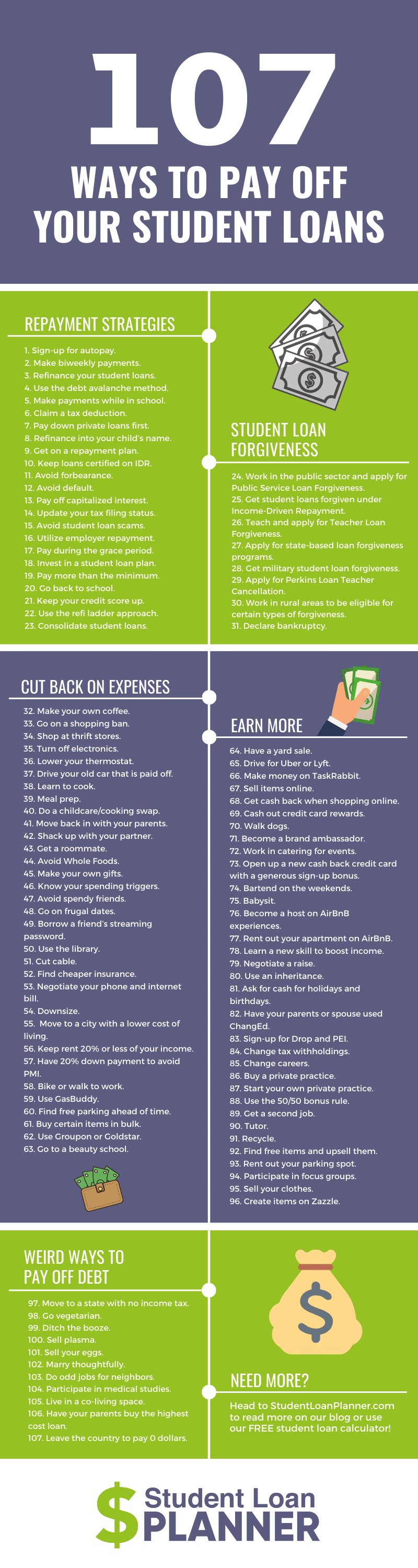

For millions of graduates, the transition from the classroom to the workforce is accompanied by a shadow: the student loan balance. With total national student debt hovering around $1.7 trillion, “how do I pay my student loans?” is more than a logistical question—it is a foundational challenge to one’s financial future. Navigating the complexities of federal versus private loans, interest rates, and repayment plans requires more than just a checkbook; it requires a comprehensive financial strategy.

Understanding your repayment options is the first step toward reclaiming your income and building long-term wealth. This guide breaks down the mechanics of student debt and offers actionable strategies to help you pay off your loans efficiently while maintaining your financial health.

1. Understanding the Landscape: Federal vs. Private Loans

Before you can build a repayment plan, you must identify exactly what kind of debt you are carrying. Not all student loans are created equal, and the rules governing them vary significantly based on the lender.

Federal Student Loan Repayment Plans

Federal loans, issued by the government, offer the most flexibility and protection. The default is the Standard Repayment Plan, which splits your balance into equal monthly payments over 10 years. While this is the fastest way to pay off the loan under normal federal terms, the monthly cost can be high for entry-level earners.

Beyond the standard plan, the government offers Income-Driven Repayment (IDR) plans, such as the SAVE (Saving on a Valuable Education) plan, PAYE (Pay As You Earn), and IBR (Income-Based Repayment). These plans cap your monthly payments at a percentage of your discretionary income (often 5% to 15%) and can lead to loan forgiveness after 20 or 25 years of consistent payments. These are vital tools for those whose debt-to-income ratio is high.

The Nuances of Private Loans

Private loans are issued by banks, credit unions, or online lenders. Unlike federal loans, they rarely offer income-based flexibility or forgiveness programs. The terms of a private loan are dictated by the contract you signed at the outset.

Paying off private loans usually requires a more aggressive approach because they often carry higher, variable interest rates. If you have private debt, your priority should be understanding your interest rate and looking for opportunities to lower it through refinancing, as private lenders do not provide the same “safety net” (like deferment or forbearance) that the Department of Education offers.

2. Strategic Repayment Methods: Speeding Up the Process

Once you know what you owe, the next step is determining the order in which you pay it. While making the minimum payment on all loans is a requirement to protect your credit score, “paying down” debt effectively requires a focused strategy.

The Debt Avalanche Method

The Debt Avalanche is the mathematically superior method for saving money. In this strategy, you list all your loans by interest rate. You make the minimum payments on every loan, but any extra capital you have—whether it’s $50 from a side hustle or a $500 tax refund—is directed toward the loan with the highest interest rate.

By killing off the most expensive debt first, you reduce the total amount of interest that accrues over the life of your loans. This shortens your repayment timeline and keeps more money in your pocket in the long run.

