Navigating the landscape of personal and business finance often brings individuals face-to-face with a myriad of tax terms, each with its own nuances and implications. Among the most common yet frequently misunderstood are payroll taxes and income taxes. While both represent compulsory contributions to government revenue, they serve distinct purposes, are levied differently, and fund disparate public services. Understanding the fundamental differences between these two vital components of the tax system is crucial for effective financial planning, budgeting, and ensuring compliance. This article will demystify payroll tax and income tax, clarifying their unique roles, mechanisms, and impact on your financial well-being.

Understanding Payroll Taxes: The Employer-Employee Contribution

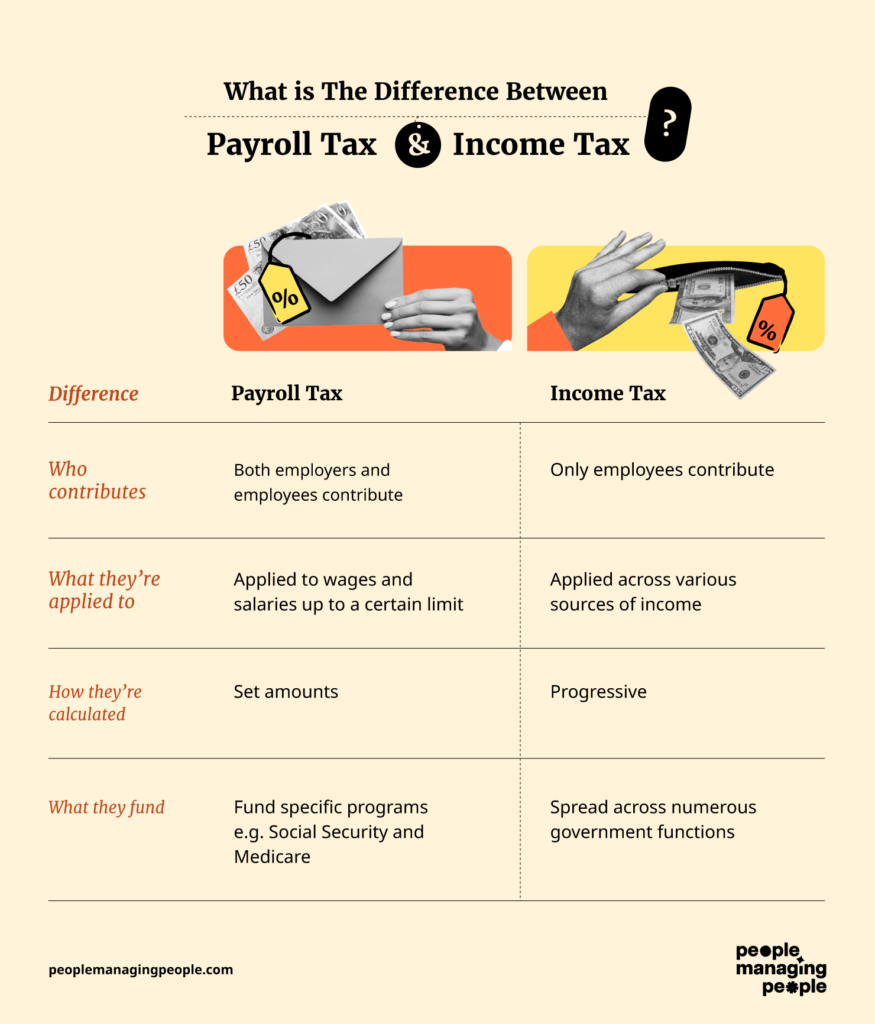

Payroll taxes are a specific type of tax directly tied to employment wages and salaries. They are typically withheld from an employee’s gross pay by their employer, who then remits these funds to the appropriate government agencies, often matching a portion of the contributions themselves. These taxes are earmarked for particular social programs, distinguishing them from the broader revenue-generating purpose of income taxes.

