Creating a budget is not just about restricting yourself; it’s about empowering yourself. It’s a foundational cornerstone of sound personal finance, offering a clear roadmap to achieving your financial aspirations, whether they involve buying a home, saving for retirement, paying off debt, or simply gaining peace of mind. Without a budget, your financial journey is akin to sailing without a compass, susceptible to unforeseen currents and destination drift.

Many people view budgeting with apprehension, associating it with deprivation or complexity. In reality, a well-crafted budget is a tool for liberation, providing clarity on where your money comes from and, more importantly, where it goes. It allows you to make conscious decisions about your spending, align your expenditures with your values, and systematically work towards your goals. This comprehensive guide will demystify the budgeting process, offering practical steps and strategies to help you build a financial framework that truly works for you.

The Foundation: Understanding Why and What to Budget

Before diving into the mechanics, it’s crucial to understand the fundamental principles that underpin effective budgeting. A budget isn’t a static document; it’s a dynamic reflection of your financial life, designed to evolve as your circumstances change.

Defining Your “Why”: Financial Goals as Your Compass

The most powerful motivator for creating and sticking to a budget is a clear understanding of why you’re doing it. What are your financial goals? Are you saving for a down payment on a house, an emergency fund, a child’s education, or an early retirement? Perhaps you’re focused on aggressively paying down high-interest debt.

Identifying specific, measurable, achievable, relevant, and time-bound (SMART) goals transforms budgeting from a chore into a purposeful endeavor. Your goals act as your financial compass, guiding your spending decisions and helping you prioritize. When faced with a discretionary purchase, you can ask yourself: “Does this align with my financial goals?” This simple question can be a powerful deterrent against impulse spending and keeps you focused on the bigger picture.