The Debt Snowball Method

If you struggle with motivation, the Debt Snowball might be the better fit. In this approach, you ignore the interest rates and focus on the smallest balance first. Once the smallest loan is paid off, you take the entire monthly payment you were sending to that loan and “roll” it into the next smallest balance.

The psychological win of seeing an account hit a zero balance can provide the momentum needed to stay disciplined over several years. While you may pay slightly more in interest than with the avalanche method, the consistency it builds is often the difference between finishing the journey and giving up.

Implementing Auto-Pay for Discounts

Most loan servicers (both federal and private) offer a 0.25% interest rate deduction if you sign up for automatic debit. While a quarter of a percentage point may seem negligible, on a $30,000 or $50,000 balance, it translates to hundreds of dollars saved over the life of the loan. Furthermore, it ensures you never miss a payment, protecting your credit score from the damage of late fees and reports of delinquency.

3. Leveraging Assistance and Forgiveness Programs

You do not always have to bear the full burden of your student debt alone. There are several institutional and governmental programs designed to incentivize certain career paths or provide relief to those in specific financial brackets.

Public Service Loan Forgiveness (PSLF)

The PSLF program is perhaps the most significant benefit for federal loan borrowers. If you work full-time for a government agency (at any level) or a 501(c)(3) non-profit organization, you may be eligible to have the remaining balance of your Direct Loans forgiven tax-free after making 120 qualifying monthly payments under an IDR plan.

To maximize this, it is crucial to certify your employment annually and ensure your loans are consolidated into the Direct Loan program if they aren’t already.

Employer Student Loan Contributions

In a competitive job market, more companies are offering student loan repayment assistance as a fringe benefit. Under current tax laws (specifically Section 127 of the Internal Revenue Code, which was extended through 2025), employers can provide up to $5,250 per year in tax-free student loan repayment assistance to their employees.

When searching for a new job or negotiating a raise, inquire about this benefit. It is essentially “free money” that goes directly toward your principal, drastically reducing the time you spend in debt.

4. Refinancing and Consolidation: When to Pivot

Refinancing is the process of taking out a new loan with a private lender to pay off your existing loans. This is a powerful tool, but it is not a one-size-fits-all solution.

When to Refinance

Refinancing makes sense if you have a strong credit score (typically 700+), a stable income, and high-interest private loans. By refinancing into a lower interest rate, you reduce your monthly payment and the total cost of the loan. For example, dropping an interest rate from 8% to 5% on a $40,000 loan can save thousands of dollars.

The Risks of Consolidating Federal Loans into Private

The most important rule of student loan management is this: Never refinance federal loans into private loans unless you are certain you don’t need federal protections.

Once you refinance a federal loan with a private bank, you permanently lose access to IDR plans, PSLF, and federal discharge options in cases of total disability. If you have a high-paying, stable career in the private sector and do not qualify for forgiveness, refinancing federal loans to a lower private rate might be a smart financial move. However, for most, keeping federal loans within the federal system provides a necessary safety net.

5. Building a Sustainable Financial Future

Paying off student loans is a marathon, not a sprint. To avoid burnout and financial strain, you must integrate your debt repayment into a broader financial life.

Budgeting for Debt and Life

The most common mistake graduates make is living a “lifestyle” that their debt-to-income ratio cannot support. Use the 50/30/20 rule as a baseline: 50% of your income goes to needs (rent, groceries), 30% to wants, and 20% to financial goals (savings and debt repayment). If your student loan payments are eating up 40% of your income, you must find ways to reduce your “wants” or “needs” to ensure you are still contributing to an emergency fund.

Paying off debt while having zero savings is dangerous; one car repair or medical bill could force you to put expenses on a high-interest credit card, negating the progress you’ve made on your student loans.

Avoiding Common Repayment Pitfalls

- Ignoring Interest Accrual: If you are in a deferment or forbearance period where interest is still accruing (unsubsidized loans), try to at least pay the interest monthly. This prevents “capitalization,” where the accrued interest is added to your principal balance, causing you to pay interest on your interest.

- The “Lump Sum” Trap: While it’s tempting to throw every extra penny at your debt, ensure you are still contributing to your employer-sponsored 401(k), especially if there is a match. The 100% return of an employer match is almost always better than the 5-7% interest savings from a student loan payment.

- Losing Contact with Servicers: If you move or change your email, update your loan servicer immediately. Missing a notice about a change in your repayment terms or a missed payment can lead to default, which ruins your credit and can lead to wage garnishment.

Conclusion

Paying your student loans is not just about writing a check every month; it is about taking control of your financial narrative. By identifying your loan types, choosing a strategic repayment method like the Avalanche or Snowball, and staying informed about forgiveness and refinancing opportunities, you can turn a daunting debt into a manageable part of your financial plan. Debt is a tool that helped you earn your degree; now, use the tools of personal finance to ensure that debt doesn’t stand in the way of your next great achievement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.