Securing a loan is one of the most significant financial milestones an individual or business owner can undertake. Whether you are looking to consolidate high-interest debt, fund a major home renovation, or launch a new entrepreneurial venture, the process of obtaining capital requires more than just a simple application. It demands a strategic approach to personal finance, a deep understanding of lending criteria, and an analytical eye for the terms and conditions that will govern your financial life for years to come.

In the modern financial ecosystem, the “how” of getting a loan has evolved. It is no longer just about walking into a local bank branch; it involves navigating a digital landscape of traditional institutions, credit unions, and fintech disruptors. This guide provides a professional and comprehensive roadmap to understanding the lending process, optimizing your financial profile, and securing the best possible terms for your specific needs.

1. Evaluating Your Financial Health Before Applying

Before you approach a lender, you must view your finances through their eyes. Lenders are fundamentally in the business of risk management. Their primary goal is to determine the probability that you will repay the borrowed capital plus interest. By assessing your financial health beforehand, you can identify potential red flags and address them to improve your approval odds.

The Power of the Credit Score

Your credit score is arguably the most influential factor in the loan approval process. Most lenders rely on FICO scores, which range from 300 to 850. A higher score signals to the lender that you have a history of responsible credit management.

To prepare for a loan, you should pull your credit reports from the three major bureaus—Equifax, Experian, and TransUnion. Look for errors or fraudulent activity that could be dragging your score down. Even a 20-point difference in your score can move you from a “prime” to a “subprime” category, potentially costing you thousands of dollars in additional interest over the life of the loan.

Debt-to-Income Ratio (DTI)

While your credit score shows how you manage debt, your Debt-to-Income (DTI) ratio shows how much debt you can realistically afford to take on. Lenders calculate this by dividing your total monthly debt payments by your gross monthly income.

Generally, a DTI of 36% or lower is considered healthy, although some mortgage lenders may allow up to 43% or higher depending on the loan type. If your DTI is too high, it signals to the lender that your cash flow is overextended, making you a higher risk for default. Reducing existing credit card balances or increasing your documented income can help lower this ratio.

Proof of Income and Employment Stability

Lenders want to see a consistent and predictable income stream. For W-2 employees, this usually means providing recent pay stubs and W-2 forms from the last two years. For the self-employed or those with “side hustle” income, the documentation requirements are more stringent, often requiring two years of comprehensive federal tax returns and profit-and-loss statements. Stability matters; lenders prefer seeing at least two years of consistent employment within the same industry.

2. Navigating Different Types of Loans

Not all loans are created equal. The structure, interest rate, and repayment terms vary significantly depending on the purpose of the funds and the collateral involved. Selecting the right financial instrument is crucial for long-term fiscal health.

Personal Loans: Secured vs. Unsecured

Personal loans are versatile and can be used for almost any purpose. They are typically “unsecured,” meaning they are not backed by collateral like a house or car. Because they are higher risk for the lender, interest rates are usually higher than those for secured loans. However, if you have significant savings or a vehicle you own outright, you might opt for a “secured” personal loan to lower your interest rate, though you risk losing the asset if you default.

Mortgages and Home Equity Products

For those looking to enter the real estate market or leverage the value of their current home, mortgages and Home Equity Lines of Credit (HELOCs) are the standard tools. These are long-term commitments often spanning 15 to 30 years. Because the loan is secured by real estate, interest rates are typically lower than personal loans. However, the application process is significantly more rigorous, involving appraisals, title searches, and extensive underwriting.

