In the modern financial landscape, the seamless movement of money is predicated on a series of digital handshakes. Whether you are setting up direct deposit for a new job, authorizing an automated bill payment, or transferring funds between investment accounts, you will inevitably be asked for two primary pieces of information: your account number and your routing number. While your account number is unique to your specific relationship with a bank, the routing number serves as the “address” for the financial institution itself.

Understanding how to locate and verify your routing number is a fundamental skill in personal finance. This guide explores the most efficient methods to retrieve this information, the technical architecture behind these nine-digit codes, and the nuances you must understand to ensure your transactions are processed without delay.

Understanding the Role of the Routing Transit Number (RTN)

Before searching for the digits, it is essential to understand what a routing number actually represents. Formally known as a Routing Transit Number (RTN), this system was developed by the American Bankers Association (ABA) in 1910. Its original purpose was to facilitate the physical sorting and shipment of paper checks, but today, it serves as the backbone of the electronic payment network.

What is a Routing Number?

A routing number is a nine-digit code used to identify a specific financial institution in the United States. It acts as a digital roadmap, telling the Federal Reserve or the Automated Clearing House (ACH) exactly where a transaction should be directed. The first four digits typically identify the Federal Reserve Bank district, the next four represent the specific institution, and the final digit is a check digit used for mathematical validation.

The Difference Between Routing and Account Numbers

A common point of confusion for many consumers is the distinction between the routing number and the account number. Think of the routing number as the zip code for your bank; it identifies the building or the network. The account number, conversely, is your specific “apartment number” within that building. While thousands of people may share the same routing number at a large institution like Chase or Bank of America, your account number is unique to you. You need both to complete most financial transactions.

Top 5 Methods to Find Your Routing Number Quickly

In an era of digital-first banking, there are several ways to access your routing number. Depending on whether you prefer physical documents or mobile interfaces, one of the following methods will provide the answer in seconds.

