Determining exactly how much you owe the government is one of the most significant financial questions an individual or business owner will face each year. For many, the calculation feels like a “black box”—an opaque process where numbers go in and a bill (or a refund) comes out. However, understanding the mechanics of tax liability is a fundamental pillar of personal finance. It allows for better budgeting, smarter investment choices, and the peace of mind that comes with financial predictability.

Calculating your tax liability is not a single calculation but a multi-step journey that moves from your total earnings down to your final obligation. Whether you are a traditional W-2 employee, a freelancer in the gig economy, or a seasoned investor, the following guide breaks down the essential components of the tax equation to help you answer the question: how much do I actually owe?

Understanding the Foundation of Your Tax Bill

Before you can determine your tax bill, you must first define what the government considers “income.” Not every dollar that enters your bank account is treated equally, and understanding the nuances of income classification is the first step toward an accurate estimate.

Gross Income vs. Adjusted Gross Income (AGI)

Your “Gross Income” is the starting point. This includes wages, bonuses, tips, interest from bank accounts, dividends, capital gains, and even gambling winnings. For those in the “Money” niche, tracking these various streams is essential.

However, you rarely pay taxes on your raw gross income. The tax code allows for “above-the-line” deductions, which are subtracted from your gross income to arrive at your Adjusted Gross Income (AGI). Common adjustments include contributions to a traditional IRA, student loan interest payments, and health savings account (HSA) contributions. Your AGI is a critical figure because it often determines your eligibility for various tax credits and further deductions.

Taxable Income: The Final Number

The journey from AGI to “Taxable Income” involves the application of either the standard deduction or itemized deductions. As of the current tax laws, a significant majority of taxpayers opt for the standard deduction due to its simplicity and relatively high threshold.

Your taxable income is the actual amount upon which the tax rates are applied. If your AGI is $80,000 and you take a standard deduction of $14,600 (for a single filer in 2024), your taxable income is $65,400. This is the number that matters most when looking at tax tables. Understanding this distinction prevents the common mistake of applying tax percentages to one’s total salary, which leads to an overestimation of the debt owed.