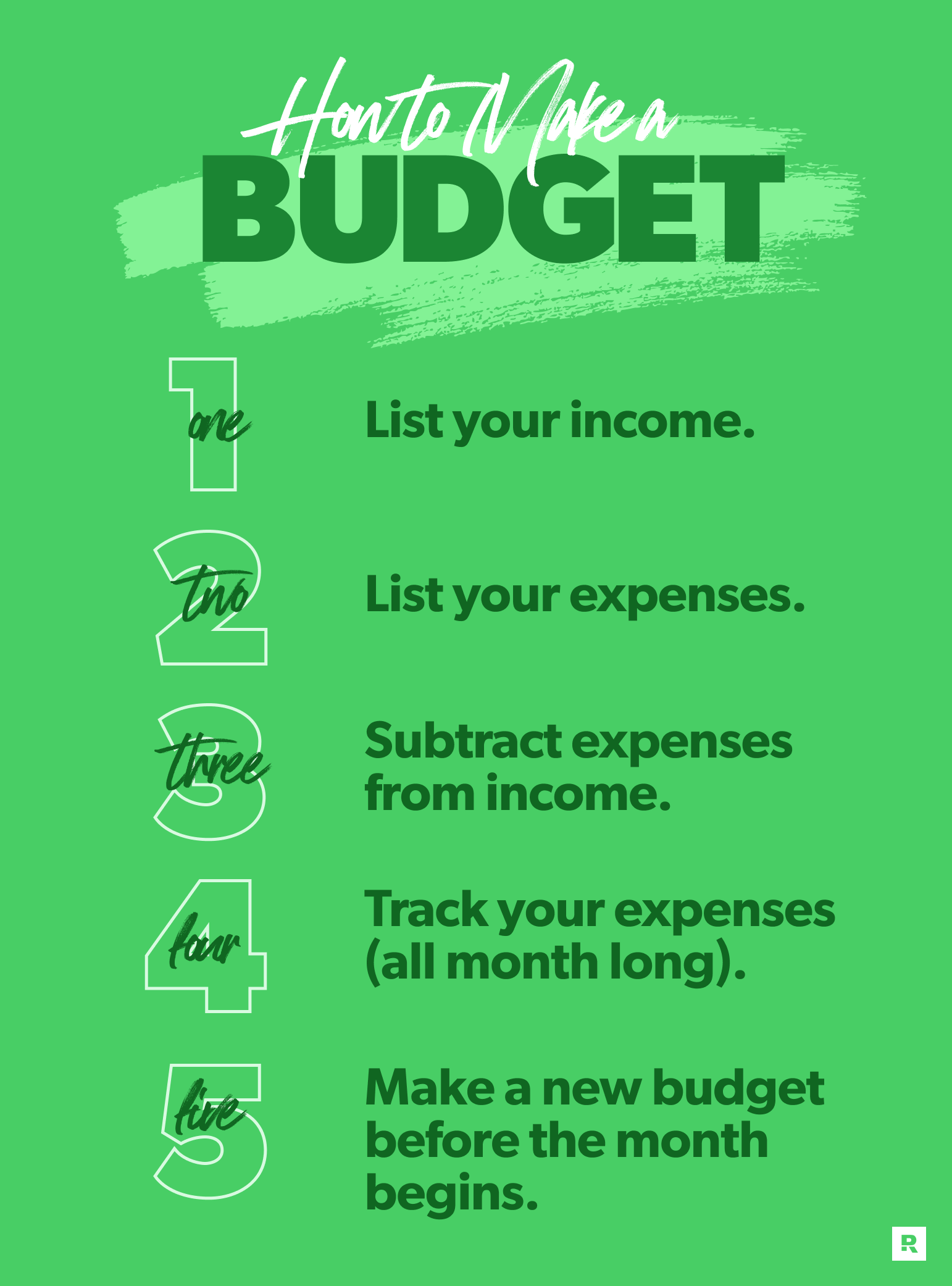

Decoding Your Income: The Starting Point

The first tangible step in creating any budget is to accurately assess your net income. This refers to the money you actually receive after taxes, deductions, and contributions (like 401k or health insurance premiums) have been taken out. It’s not your gross salary.

Gather all sources of income – your regular paycheck, freelance earnings, rental income, benefits, or any other money flowing into your accounts over a typical month. Be precise and realistic. If your income fluctuates significantly month-to-month, consider using an average of the last few months or budgeting for the lowest expected income to ensure you don’t overspend. Knowing your exact take-home pay provides the absolute ceiling for your spending and savings.

Unmasking Your Spending: Fixed vs. Variable Expenses

Once you know your income, the next critical step is to understand your expenses. All expenses can generally be categorized into two types:

- Fixed Expenses: These are costs that typically remain the same month after month and are often contractual. Examples include rent/mortgage payments, car loans, insurance premiums, loan repayments, and subscriptions. These are generally non-negotiable in the short term.

- Variable Expenses: These are costs that fluctuate monthly and are often discretionary. Examples include groceries, utilities (which can vary with usage), dining out, entertainment, clothing, and transportation (gas, public transit). These are the areas where you often have the most control and can make adjustments to meet your budget targets.

The key to successful budgeting lies in accurately identifying and tracking both types of expenses. Many people underestimate their variable spending, leading to budget shortfalls. A thorough review of your bank statements and credit card bills will provide the data needed to understand your true spending patterns.

A Step-by-Step Guide to Crafting Your Budget

With a clear understanding of your income and an initial grasp of your expenses, you’re ready to start building your budget. This process is iterative, meaning you’ll likely refine it over time.

Step 1: Gather Your Financial Data

Before you can budget, you need the raw data. Collect all relevant financial documents for the past 1-3 months:

- Bank statements (checking and savings)

- Credit card statements

- Pay stubs

- Utility bills

- Loan statements (student loans, car loans, mortgage)

- Any other receipts or financial records that indicate spending or income.

The more comprehensive your data, the more accurate your budget will be. This initial data collection phase is crucial for revealing where your money has actually been going, which can often be surprising.

Step 2: Categorize and Track Every Dollar

Go through your collected statements and categorize every single transaction. Create broad categories like Housing, Transportation, Food, Utilities, Debt Repayment, Savings, Entertainment, Personal Care, and Miscellaneous. Don’t be afraid to create more specific sub-categories as needed (e.g., under Food: Groceries, Restaurants, Coffee Shops).

