For many taxpayers, the realization that they might have an outstanding balance with the Internal Revenue Service (IRS) brings a sense of immediate anxiety. Whether it stems from a missed filing, a mathematical error on a previous return, or an unexpected change in income, the question “How much do i owe the IRS?” is one of the most critical inquiries in the realm of personal finance. Managing tax debt is not merely about compliance; it is a fundamental component of maintaining financial health and long-term stability.

Understanding your tax liability requires navigating a complex landscape of digital tools, official notices, and statutory interest rates. This guide provides a deep dive into how to determine your balance, why that balance may have grown over time, and the strategic financial tools available to help you resolve your debt while protecting your credit and assets.

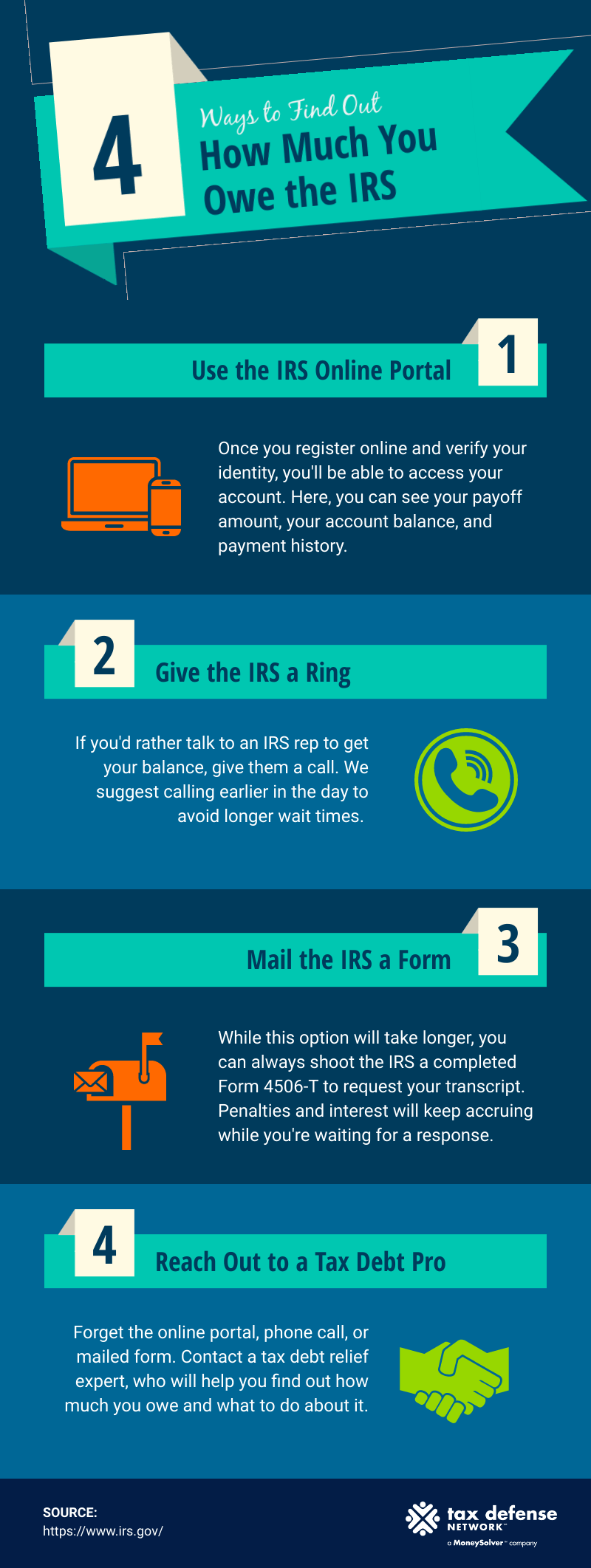

Determining Your Liability: How to Check What You Owe

The first step in resolving any financial obligation is gaining total transparency over the numbers. Gone are the days when taxpayers had to wait weeks for a paper letter to arrive in the mail to understand their standing. Today, the IRS has digitized many of its processes, allowing for more immediate access to financial data.

Using the IRS Online Account Tool

The most efficient way to find your current balance is through the IRS Online Account portal. This secure platform provides a real-time snapshot of your federal tax obligations. By creating an account (which requires identity verification through services like ID.me), you can view the total amount owed, broken down by tax year. Beyond the raw numbers, the portal allows you to view your payment history, see key information from your most recent tax return, and even view digital copies of select notices sent by the agency. This tool is the gold standard for anyone practicing proactive personal finance management.

Requesting Transcripts via Mail or Phone

For those who prefer traditional methods or are unable to pass the digital identity verification, requesting a tax transcript is the alternative. There are several types of transcripts, but the “Tax Account Transcript” is the most useful for determining debt. It provides a detailed history of your account, including the original tax assessed, any subsequent adjustments made by the IRS, payments made, and accrued interest and penalties. While this can be requested via the “Get Transcript by Mail” tool or by calling the IRS directly, it requires patience, as physical delivery typically takes five to ten business days.

Understanding the Different Types of IRS Notices

Often, the first sign that you owe money is a letter in the mail. However, not all notices are created equal. A “Notice of Tax Due and Demand for Payment” (CP14) is usually the initial notification. If left unaddressed, this can escalate to a “Final Notice of Intent to Levy” (CP504). Distinguishing between an informational inquiry and an urgent demand for payment is crucial for prioritizing your financial responses. High-level financial planning involves reading these notices carefully to ensure the IRS’s calculations align with your own records, as errors are not uncommon.

