The burden of student loan debt can feel immense, a financial shadow stretching far beyond graduation. For many, the question of “how can I pay back my student loans?” isn’t just a query but a pressing financial priority. Navigating the complex landscape of repayment options, interest rates, and loan servicers requires a strategic approach, blending an understanding of your specific loan types with a clear picture of your personal financial situation. This comprehensive guide will equip you with the knowledge and strategies to not only manage your student loans but to conquer them, paving the way for greater financial freedom.

Understanding Your Student Loan Landscape

Before you can effectively tackle your student loans, you need a firm grasp of what kind of debt you actually have. Not all student loans are created equal, and their differences significantly impact your repayment options.

Differentiating Federal vs. Private Loans

The most crucial distinction to make is between federal and private student loans. This isn’t merely a bureaucratic difference; it dictates the flexibility, relief options, and interest rates you can expect.

- Federal Student Loans: These are issued by the U.S. Department of Education and come with a host of borrower protections and flexible repayment plans, including income-driven options, deferment, forbearance, and potential for loan forgiveness. Examples include Direct Subsidized Loans, Direct Unsubsidized Loans, PLUS Loans, and Perkins Loans (though new Perkins Loans are no longer being disbursed). They typically have fixed interest rates.

- Private Student Loans: These are offered by banks, credit unions, and other private lenders. They generally offer fewer borrower protections, less flexible repayment options, and interest rates that can be fixed or variable, often depending on your creditworthiness (or your co-signer’s). They are typically more difficult to modify or forgive.

Knowing which type you have is the first step in formulating your repayment strategy. You can typically find this information by logging into your account on the National Student Loan Data System (for federal loans) or by checking statements from your private lenders.

Key Loan Terms: Interest Rates, Loan Servicers, and Repayment Dates

Once you’ve identified your loan types, delve into the specifics:

- Interest Rates: This is the cost of borrowing money, expressed as a percentage. A higher interest rate means you pay more over the life of the loan. Understanding if your rate is fixed (stays the same) or variable (can change) is vital for long-term planning.

- Loan Servicers: These are the companies that handle the billing and other services for your student loan. They are your primary point of contact for questions, payments, and repayment plan changes. Common federal loan servicers include Nelnet, Aidvantage, MOHELA, and Edfinancial. For private loans, your servicer will be the bank or company you borrowed from. Keep their contact information handy.

- Repayment Dates: Your loan servicer will provide a clear repayment schedule, including your monthly payment amount and due date. Missing these dates can lead to late fees and damage your credit score.

Assessing Your Financial Situation

Before you commit to a repayment strategy, take an honest look at your personal finances. Create a detailed budget that includes all your income and expenses. Understand your disposable income – the money left after essential expenses – as this will inform how aggressively you can tackle your debt. This assessment is critical for choosing a plan that is sustainable and realistic for your current circumstances.

Exploring Federal Student Loan Repayment Options

Federal student loans offer a suite of repayment plans designed to accommodate various financial situations. Understanding these options is key to choosing the best path for you.

Standard Repayment Plan

This is the default plan for most federal loans. Payments are fixed and spread out over 10 years (or up to 30 years for consolidated loans). It typically results in the lowest total interest paid because you pay off the loan quickly, but the monthly payments can be higher.

Graduated Repayment Plan

Under this plan, payments start lower and gradually increase every two years, usually over a 10-year period. This can be helpful if your income is expected to rise over time, but you’ll pay more interest overall than with the Standard plan.

Extended Repayment Plan

If you have more than $30,000 in federal student loans, you may be eligible for an extended repayment plan, allowing you to stretch payments over 25 years. This lowers your monthly payment but significantly increases the total interest paid over the life of the loan. Payments can be fixed or graduated.

Income-Driven Repayment (IDR) Plans

IDR plans are a lifeline for borrowers struggling with high monthly payments relative to their income. They cap your monthly payment at an affordable percentage of your discretionary income, typically 10-20%, and extend the repayment period to 20 or 25 years. Any remaining balance after the repayment period may be forgiven, though it might be considered taxable income. Common IDR plans include:

- REPAYE (Revised Pay As You Earn): Generally caps payments at 10% of discretionary income.

- PAYE (Pay As You Earn): Also caps payments at 10% of discretionary income, but has stricter eligibility requirements.

- IBR (Income-Based Repayment): Caps payments at 10% or 15% of discretionary income, depending on when you took out your loans.

- ICR (Income-Contingent Repayment): Caps payments at 20% of discretionary income or what you would pay on a fixed 12-year plan, whichever is less.