Navigating Tax Brackets and Rates

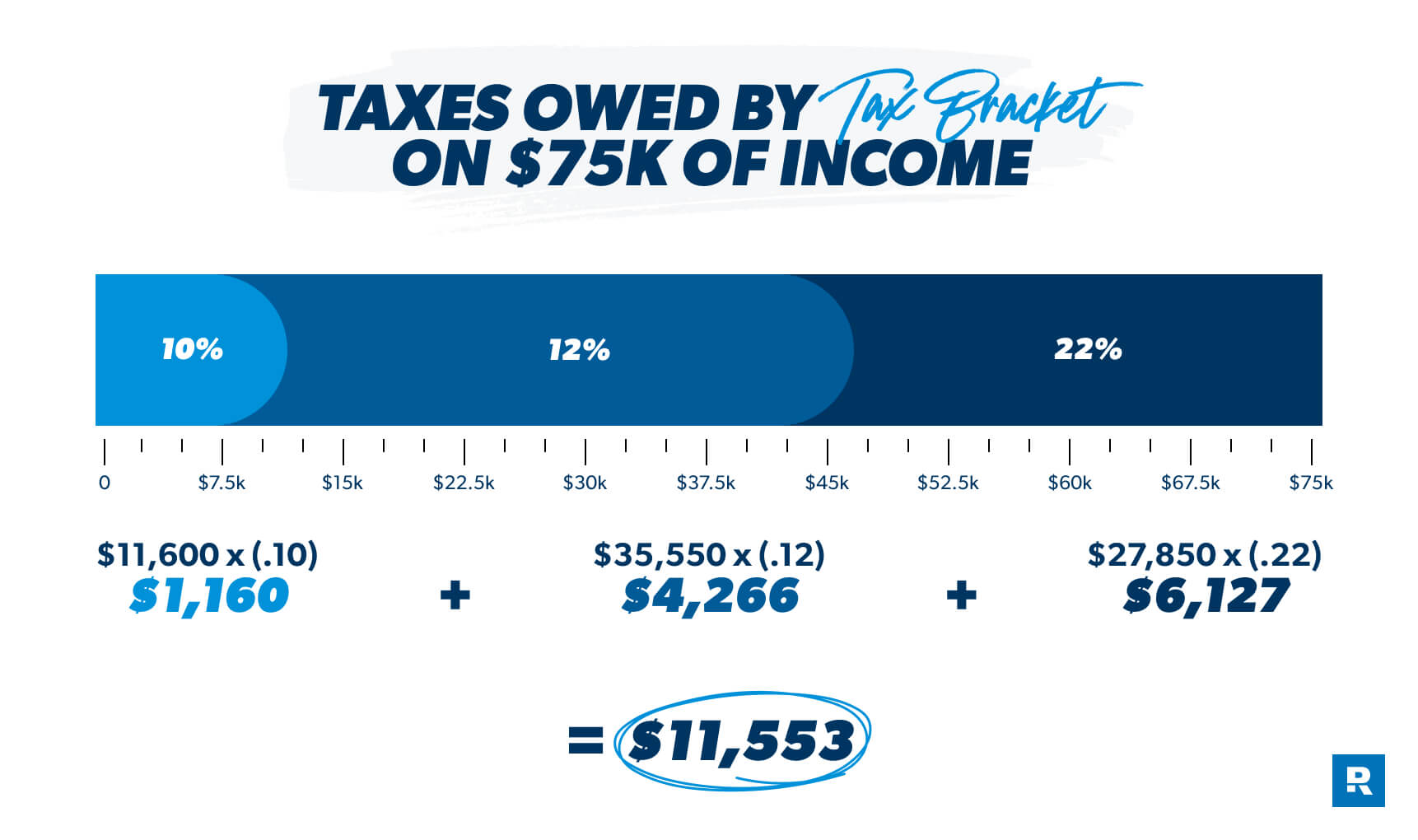

One of the most persistent myths in personal finance is that moving into a higher tax bracket means all your income is now taxed at that higher rate. In reality, the United States (and many other nations) utilizes a progressive tax system.

The Progressive Tax System Explained

A progressive tax system is designed so that different portions of your income are taxed at different rates. For example, if you fall into the 22% bracket, you do not pay 22% on every dollar. Instead, your first bucket of income is taxed at 10%, the next bucket at 12%, and only the portion that spills over into the highest bucket is taxed at 22%.

This structure ensures that earning more money almost always results in more “take-home” pay, even if the marginal rate on those last few dollars is higher. When asking “how much taxes do I owe,” you must calculate the tax for each “bucket” and sum them up to find your total income tax.

Marginal vs. Effective Tax Rates

To truly master your money, you must distinguish between your marginal tax rate and your effective tax rate. Your marginal rate is the highest bracket you touch—it is the rate you would pay on the next dollar you earn. This is helpful for deciding whether to take a side hustle or put more money into a 401(k).

Your effective tax rate, however, is the actual percentage of your total income that goes to the IRS. You find this by dividing your total tax owed by your total earned income. For most people, the effective rate is significantly lower than the marginal rate. Tracking your effective rate over several years is a great way to measure the efficiency of your financial planning and tax-mitigation strategies.

Reducing the Burden: Deductions and Credits

Once you have calculated your initial tax based on the brackets, the work isn’t over. The tax code provides two primary mechanisms to lower your bill: deductions and credits. While people often use these terms interchangeably, they function very differently in a financial context.

Standard vs. Itemized Deductions

As mentioned earlier, deductions lower the amount of income you are taxed on. The decision to “itemize” depends on whether your specific deductible expenses—such as mortgage interest, state and local taxes (SALT), and charitable contributions—exceed the standard deduction amount set by the IRS.

