In the world of personal and business finance, few variables carry as much weight as the interest rate. Whether you are a first-time homebuyer, a seasoned investor, or a small business owner looking to expand, the question “what is the interest rate today?” is more than a casual inquiry—it is a fundamental query that dictates your purchasing power, your investment returns, and your long-term financial security.

Interest rates function as the “price of money.” When rates are low, borrowing is cheap, encouraging spending and investment. When rates are high, borrowing becomes expensive, and the incentive shifts toward saving. Today, we find ourselves in a complex economic climate where interest rates have moved away from the historic lows of the last decade, settling into a “higher for longer” paradigm that requires a sophisticated understanding of the financial markets.

The Mechanics of Modern Interest Rates

To understand what the interest rate is today, one must first understand the machinery that drives it. Interest rates are not set by a single entity in a vacuum; rather, they are the result of monetary policy, inflation expectations, and market demand.

The Federal Reserve and the Federal Funds Rate

The primary driver of interest rates in the United States is the Federal Reserve, specifically the Federal Open Market Committee (FOMC). The Fed sets the “Federal Funds Rate,” which is the target interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. While this rate isn’t what you pay on your credit card directly, it serves as the benchmark for almost all other consumer and business rates. When the Fed raises this rate to combat inflation, the “Prime Rate”—the base rate that banks charge their most creditworthy corporate customers—rises in tandem.

How Inflation Drives Interest Rate Policy

The relationship between inflation and interest rates is inverse and intentional. Central banks use interest rates as a thermostat to control the heat of the economy. When inflation rises above the typical 2% target, the economy is considered “overheated.” By raising interest rates today, the Fed makes it more expensive for businesses to borrow for expansion and for consumers to buy cars or homes on credit. This cooling effect reduces demand, which eventually slows down price increases. Conversely, if the economy is sluggish, the Fed lowers rates to “grease the wheels” of commerce.

Navigating Different Types of Interest Rates in Today’s Market

When someone asks “what is the interest rate today?”, they are often referring to a specific financial product. There is no single universal rate, but rather a spectrum of rates influenced by risk, duration, and collateral.

Mortgage Rates: The Cost of Homeownership

For the average consumer, mortgage rates are the most visible manifestation of interest rate policy. These rates are traditionally tied to the yield on the 10-year Treasury note. In the current market, we have seen 30-year fixed-rate mortgages fluctuate significantly. Unlike the 3% rates seen in 2021, today’s rates often hover in the 6% to 7% range. This shift has a profound impact on “housing affordability,” as a few percentage points can add hundreds of dollars to a monthly payment, effectively pricing some buyers out of the market while cooling the pace of home sales.

Consumer Credit and Personal Loan Rates

Interest rates on credit cards and personal loans are generally much higher than mortgage rates because they are “unsecured”—meaning there is no house or car for the bank to seize if you stop paying. Today, credit card APRs (Annual Percentage Rates) frequently exceed 20%. In a high-rate environment, carrying a balance on a credit card becomes exponentially more dangerous to one’s financial health. On the other hand, personal loans and HELOCs (Home Equity Lines of Credit) have also seen upward pressure, making it essential for consumers to maintain high credit scores to access the “best” available rates.