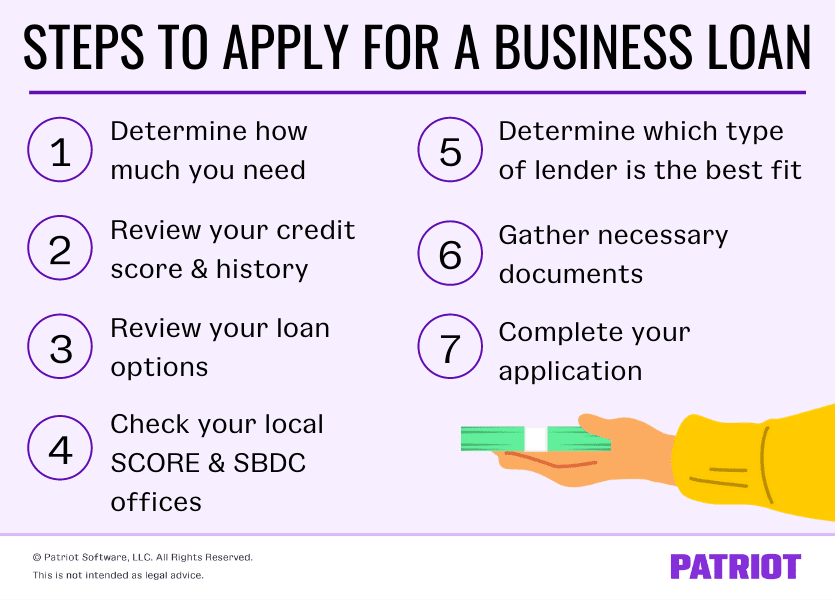

Business and Small Business Administration (SBA) Loans

If the goal is to fund a business, personal loans are often insufficient. Business loans focus on the health of the company, including its revenue, cash flow, and business credit score. SBA loans are a popular option because they are partially guaranteed by the government, allowing lenders to offer more favorable terms to small business owners who might not qualify for traditional commercial financing.

3. The Strategic Loan Application Process

Once you have assessed your health and chosen your loan type, the application phase begins. This stage requires organizational precision and a proactive approach to communication with the lender.