For high-income earners or those with significant medical expenses, itemizing can lead to a lower taxable income. However, for the average earner, the standard deduction usually provides the greatest benefit with the least amount of paperwork. The choice between the two is a pivotal moment in the tax-filing process that can shift your liability by thousands of dollars.

Non-Refundable vs. Refundable Credits

If deductions are good, credits are better. While a deduction lowers your taxable income, a tax credit is a dollar-for-dollar reduction of the actual tax you owe. If you owe $5,000 in taxes and qualify for a $2,000 credit, your bill drops directly to $3,000.

Credits come in two forms:

- Non-Refundable Credits: These can reduce your tax liability to zero, but the government will not cut you a check for any “leftover” credit. Examples include the Child and Dependent Care Credit.

- Refundable Credits: These are the gold standard of the tax world. If the credit exceeds what you owe, you receive the difference as a refund. The Earned Income Tax Credit (EITC) and the Child Tax Credit (partially refundable) are prime examples. Identifying these credits is the most effective way to drastically reduce the total amount of taxes you owe.

Specialized Considerations for Modern Earners

The “how much do I owe” question becomes more complex for those who don’t fit the traditional 9-to-5 mold. Modern wealth creation often involves multiple streams of income, each with its own set of rules.

Self-Employment and the Gig Economy

If you are a freelancer, contractor, or business owner, you are responsible for both the employee and employer portions of Social Security and Medicare taxes, collectively known as Self-Employment (SE) tax. This adds roughly 15.3% to your tax burden on top of standard income taxes.

However, self-employed individuals also have access to a wider array of deductions. You can deduct “ordinary and necessary” business expenses, such as home office costs, professional software, marketing expenses, and a portion of your health insurance premiums. For this demographic, the key to knowing how much you owe lies in meticulous bookkeeping and quarterly estimated payments.

Investment Income and Capital Gains

For those focused on investing and building a portfolio, taxes on “unearned income” are a major consideration. If you sell an asset (like stocks or real estate) for a profit, you owe capital gains tax.

- Short-term capital gains (assets held for a year or less) are taxed at your ordinary income rates.

- Long-term capital gains (assets held for more than a year) enjoy preferential rates of 0%, 15%, or 20%, depending on your income level.

Strategically timing the sale of assets—a practice known as tax-loss harvesting—can allow you to offset gains with losses, effectively lowering the total taxes you owe on your investment portfolio.

Planning and Tools for Accurate Estimation

The final step in determining your tax liability is comparing what you owe with what you have already paid. Most Americans pay their taxes throughout the year via employer withholding or quarterly estimated payments.

Using Withholding and Estimated Payments

If you are an employee, your W-4 form dictates how much your employer takes out of each paycheck. If you find yourself owing a large sum every April, you likely have too little withheld. Conversely, a massive refund means you’ve essentially given the government an interest-free loan.

For those with complex finances, the IRS “Tax Withholding Estimator” is an invaluable digital tool. By inputting your latest paystubs and expected investment income, you can get a real-time snapshot of your standing. This allows you to adjust your withholding mid-year to ensure you hit the “Safe Harbor” rules, avoiding underpayment penalties.

Financial Planning for the Next Tax Year

Knowing how much you owe today is the first step toward owing less tomorrow. Tax planning is a year-round activity, not an April event. By understanding your brackets and the impact of deductions, you can make informed decisions throughout the year. Should you contribute more to your 401(k)? Should you donate to charity before December 31st? Should you realize a gain on a stock now or wait until it qualifies for long-term rates?

Ultimately, taxes are the largest recurring expense for most people. By treating the calculation of your tax liability as a core component of your personal finance strategy rather than a source of stress, you gain control over your financial future. Understanding the math behind the “how much” allows you to focus on the “how to”—how to grow your wealth, how to protect your assets, and how to build a lasting financial legacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.