IDR plans are particularly beneficial if your income is low or unstable, as payments adjust annually based on your updated income and family size.

Forbearance and Deferment: When to Use Them

These are temporary options to postpone your loan payments.

- Deferment: Allows you to postpone payments due to specific circumstances like unemployment, economic hardship, or military service. Interest may not accrue on subsidized loans during deferment.

- Forbearance: Allows you to temporarily stop or reduce payments for up to 12 months at a time, but interest always accrues on all loan types during forbearance.

Both should be considered short-term solutions, as interest can add up, increasing your total debt. They are best used in genuine financial emergencies after exhausting other options.

Public Service Loan Forgiveness (PSLF) and Other Forgiveness Programs

If you work for a government agency or a qualifying non-profit organization, the Public Service Loan Forgiveness (PSLF) program might be for you. After making 120 qualifying monthly payments while working full-time for a qualifying employer, the remaining balance on your Direct Loans may be forgiven tax-free.

Beyond PSLF, there are other targeted federal loan forgiveness, cancellation, and discharge programs for teachers, healthcare professionals, borrowers with total and permanent disability, or those whose schools closed. Research these carefully if you believe you might qualify.

Strategies for Managing Private Student Loans

Private student loans offer fewer protections than federal loans, making their management more challenging but not impossible.

Contacting Your Lender

If you’re struggling to make payments on private loans, your first step should always be to contact your loan servicer. While they aren’t obligated to offer the same relief as federal loans, some lenders may have hardship programs, temporary payment reductions, or deferment options they can extend. Don’t wait until you’re delinquent; proactive communication is key.

Refinancing Private Student Loans

Refinancing involves taking out a new loan, typically with a lower interest rate, to pay off your existing private student loans. This can significantly reduce your monthly payment and the total interest you pay over time. To qualify, you generally need a good credit score, a stable income, and a low debt-to-income ratio. You might also need a co-signer. Be aware that refinancing federal loans into a private loan means forfeiting all federal benefits and protections, a decision that should not be taken lightly.

Exploring Co-signer Release Options

If you have a co-signer on your private student loan, explore whether your lender offers a co-signer release option. This allows your co-signer to be removed from the loan after you meet specific eligibility criteria, such as a certain number of on-time payments and demonstrating financial stability. This can be a great relief for your co-signer and a step toward greater financial independence for you.

Proactive Strategies to Accelerate Repayment and Save Money

Beyond choosing the right repayment plan, several proactive steps can help you pay off your loans faster and save thousands in interest.