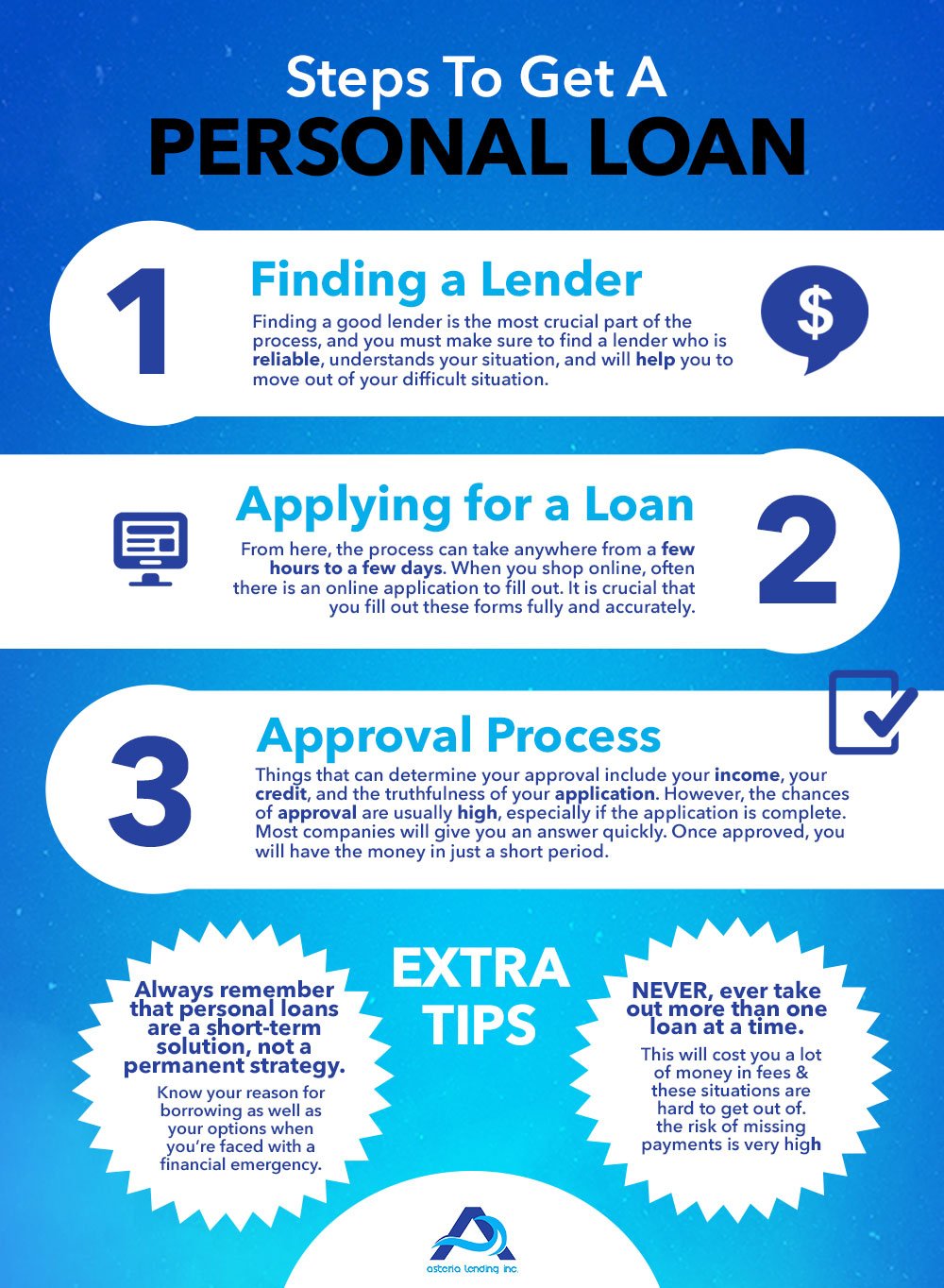

Shopping Around and Pre-Qualification

Never accept the first offer you receive. Different lenders have different “risk appetites.” A traditional bank might reject an application that a fintech lender would gladly accept, albeit at a slightly higher rate.

Utilize “pre-qualification” tools whenever possible. Pre-qualification usually involves a “soft” credit pull, which does not impact your credit score, allowing you to compare estimated rates and terms across multiple lenders. Once you find the most competitive offer, you proceed to the formal application, which triggers a “hard” credit pull.

Gathering Essential Documentation

Delays in loan approval often stem from missing documentation. To expedite the process, create a digital folder containing:

- Government-issued ID (Passport or Driver’s License).

- Social Security Number.

- The last two months of bank statements (all pages).

- Recent tax returns and W-2s/1099s.

- A list of current debts and monthly obligations.

- Documentation regarding the purpose of the loan (e.g., a purchase agreement or contractor estimates).

Submitting the Application and Underwriting

After submission, the loan enters “underwriting.” This is the phase where a professional underwriter (or an automated algorithm) verifies all your information. During this time, the lender may ask for “letters of explanation” regarding specific transactions on your bank statements or gaps in employment. It is vital to respond to these requests immediately; a delay in response can lead to the expiration of your locked-in interest rate.

4. Strategies to Increase Your Approval Odds

If your financial profile isn’t perfect, there are proactive steps you can take to move the needle in your favor. Strategic positioning can often make the difference between a rejection and an approval.

Correcting Credit Report Errors

Statistically, a significant percentage of credit reports contain errors. These can range from accounts that don’t belong to you to outdated “late payment” statuses that should have aged off. By disputing these errors through the credit bureau’s online portals, you can often see a rapid improvement in your score within 30 to 45 days.

Strategic Debt Reduction

If your DTI is the primary hurdle, consider the “snowball” or “avalanche” methods to pay down revolving debt quickly. Reducing your credit card utilization (the amount of credit you use vs. your total limit) to under 10% can provide a significant, immediate boost to your credit score, making you a much more attractive candidate for a loan.

Utilizing a Co-signer or Collateral

If you are a first-time borrower or have a damaged credit history, you may need a co-signer. A co-signer is someone with strong credit who agrees to take responsibility for the loan if you fail to pay. This reduces the lender’s risk significantly. Alternatively, offering collateral—such as a certificate of deposit (CD) or a paid-off vehicle—can transform a high-risk application into a secured, low-risk one.

5. Managing Your Loan for Long-Term Financial Health

Getting the loan is only the beginning. The way you manage the debt once the funds are in your account will dictate your financial flexibility for years to come.

Understanding the Amortization Schedule

Most loans are “amortized,” meaning your monthly payments are split between paying off interest and paying down the principal balance. In the early years of a loan, a larger portion of your payment goes toward interest. Understanding this schedule allows you to see the benefit of making extra principal-only payments, which can drastically reduce the total interest paid over the life of the loan.

Avoiding Predatory Lending Pitfalls

Be wary of “payday loans” or “no-credit-check” loans. These products often carry Annual Percentage Rates (APRs) exceeding 300%, creating a cycle of debt that is nearly impossible to escape. Always look at the APR, not just the monthly payment. The APR reflects the true cost of the loan, including interest and fees, providing a transparent metric for comparison.

Planning for Early Repayment

Before signing the final loan agreement, check for “prepayment penalties.” Some lenders charge a fee if you pay the loan off early, as they lose out on the expected interest. Ideally, you want a loan that allows you to pay it off as quickly as your cash flow permits, saving you money in the long run and freeing up your DTI for future financial opportunities.

In conclusion, getting a loan is a process of preparation, comparison, and execution. By focusing on your credit health, choosing the right financial product, and maintaining a disciplined approach to documentation and repayment, you can turn a loan into a powerful tool for wealth creation and financial stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.