Navigating the complexities of tax season can be daunting, but fulfilling your payment obligations to the Internal Revenue Service (IRS) is a fundamental aspect of financial responsibility. Whether you’re an individual taxpayer, a self-employed professional, or a small business owner, understanding the various methods available to remit your taxes is crucial for ensuring compliance, avoiding penalties, and maintaining peace of mind. This comprehensive guide will demystify the IRS payment process, outlining the most common and secure ways to make your payments, along with essential tips for a smooth and error-free experience.

Understanding Your IRS Payment Obligations and Deadlines

Before diving into payment methods, it’s vital to grasp why and when you might need to make a payment to the IRS. These obligations extend beyond the annual tax filing deadline, encompassing a range of scenarios that require proactive financial planning.

Common Scenarios Requiring IRS Payments

The need to make a payment to the IRS can arise from several situations, each with its own set of rules and implications:

- Annual Tax Due: This is the most common scenario, occurring when the tax calculated on your filed return (e.g., Form 1040, Form 1120) exceeds the total amount withheld from your paychecks or paid through estimated taxes during the year. This balance must be paid by the tax deadline to avoid penalties.

- Estimated Taxes: Individuals who are self-employed, own a business, or have significant income not subject to withholding (e.g., investment income, rental income, alimony) are often required to pay estimated taxes quarterly. This ensures you pay income tax and self-employment tax as you earn or receive income throughout the year, rather than a lump sum at tax time. Failure to pay sufficient estimated taxes can result in underpayment penalties.

- Extension Payments: If you file for an extension to submit your tax return (typically Form 4868 for individuals), remember that an extension to file is not an extension to pay. Any tax you owe is still due by the original deadline, usually April 15th. You should estimate your tax liability and pay that amount when you file your extension to avoid interest and penalties.

- Installment Agreements or Offers in Compromise (OIC): If you owe taxes but cannot pay them in full, the IRS may allow you to enter into an installment agreement to make monthly payments, or in some cases, an Offer in Compromise (OIC) where you pay a lower amount than what you owe. Payments under these agreements follow a specific schedule.

- Penalties and Interest: In instances of late filing, late payment, underpayment of estimated tax, or other compliance issues, the IRS may assess penalties and interest. These amounts must also be paid to resolve your tax liability.

Key Deadlines and Consequences of Non-Compliance

Adhering to IRS deadlines is paramount to avoiding costly penalties and interest. The most significant deadline for most individual taxpayers is April 15th (or the next business day if it falls on a weekend or holiday) for filing and paying taxes for the prior year. For those paying estimated taxes, the year is divided into four payment periods with specific due dates:

- Period 1 (Jan 1 to Mar 31): Due April 15

- Period 2 (Apr 1 to May 31): Due June 15

- Period 3 (Jun 1 to Aug 31): Due September 15

- Period 4 (Sep 1 to Dec 31): Due January 15 of the following year

Failure to meet these deadlines or pay the correct amount can trigger penalties, including:

- Failure-to-Pay Penalty: This penalty is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, capped at 25% of your unpaid tax.

- Failure-to-File Penalty: If you don’t file on time, the penalty is 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid tax. This can be significantly higher than the failure-to-pay penalty.

- Underpayment of Estimated Tax Penalty: Applies if you don’t pay enough tax throughout the year through withholding or estimated tax payments.

- Interest: Interest is charged on underpayments and applies to any unpaid tax from the due date of the return until the date of payment. Interest rates are set quarterly by the IRS.

Understanding these obligations and deadlines forms the foundation for effectively managing your tax payments.

Electronic and Digital Payment Methods: Convenience and Speed

In the digital age, the IRS has significantly expanded its electronic payment options, offering taxpayers convenient, secure, and often free ways to remit their taxes. These methods are generally preferred for their speed, accuracy, and instant confirmation.