Why Your Balance Might Be Higher Than Expected

It is often a shock to taxpayers when the amount they owe is significantly higher than the original tax liability they calculated. This discrepancy is almost always a result of the statutory “add-ons” that the IRS is legally required to charge. Understanding these mechanics is vital for anyone looking to optimize their business or personal finance strategy.

Accrued Interest and Late Payment Penalties

The IRS is not just a collection agency; in some ways, it functions like a high-interest lender when payments are late. The interest rate on underpayments is determined quarterly and is typically the federal short-term rate plus 3%. Because this interest compounds daily, a stagnant debt can grow exponentially over several years. This makes “ignoring the problem” one of the most expensive financial mistakes a person can make.

Failure-to-File vs. Failure-to-Pay

One of the most important distinctions in tax law is the difference between the penalty for not filing and the penalty for not paying. The “Failure-to-File” penalty is much more severe, often 5% of the unpaid taxes for each month the return is late. In contrast, the “Failure-to-Pay” penalty is 0.5% per month. From a strategic money management perspective, it is always better to file your return on time—even if you cannot afford to pay a single cent—because it stops the more aggressive 5% penalty from accruing.

Common Errors and Underreporting Issues

Sometimes, you owe the IRS more because of a “CP2000” notice, which occurs when the information reported on your return doesn’t match the information the IRS received from third parties (like 1099s from a side hustle or W-2s from an employer). In the age of the “gig economy,” many freelancers forget to report income from smaller digital platforms, leading to automated audits. Reviewing these discrepancies is essential; if the IRS’s information is wrong, you have the right to challenge the assessment and potentially lower your debt.

Strategic Payment Options and Financial Tools

Once the balance is confirmed, the focus shifts to resolution. The IRS offers several “Financial Tools” designed to help taxpayers settle their debt without facing immediate financial ruin. Choosing the right path depends on your liquid assets, monthly cash flow, and long-term financial goals.

Short-Term and Long-Term Installment Agreements

For those who cannot pay in full immediately but have steady income, an Installment Agreement (IA) is the most common solution. A short-term plan gives you up to 180 days to pay the balance in full, often with lower administrative fees. A long-term plan (or “payment plan”) allows for monthly payments for up to 72 months. While interest continues to accrue, setting up an IA prevents the IRS from taking more aggressive collection actions like wage garnishments or bank levies.

Offer in Compromise (OIC)

The “Offer in Compromise” is often touted by late-night commercials as a way to “settle for pennies on the dollar.” In reality, the OIC is a rigorous financial tool reserved for those who truly cannot pay their debt without experiencing extreme hardship. The IRS examines your “Reasonable Collection Potential” by looking at your assets, future income, and necessary living expenses. If you qualify, the OIC can be a life-changing financial reset, but the application process is exhaustive and requires full transparency of your financial life.

“Currently Not Collectible” Status

If your financial situation is so dire that paying the IRS would prevent you from covering basic living expenses (rent, food, utilities), you may request “Currently Not Collectible” (CNC) status. This does not erase the debt, and interest continues to build, but it halts all collection activities. From a personal finance standpoint, this is a temporary bridge used during periods of unemployment or medical crisis to protect your immediate survival.

Proactive Financial Planning to Avoid Future Debt

The ultimate goal of financial literacy is to move from a state of “reaction” to a state of “proaction.” Once you understand how much you owe and how to pay it, the next step is ensuring you never find yourself in this position again.

Adjusting Your Withholdings (Form W-4)

For W-2 employees, the most common reason for owing money is an incorrectly filed Form W-4. If you have multiple jobs, a working spouse, or significant non-wage income, the standard withholding might not be enough. Using the IRS Tax Withholding Estimator tool once or twice a year can help you fine-tune your withholdings, ensuring you pay just enough throughout the year to avoid a large bill—and a penalty—at tax time.

Making Quarterly Estimated Payments for Freelancers

In the world of online income and side hustles, taxes are not withheld automatically. This places the burden of “tax collector” on the individual. Successful entrepreneurs and freelancers use the 1040-ES to make quarterly estimated payments. By treating tax as a recurring business expense rather than a once-a-year surprise, you maintain better cash flow and avoid the underpayment penalties that trap many small business owners.

Leveraging Tax Software and Professional Advice

While DIY tax software is excellent for simple returns, complex financial situations often benefit from a Certified Public Accountant (CPA) or Enrolled Agent (EA). These professionals can identify deductions and credits you might have missed, effectively lowering your total liability. In the context of “Money,” paying for professional tax advice is often an investment that yields a high return in the form of tax savings and peace of mind.

The Psychological and Financial Impact of Tax Debt

It is important to acknowledge that tax debt is not just a line item on a balance sheet; it is a heavy psychological burden. Financial stress can cloud judgment, leading to poor investment choices or a lack of motivation in one’s career.

By taking control of your IRS balance, you are reclaiming your financial narrative. Transparency is the antidote to fear. When you know exactly what you owe, why you owe it, and what the plan is to pay it back, you move from a position of vulnerability to a position of power. In the broader scope of personal finance, mastering your relationship with the IRS is a milestone of maturity. It signals that you are ready to manage your wealth with the discipline and strategy required for long-term prosperity.

Whether you utilize online tools to check your balance today or consult with a professional to draft an Offer in Compromise, the act of engagement is your most valuable asset. The IRS is a powerful entity, but it provides a clear framework for resolution. By following the steps outlined in this guide, you can navigate your tax debt with professional precision and keep your financial future on track.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.