1. Checking Your Physical Paper Checks

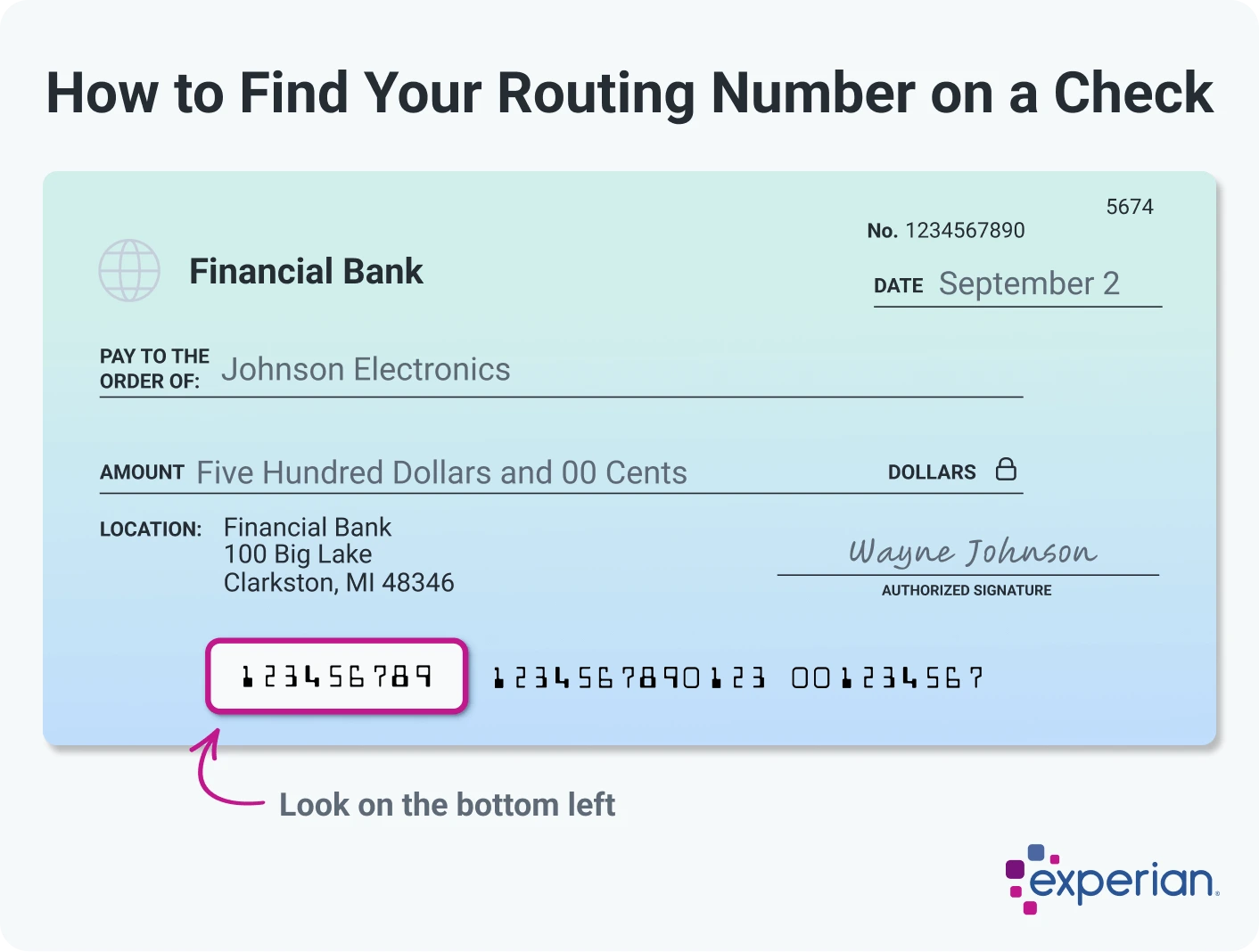

If you have a checkbook, the most reliable way to find your routing number is to look at the bottom of a check. At the bottom-left corner, you will see a string of numbers printed in a specialized font (MICR). The first nine-digit sequence, bracketed by unique symbols, is your routing number. The sequence following it is usually your account number, followed by the specific check number.

2. Utilizing Mobile Banking and Online Portals

For those who have moved away from paper checks, your bank’s mobile app or website is the most convenient tool. Once you log in, navigate to the “Account Details” or “Account Information” section. Most modern banking interfaces will display the routing number alongside your current balance. Some banks even offer a “Copy” button specifically for the routing number to prevent transcription errors when pasting it into other financial forms.

3. Reviewing Monthly Bank Statements

Your monthly bank statement—whether received via mail or downloaded as a PDF—contains a wealth of identifying information. Typically, the routing number is located in the header or the “Account Summary” section of the statement. This is an excellent method for those who need official documentation of the number for a mortgage application or tax filing.

4. Searching the Bank’s Official Website

Many national banks use a single routing number for all customers in a specific state or region. If you do not have your login credentials handy, you can often search the bank’s public website for “Routing Numbers.” Be cautious, however, as large institutions may have different numbers for different regions or different types of transactions (such as wire transfers vs. ACH).

5. Contacting Customer Service Directly

If you are dealing with a smaller credit union or a bank that has recently undergone a merger, the most secure way to verify your routing number is to call the customer service department. A representative can confirm the correct number for your specific account type, ensuring that you don’t accidentally use an outdated or incorrect code.

Routing Numbers in the Digital Age: Wire Transfers vs. ACH

One of the most frequent mistakes in personal finance is assuming that a bank has only one routing number. Depending on the type of transaction you are performing, the number you need may change.

Domestic ACH Transfers

The Automated Clearing House (ACH) network handles the majority of consumer transactions, including direct deposits, payroll, and monthly utility payments. This is the “standard” routing number found on the bottom of your checks. It is designed for batch processing and usually takes 1–3 business days for funds to clear.

International and Domestic Wire Transfers

Wire transfers are used for high-value, real-time movements of money, such as a down payment on a home. Many banks utilize a specific “Wire Routing Number” that is different from their ACH routing number. Using an ACH routing number for a wire transfer—or vice versa—can result in the transaction being rejected or, in some cases, the funds being held in a suspense account for weeks. Always verify with your bank if a specialized wire number is required before initiating a large transfer.

Security and Privacy: Protecting Your Financial Information

Because a routing number is essentially a public identifier for a bank, many people wonder how much of a security risk it poses if shared. While a routing number alone cannot be used to steal your identity, it is a piece of the puzzle that fraudsters look for.

Is a Routing Number Public Information?

Generally, yes. You can find the routing numbers for major banks through a simple Google search or the ABA’s online lookup tool. Because many people share the same routing number, it is not considered “private” in the same way a Social Security number is. However, when paired with your account number, it provides the keys to your financial “front door.”

Best Practices for Financial Security

To maintain the integrity of your personal finance ecosystem, only provide your routing and account numbers to trusted entities. Be wary of providing this information over unencrypted email or to unfamiliar websites. When setting up a side hustle or an online income stream, ensure the platform uses a secure payment processor like Stripe or Plaid, which tokenizes your data so the merchant never sees your actual banking details.

Common Challenges and Troubleshooting

Even with the right tools, finding or using a routing number can sometimes be complicated by corporate shifts or technical requirements.

What to Do If Your Bank Has Merged

The banking industry is constantly consolidating. If your bank was recently acquired (for example, if you were a BBVA customer moved to PNC), your routing number will eventually change. Most banks provide a “grace period” where the old routing number remains active for 6–12 months. However, to avoid a disruption in your paycheck or bill payments, you should update your information to the new parent bank’s routing number as soon as they provide it to you.

Verifying Numbers for Third-Party Apps

When linking your bank account to apps like Venmo, PayPal, or investment platforms like Robinhood, you may be asked for your routing number to manually verify your account. If the app fails to recognize the number, double-check that you aren’t accidentally entering the routing number for a savings account when you intended to use a checking account. Some savings accounts have restricted routing capabilities that prevent them from being linked to certain third-party payment apps.

Conclusion

The routing number is an essential cog in the machinery of personal and business finance. While it may seem like a simple string of digits, it represents your entry point into the global financial network. By knowing where to find it—whether on a physical check, through a mobile portal, or via a bank statement—and understanding the difference between ACH and wire codes, you can manage your money with greater confidence and precision. In an era where financial speed is paramount, having this information at your fingertips ensures that your capital always reaches its destination on time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.