This step is arguably the most insightful. Many people have a general idea of their major expenses but are often shocked by the cumulative impact of smaller, seemingly insignificant transactions. Tracking every dollar helps you see the “leaks” in your financial dam. You can do this manually on a spreadsheet, with pen and paper, or by using a budgeting app that automatically categorizes transactions (though always double-check its accuracy).

Step 3: Allocate Funds and Set Spending Limits

Now that you have your income and a detailed breakdown of your expenses, it’s time to create your actual budget. Subtract your total expenses from your total net income. Ideally, you want a positive number, meaning you have money left over. If you have a negative number, your spending exceeds your income, and immediate adjustments are necessary.

For each expense category, allocate a specific amount of money you intend to spend for the upcoming month. Be realistic, especially in the beginning. It’s better to overestimate slightly than to constantly fall short.

- Prioritize Needs: Start with your fixed expenses and essential variable costs (e.g., housing, utilities, groceries, transportation). These are non-negotiable.

- Address Debt and Savings: Allocate funds towards debt repayment beyond the minimums and, crucially, towards your savings goals (emergency fund, retirement, etc.). Many financial experts recommend “paying yourself first” by dedicating a portion of your income to savings before anything else.

- Allocate to Wants: Once needs, debt, and savings are covered, allocate remaining funds to discretionary spending categories like dining out, entertainment, hobbies, and personal shopping. This is where your financial goals from Step 1 will guide your decisions. If a goal is critical, you might significantly reduce “want” spending to free up more money for savings or debt repayment.

The goal is to ensure that your total allocated expenses (including savings and debt repayment) do not exceed your net income.

Step 4: Monitor, Review, and Adjust Regularly

Creating a budget is not a one-time event; it’s an ongoing process. Throughout the month, continually monitor your spending against your allocated limits in each category. This can be done daily, weekly, or bi-weekly, depending on your preference and the tools you use.

At the end of each month, review your budget’s performance:

- Did you stick to your limits?

- Where did you overspend or underspend?

- Were your initial allocations realistic?

- Have your income or expenses changed?

Based on this review, make necessary adjustments for the upcoming month. Perhaps you allocated too little for groceries and too much for entertainment, or maybe an unexpected car repair means you need to reallocate funds from another category next month. Flexibility is key. The first few months of budgeting are often a learning curve, and consistent adjustments will lead to a more accurate and effective budget over time.

Exploring Diverse Budgeting Methodologies

While the core steps remain consistent, different budgeting methods offer various frameworks to organize your finances. Choosing the right one depends on your personal preferences, financial situation, and discipline level.

The 50/30/20 Rule: A Balanced Approach

This popular method suggests allocating your after-tax income into three main categories:

- 50% for Needs: This covers essential expenses like housing, utilities, groceries, transportation, and minimum loan payments.

- 30% for Wants: This includes discretionary spending such as dining out, entertainment, hobbies, shopping, and vacations.

- 20% for Savings & Debt Repayment: This portion is dedicated to building an emergency fund, retirement savings, investing, and paying down debt beyond the minimums.

The 50/30/20 rule provides a straightforward guideline and is an excellent starting point for many, especially those new to budgeting. It emphasizes balance and ensures that both current needs and future goals are addressed.

Zero-Based Budgeting: Giving Every Dollar a Job

Zero-based budgeting involves assigning every single dollar of your income a “job” before the month begins. This means that your income minus your expenses (including savings and debt repayment) should equal zero.

Instead of just tracking where your money went, you proactively decide where it will go. This method requires meticulous planning and discipline but offers immense clarity and control over your finances. It ensures that no money is “lost” or spent without intention. If you have $3,000 in income, you will allocate exactly $3,000 across all categories, ensuring no dollar is unaccounted for.

The Envelope System: A Tangible Approach

This method is particularly effective for those who prefer a tactile approach or struggle with overspending on variable expenses using credit cards. The envelope system involves withdrawing a set amount of cash for certain variable spending categories (like groceries, entertainment, or dining out) at the beginning of the month and placing that cash into separate envelopes labeled with the category.