Making Extra Payments and Applying Them to Principal

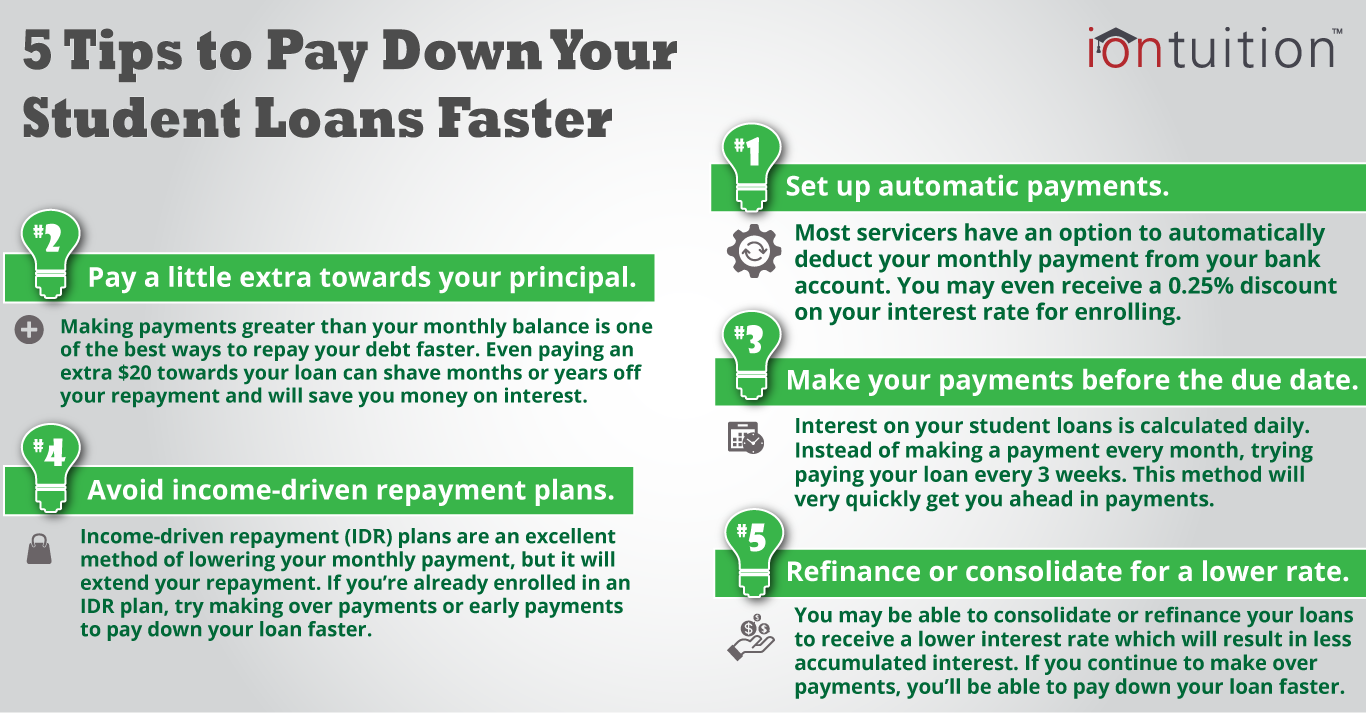

Even small extra payments can make a big difference. When you send in more than your minimum due, instruct your loan servicer to apply the additional amount directly to the loan’s principal balance. This reduces the amount of money interest is calculated on, leading to significant savings over time. Consider rounding up your payment, making bi-weekly payments (which results in one extra full payment per year), or putting windfalls like tax refunds or bonuses towards your loans.

The Debt Avalanche vs. Debt Snowball Method

These popular debt repayment strategies can be applied to student loans:

- Debt Avalanche: Focus on paying off the loan with the highest interest rate first, while making minimum payments on all other loans. Once the highest-interest loan is paid off, you roll that payment amount into the next highest-interest loan. This method saves you the most money on interest.

- Debt Snowball: Focus on paying off the smallest loan balance first, while making minimum payments on all other loans. Once the smallest loan is paid off, you roll that payment amount into the next smallest loan. This method prioritizes psychological wins, keeping you motivated by showing quick progress.

Choose the method that best aligns with your financial personality and motivation.

Automating Payments for Interest Rate Reductions

Many loan servicers offer a small interest rate reduction (e.g., 0.25%) if you sign up for automatic debit payments. This seemingly minor discount can add up over years, and it ensures you never miss a payment, protecting your credit score.

Budgeting and Finding Additional Income

A strict budget is your best friend in debt repayment. Identify areas where you can cut expenses and redirect those savings towards your loans. Consider taking on a side hustle, selling unused items, or negotiating a raise to boost your income and accelerate your repayment timeline. Every extra dollar you put towards your principal is a dollar that won’t accrue interest.

Avoiding Common Pitfalls

- Ignoring your loans: Pretending your loans don’t exist will only lead to greater problems, including default and damaged credit.

- Not understanding your loans: Failing to grasp the difference between federal and private, or your specific repayment terms, can lead to poor decisions.

- Missing payments: Late payments incur fees and negatively impact your credit score.

- Not updating contact information: Ensure your loan servicer always has your current address and phone number.

Navigating Challenges and Seeking Professional Help

Despite your best efforts, financial difficulties can arise. Knowing how to react and when to seek help is paramount.

What to Do If You Can’t Afford Payments

If you find yourself unable to make your monthly payments, do not panic and do not ignore the problem. Immediately contact your loan servicer. For federal loans, they can help you explore income-driven repayment plans, deferment, or forbearance. For private loans, inquire about any hardship programs they might offer. The goal is to avoid default at all costs.

Understanding Default and Its Consequences

Defaulting on your student loans carries severe consequences. For federal loans, this can mean wage garnishment, seizure of tax refunds, loss of eligibility for future federal student aid, and a ruined credit score. For private loans, lenders can pursue lawsuits, collections, and report the default to credit bureaus. Defaulting can haunt your financial life for years.

When to Consult a Financial Advisor or Credit Counselor

If your student loan situation feels overwhelming, or you’re unsure which path to take, consider seeking professional guidance. A certified financial planner can help you integrate your loan repayment into your broader financial goals. A non-profit credit counseling agency can provide unbiased advice on debt management, budgeting, and dealing with creditors. Be wary of companies that charge high upfront fees for services you could get for free or at a low cost from your loan servicer or non-profit organizations.

Paying back student loans is a marathon, not a sprint. It requires patience, discipline, and a clear strategy. By understanding your loan types, exploring all available repayment options, and adopting proactive financial habits, you can take control of your student loan debt and work steadily towards a future free from this financial obligation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.