What Payroll Taxes Fund

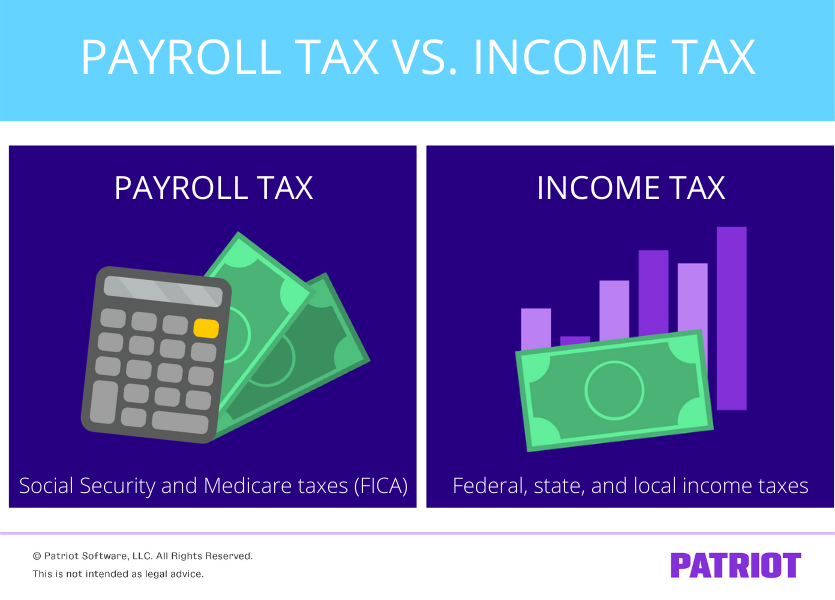

The primary beneficiaries of payroll taxes are social insurance programs designed to provide a safety net for workers and their families. In the United States, for instance, the most prominent payroll taxes are for Social Security and Medicare, collectively known as FICA (Federal Insurance Contributions Act) taxes.

- Social Security provides retirement benefits, disability income, survivor benefits, and spousal benefits. It ensures that qualifying individuals have a source of income after they stop working or if they are unable to work due to disability.

- Medicare funds healthcare services for individuals aged 65 or older, as well as younger people with certain disabilities or end-stage renal disease. It covers hospital insurance, medical insurance, and prescription drug costs.

Some states or localities may also have their own forms of payroll taxes, such as those funding unemployment insurance or workers’ compensation programs, though these are often borne solely by the employer.

Who Pays What

A defining characteristic of payroll taxes is the shared responsibility between employees and employers. For FICA taxes:

- Employees contribute a percentage of their gross wages up to a certain annual limit for Social Security, and a flat percentage of all wages for Medicare. This portion is directly deducted from their paycheck.

- Employers are required to match the employee’s contribution for Social Security and Medicare. This employer-paid portion is an additional cost of employment, distinct from the employee’s wages.

For example, if the Social Security tax rate is 6.2% and the Medicare tax rate is 1.45%, an employee pays 7.65% of their wages (up to the Social Security wage base), and the employer pays an additional 7.65%. This effectively doubles the total contribution to 15.3%. For high-income earners, an additional Medicare tax may apply, which is solely borne by the employee. Self-employed individuals bear the full burden of both the employer and employee portions, paying the “self-employment tax” which is equivalent to the combined FICA rates.

Withholding and Reporting

Employers are legally obligated to withhold payroll taxes from each employee’s paycheck and periodically deposit these funds with the government. They must also report these withholdings on forms such as Form W-2, which employees receive at the end of the year. This form details the employee’s gross wages, the amount of Social Security and Medicare taxes withheld, and other taxes. This system ensures consistent funding for social programs and streamlines the collection process. Non-compliance can lead to significant penalties for employers.

Demystifying Income Taxes: Your Share of Earnings

Income tax, in contrast to payroll tax, is a broader tax levied on an individual’s or entity’s total financial income. This can include wages, salaries, investment income (like dividends, interest, and capital gains), rental income, business profits, and various other forms of earnings. Its primary purpose is to generate general revenue for the government to fund a wide array of public services, from national defense and infrastructure to education and healthcare, which are not specifically covered by social insurance programs.

Federal vs. State Income Tax

In the United States, income tax is primarily collected at two levels:

- Federal Income Tax: This is levied by the U.S. government on all taxable income earned by its citizens and residents, regardless of where they live. It is the largest single source of revenue for the federal budget.

- State Income Tax: Most, but not all, U.S. states also impose an income tax. The rates and rules vary significantly from state to state, with some states having flat tax rates, others having progressive rates, and a few having no state income tax at all. Additionally, some local governments may also levy their own income taxes.