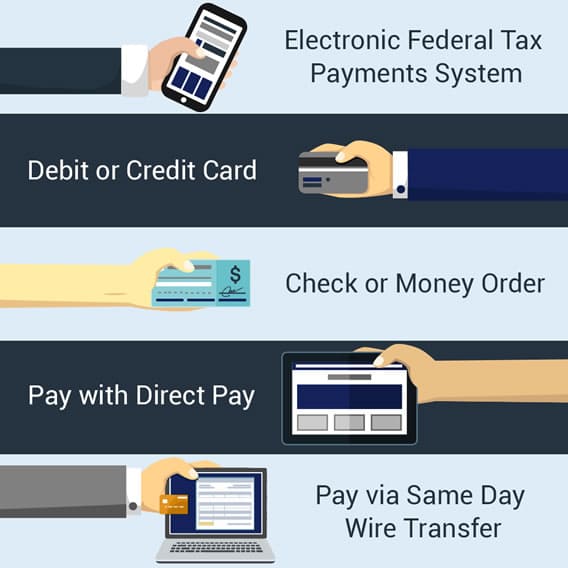

1. IRS Direct Pay: Your Free Bank Account Option

IRS Direct Pay is a secure web-based service offered directly by the IRS, allowing you to pay your taxes directly from your checking or savings account for free.

- How it Works:

- Visit the IRS Direct Pay page on IRS.gov.

- Select the reason for your payment (e.g., income tax, estimated tax).

- Choose the tax year you’re paying for.

- Enter your bank account information (routing and account numbers).

- You’ll receive an immediate confirmation number via email if you provide your email address.

- Advantages: It’s completely free, secure, and provides immediate confirmation. You can schedule payments up to 30 days in advance.

- Best For: Most individual taxpayers, especially those who prefer to pay directly from their bank without incurring fees.

2. Debit Card, Credit Card, or Digital Wallet: Flexibility with Fees

For those who prefer the flexibility of cards or digital wallets, the IRS partners with third-party payment processors to facilitate these transactions. While convenient, these options typically involve a processing fee.

- How it Works:

- Access the IRS’s approved payment processors list on IRS.gov.

- Choose a processor (e.g., ACI Payments, Inc., PayUSAtax, Official Payments).

- Follow the processor’s instructions to enter your payment details, tax information, and card/digital wallet information.

- You will pay a processing fee, which varies by processor and payment method.

- Associated Fees: Fees are a percentage for credit card payments (usually 1.96% to 2.29%) and a lower flat fee for debit card payments (typically $2.20 to $3.95). Digital wallet fees (e.g., PayPal, Click to Pay) may also apply.

- Advantages: Offers flexibility, allows you to earn credit card rewards (if applicable), and can help manage cash flow. Payments are posted quickly.

- Best For: Taxpayers who prioritize convenience, want to earn rewards, or need to bridge a temporary cash flow gap (though interest on credit card debt can negate tax savings).

3. Electronic Federal Tax Payment System (EFTPS): For Businesses and Regular Payers

EFTPS is a free service provided by the U.S. Department of the Treasury that allows individuals and businesses to make all federal tax payments electronically. While primarily designed for business and payroll taxes, individuals who regularly make estimated tax payments can also benefit.

- How it Works:

- You must enroll in EFTPS, which involves an online application and receiving a PIN via postal mail (this can take 5-7 business days).

- Once enrolled, you can schedule payments up to 365 days in advance, directly from your checking or savings account.

- You’ll receive an immediate confirmation number upon scheduling a payment.

- Advantages: Allows for advance scheduling, provides robust payment history records, and is free. Excellent for managing recurring tax obligations.

- Best For: Businesses, self-employed individuals, and anyone who makes frequent or recurring federal tax payments.

Traditional and Alternative Payment Methods: When Digital Isn’t an Option

While digital payments offer unparalleled convenience, the IRS still provides traditional and alternative methods for those who prefer or require them.

1. Payment by Mail: Check or Money Order

Paying by mail remains a viable option, though it’s slower and comes with specific instructions to ensure your payment is correctly applied.

- How it Works:

- Make your check or money order payable to the “U.S. Treasury.”

- On the memo line, write your name, address, daytime phone number, Social Security number (or Employer Identification Number for businesses), the tax year, and the related tax form or notice number.

- Do not staple your payment to your tax return. For most individual income tax payments, include Form 1040-V, Payment Voucher.

