such as wage garnishments or tax liens.

Strategic Financial Planning to Minimize Future Tax Liability

The most successful financial minds don’t just think about taxes in April; they think about them year-round. Tax planning is a proactive strategy to arrange your financial affairs in a way that minimizes the amount of tax you owe.

Maximizing Retirement Account Contributions

One of the most effective ways to lower your tax bill is to contribute to tax-advantaged retirement accounts. Contributions to a traditional 401(k) or a Traditional IRA are often “pre-tax,” meaning they reduce your taxable income for the year. For example, if you earn $70,000 and contribute $10,000 to a 401(k), you are only taxed as if you earned $60,000. This is an immediate “return” on your investment in the form of tax savings.

Tax-Loss Harvesting and Investment Strategies

In a taxable brokerage account, you can use “tax-loss harvesting” to your advantage. This involves selling investments that are at a loss to offset capital gains realized from other investments. If your losses exceed your gains, you can use up to $3,000 of the excess loss to offset your ordinary income, effectively turning a market downturn into a tax break.

Staying Informed on Changing Tax Laws

Tax legislation is rarely static. Provisions regarding child tax credits, energy-efficient home improvements, and corporate tax rates are frequently adjusted by Congress. Staying informed or maintaining a relationship with a financial advisor ensures that you can pivot your strategy in response to new laws. By viewing tax payment as a dynamic part of your broader financial strategy rather than a one-time annual chore, you empower yourself to build greater wealth and financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.