Once the cash in an envelope is gone, you stop spending in that category until the next budgeting period. This physically restricts your spending and makes you more conscious of each purchase. While less practical for all expenses in a digital world, it can be powerful for categories where you tend to overspend.

Pay Yourself First: Prioritizing Savings

While not a full budgeting system on its own, “Pay Yourself First” is a powerful budgeting philosophy that can be integrated into any method. It advocates for prioritizing savings and debt repayment by automatically transferring funds to these accounts before you pay any other bills or spend on discretionary items.

By automating these transfers to your savings or investment accounts immediately after you get paid, you ensure that your financial future is prioritized. What’s left over then becomes the amount you budget for your needs and wants, naturally encouraging more disciplined spending.

Sustaining Your Budget: Tools, Tips, and Overcoming Obstacles

Creating a budget is only half the battle; the real victory lies in consistently sticking to it and adapting it over time.

Choosing the Right Budgeting Tools

The best budgeting tool is the one you will consistently use.

- Spreadsheets (Excel, Google Sheets): Offer maximum flexibility and customization. You build it from scratch, tailoring it precisely to your needs. This requires a bit more upfront effort but provides unparalleled control.

- Budgeting Apps and Software: Many apps (like Mint, YNAB, Personal Capital, Simplifi) can link to your bank accounts and credit cards, automatically categorizing transactions and providing real-time insights into your spending. They often include features for goal setting, bill reminders, and net worth tracking. While they provide convenience, it’s essential to understand their features and ensure data security.

- Pen and Paper: Simple, cost-effective, and effective for those who prefer a less digital approach. It forces you to manually record every transaction, which can heighten awareness of your spending.

Regardless of the tool, the underlying principles of tracking income, categorizing expenses, and setting limits remain the same.

Strategies for Dealing with Irregular Income

If your income fluctuates (e.g., freelancers, commission-based jobs), budgeting requires a slightly different approach:

- Budget for Your Minimum: Base your essential expenses on your lowest expected monthly income.

- Create an Income Buffer: Build up a savings fund dedicated solely to bridging gaps during low-income months.

- Prioritize Savings with Windfalls: When higher income months occur, prioritize putting extra money towards savings, debt, or future fixed expenses.

- Allocate by Category Percentage: Instead of fixed amounts, budget a percentage of your income for each category.

Cultivating Budgeting Discipline and Avoiding Burnout

Budgeting requires discipline, but it doesn’t mean you can never enjoy your money.

- Be Realistic: Don’t cut out all discretionary spending at once. This can lead to frustration and abandonment of the budget. Start with small, manageable cuts.

- Allow for “Fun Money”: Include a small allowance for guilt-free spending in your budget. This prevents feelings of deprivation.

- Track Your Progress: Seeing your savings grow or debt shrink is incredibly motivating. Celebrate small wins along the way.

- Find an Accountability Partner: Discussing your budget with a trusted friend or family member can provide support and encourage consistency.

The Power of Flexibility and Regular Adjustments

Life is unpredictable, and your budget needs to be able to adapt.

- Expect the Unexpected: Build an emergency fund for unforeseen expenses. This prevents a single event from derailing your entire financial plan.

- Review Quarterly/Annually: Beyond monthly reviews, take a broader look at your budget every few months or annually. Major life changes (new job, marriage, children, moving) will necessitate significant budget revisions.

- Don’t Be Afraid to Tweak: If a category consistently goes over or under budget, adjust it. Your budget is a living document, not a rigid set of rules etched in stone. Its purpose is to serve you, not the other way around.

Creating a budget is one of the most impactful steps you can take towards financial stability and freedom. It transforms abstract financial worries into concrete plans, allowing you to take control of your money rather than letting your money control you. By understanding your income and expenses, setting clear goals, employing a suitable methodology, and diligently monitoring your progress, you’ll not only create a budget but also build a powerful tool that propels you towards a more secure and prosperous future. Start today, and watch your financial clarity grow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.