- Mail your payment to the correct IRS address, which varies depending on your location and the form you are filing. Always check IRS.gov for the most current mailing addresses.

- Disadvantages: Slower processing, risk of mail delays or loss, no immediate confirmation.

- Best For: Those without access to electronic banking or who prefer traditional payment methods, although generally not recommended due to lack of immediate confirmation and slower processing.

2. Cash Payments: Through Retail Partners

For taxpayers who prefer to pay with cash, the IRS offers options through various retail partners.

- How it Works:

- You must first obtain a payment code or use a service like PayNearMe or VanillaDirect. This usually involves visiting IRS.gov or calling the IRS to get a payment barcode or authorization.

- Take the barcode or authorization to a participating retail store (e.g., 7-Eleven, Family Dollar, CVS Pharmacy).

- Make your cash payment. The store will provide a receipt confirming the transaction.

- Limits and Security: There may be daily payment limits (e.g., $500 per payment). Keep your receipt as proof of payment.

- Best For: Taxpayers who exclusively use cash and need a secure way to make their payments.

3. Wire Transfers: For International or Large Sum Payments

In specific circumstances, typically involving large payments or international taxpayers, wire transfers may be an appropriate method.

- How it Works:

- You must contact the IRS for specific instructions on how to initiate a wire transfer. This is not a standard method for most taxpayers.

- For international payments, foreign taxpayers can usually pay through an international money order, a check drawn on a U.S. bank, or through an authorized third-party service.

- Best For: Non-U.S. residents, certain foreign businesses, or taxpayers making extremely large payments under specific IRS guidance.

Important Considerations and Best Practices

Regardless of the payment method you choose, a few best practices can help ensure your payment is processed correctly and your financial information remains secure.

Verifying Your Payment and Keeping Records

- Confirmation Numbers: Always save any confirmation numbers you receive when making electronic payments. These are your proof of payment.

- Bank Statements: Review your bank or credit card statements to ensure the payment was successfully debited or charged.

- Receipts: Keep physical receipts for cash payments and print confirmation emails for electronic ones. Maintain records for at least three years, as recommended by the IRS.

- IRS Account: You can also check your payment history and balance due by creating or logging into your online IRS account on IRS.gov.

What to Do If You Can’t Pay

If you find yourself in a situation where you owe taxes but cannot pay them in full by the due date, do not ignore the problem. The IRS offers several options:

- Apply for a Payment Plan (Installment Agreement): You can request a short-term payment plan (up to 180 days) or a long-term installment agreement (up to 72 months) to make monthly payments. While interest and penalties still apply, this prevents further collection actions.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owed. This is generally an option if you are experiencing significant financial difficulty and cannot pay your full tax liability.

- Request an Extension to File, Not to Pay: Remember, filing Form 4868 grants an extension to file your return, but your payment is still due by the original deadline. Always pay what you can to minimize penalties and interest.

- Communicate with the IRS: Proactively contacting the IRS to discuss your situation is crucial. They are often willing to work with taxpayers who are genuinely trying to resolve their tax issues.

Avoiding Scams and Protecting Your Information

Tax-related scams are rampant, and it’s vital to be vigilant. The IRS generally initiates contact via mail, not unsolicited phone calls or emails, especially regarding payment demands.

- Recognize Official Communications: The IRS will never demand immediate payment via phone call, email, text message, or social media. They will not ask for your credit or debit card numbers over the phone.

- Use Official Channels: Only use official IRS.gov websites or approved third-party payment processors. Be wary of unofficial websites or individuals claiming to be IRS agents.

- Secure Internet Connection: When making online payments, ensure you are using a secure internet connection (e.g., not public Wi-Fi) to protect your financial information.

In conclusion, managing your tax payments to the IRS doesn’t have to be a source of stress. By understanding your obligations, utilizing the secure electronic payment options, and knowing your alternatives, you can ensure timely compliance and maintain a healthy financial standing. Always prioritize accuracy, keep meticulous records, and don’t hesitate to seek professional financial advice if your tax situation is particularly complex.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.