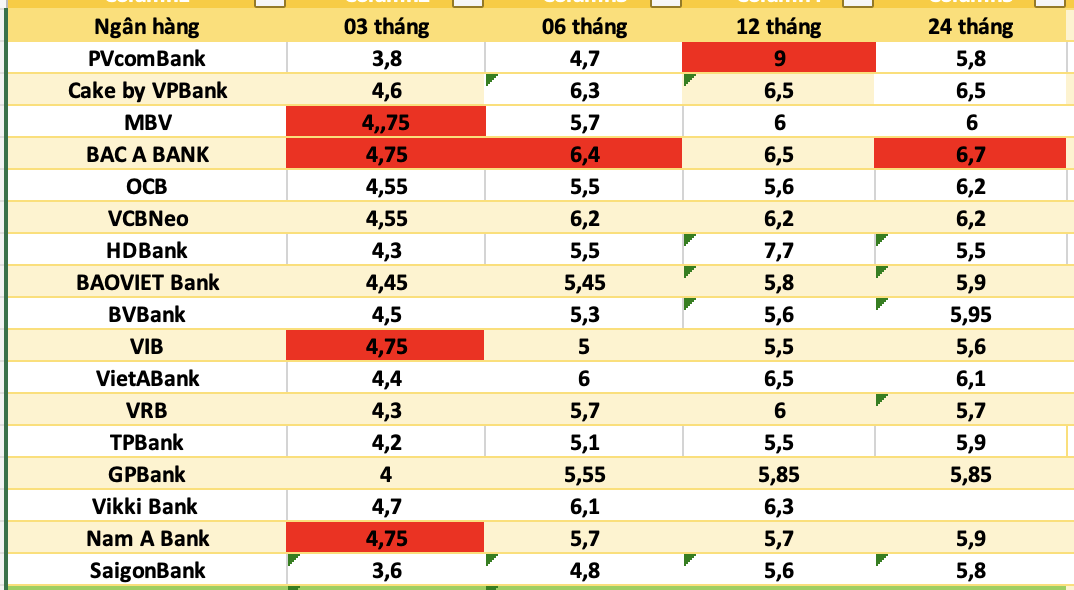

High-Yield Savings and Fixed-Income Yields

While high interest rates are a burden for borrowers, they are a boon for savers. For nearly a decade, savings accounts offered negligible returns. Today, however, “High-Yield Savings Accounts” (HYSAs) and Certificates of Deposit (CDs) offer rates that often exceed 4% or 5%. This has revitalized the “fixed-income” portion of many investment portfolios. Investors today can find “risk-free” returns on government-backed Treasury bills that were unimaginable just a few years ago, providing a safe haven during stock market volatility.

The Global Economic Context: Why Rates Are Shifting Now

The current state of interest rates is a direct response to the unprecedented economic events of the early 2020s. To manage your finances effectively, you must recognize the macro-trends that have led us to this point.

Post-Pandemic Recovery and Supply Chain Dynamics

The global economy experienced a massive shock during the COVID-19 pandemic, followed by a rapid infusion of fiscal stimulus. This, combined with snarled supply chains, led to a surge in demand that supply could not meet. The resulting inflation was the highest seen in forty years. In response, central banks across the globe began one of the most aggressive rate-hiking cycles in history to prevent an inflationary spiral. Today’s rates reflect the tail end of that battle, as the economy seeks a “soft landing”—cooling inflation without triggering a severe recession.

Quantitative Tightening vs. Easing

Beyond moving the benchmark rate, the Federal Reserve also manages the money supply through a process known as Quantitative Tightening (QT). By reducing the number of bonds it holds on its balance sheet, the Fed effectively removes liquidity from the financial system. This puts further upward pressure on long-term interest rates. Understanding this “invisible hand” of the Fed helps explain why mortgage rates might stay high even if the Fed stops raising the overnight funds rate.

Strategies for Managing Your Finances in a High-Rate Environment

In a high-interest rate environment, the financial “playbook” changes. The strategies that worked when money was “free” (near 0% rates) can be detrimental today.

Debt Management and Refinancing Tactics

The priority for any individual or business today should be the elimination of high-interest debt. If you are holding credit card debt at 22% interest, that is a “guaranteed” negative return on your wealth.

- Debt Consolidation: Consider moving high-interest balances to a lower-interest personal loan or a 0% APR balance transfer card if you have the credit score to qualify.

- The Refinancing Wait: For those who bought homes recently at peak rates, “waiting for the pivot” is the common strategy. This involves monitoring the market for a drop of at least 1% in mortgage rates to justify the closing costs of a refinance.

Optimizing Your Investment Portfolio

High interest rates change the “discount rate” used to value stocks. When you can get 5% from a Treasury bond, a risky tech stock looks less attractive.

- Bond Ladders: Investors are currently using “bond ladders”—buying fixed-income securities that mature at different intervals—to lock in today’s high yields while maintaining liquidity.

- Yield over Growth: In high-rate environments, investors often shift focus from “growth stocks” (which rely on cheap borrowing) to “value stocks” or dividend-paying companies that have strong cash flows and less reliance on debt.

Future Outlook: Predicting the Next Move in Interest Rates

Predicting the exact path of interest rates is notoriously difficult, but several key indicators can help us forecast the trend.

Economic Indicators to Watch

Financial analysts keep a close eye on the “Consumer Price Index” (CPI) and the “Personal Consumption Expenditures” (PCE) price index. These are the Fed’s preferred measures of inflation. If these numbers trend downward toward the 2% goal, the pressure to keep rates high will subside. Additionally, the “Jobs Report” (Non-Farm Payrolls) is crucial; if the labor market remains too strong, it may keep wages rising, which in turn keeps inflation—and interest rates—higher for longer.

Long-term Financial Planning in Volatile Markets

The “new normal” for interest rates is likely somewhere between the 0% floor of the 2010s and the double-digit peaks of the 1980s. For long-term planning, it is wise to assume a moderate-rate environment. This means:

- Stress-testing your budget: Can you afford your lifestyle if your variable-rate loans increase?

- Maintaining an Emergency Fund: Use today’s high-yield savings rates to build a 6-month cushion.

- Diversification: Ensure your portfolio isn’t solely reliant on low interest rates to succeed.

In conclusion, “what is the interest rate today” is a question that touches every corner of your financial life. While high rates present challenges for borrowing, they offer unique opportunities for saving and conservative investing. By staying informed on the Federal Reserve’s movements and understanding the difference between various rate types, you can navigate this economic cycle with confidence and protect your path to financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.