Progressive Tax System

The federal income tax system, and many state income tax systems, operate on a progressive basis. This means that as an individual’s taxable income increases, they pay a higher percentage of that income in taxes. Income is divided into brackets, with different tax rates applying to income falling within each bracket. For example, the first portion of income might be taxed at 10%, the next portion at 12%, and so on, with higher income thresholds subject to incrementally higher rates. This contrasts with a flat tax system where everyone pays the same percentage regardless of income, or a regressive system where lower incomes pay a higher percentage.

Deductions, Credits, and Exemptions

A significant feature of the income tax system is the allowance for various deductions, credits, and, historically, exemptions, which can reduce an individual’s taxable income or the actual tax owed.

- Deductions reduce the amount of income subject to tax. They can be standard deductions (a fixed amount based on filing status) or itemized deductions (specific expenses like mortgage interest, state and local taxes, or medical expenses).

- Tax Credits directly reduce the amount of tax owed, dollar for dollar. A $1,000 credit reduces your tax bill by $1,000. Credits can be non-refundable (reducing tax to zero but not resulting in a refund) or refundable (potentially resulting in a refund even if no tax was owed). Examples include the Child Tax Credit or the Earned Income Tax Credit.

- Exemptions (personal and dependent) were historically used to reduce taxable income based on the number of people supported by the taxpayer. While federal personal exemptions were eliminated with the Tax Cuts and Jobs Act of 2017, some state income tax systems may still incorporate similar concepts.

These provisions allow taxpayers to lower their overall income tax burden based on their financial circumstances, expenditures, and family size.

Key Distinctions and Overlapping Realities

While both payroll and income taxes are compulsory government levies, their core characteristics set them apart in fundamental ways.

Purpose and Funding Mechanisms

The most significant distinction lies in their purpose. Payroll taxes are specifically designated for social insurance programs (e.g., Social Security, Medicare), acting like contributions to a collective insurance fund. The funds collected are typically held in dedicated trust funds for these specific programs. Income taxes, on the other hand, are a general revenue source, pooled into the government’s general fund to finance a broad spectrum of public goods and services chosen by legislative bodies. This difference impacts not only where your tax dollars go but also how they are accounted for by the government.

Taxpayer Responsibility

The responsibility for paying and reporting these taxes also differs. For employed individuals, payroll taxes are automatically withheld by the employer, who also contributes a matching portion. This makes the employee’s direct payment largely passive. Income tax, while also often withheld from paychecks, requires active participation from the taxpayer. Individuals must file an annual tax return (e.g., Form 1040) to calculate their total income tax liability, claim deductions and credits, and either pay any remaining balance or receive a refund. Self-employed individuals have a greater direct responsibility for both, paying estimated taxes throughout the year for both their income tax and self-employment (payroll) taxes.

Impact on Your Take-Home Pay

Both payroll and income tax withholdings directly reduce your take-home pay, or net pay. However, the calculation and perception of these deductions can vary. Payroll taxes (FICA) are generally a straightforward percentage of your wages (up to the Social Security limit), with the employee portion being a consistent deduction. Income tax withholding, determined by your W-4 form and income level, is often an estimate designed to prevent a large tax bill or refund at year-end, and can be adjusted based on personal circumstances. Understanding these deductions is crucial for accurate personal budgeting and financial planning.

Strategic Financial Planning Around These Taxes

Effective management of your finances necessitates a clear understanding of both payroll and income taxes, as they significantly impact your cash flow and long-term financial health.

Maximizing Withholding Accuracy

For income tax, adjusting your W-4 form with your employer allows you to influence how much federal income tax is withheld from each paycheck. While many opt for standard withholding, you can adjust it to avoid a large tax bill or to reduce a large refund if you prefer more money in your pocket throughout the year. For payroll taxes, particularly for the self-employed, accurate tracking of income and expenses is paramount to correctly calculate and pay estimated self-employment taxes. Errors in withholding or estimated payments can lead to penalties.

Leveraging Tax-Advantaged Accounts

Understanding the impact of both tax types can guide your use of tax-advantaged retirement and savings accounts. Contributions to pre-tax retirement accounts, such as a traditional 401(k) or IRA, reduce your taxable income for income tax purposes, leading to immediate income tax savings. While these contributions do not typically reduce the amount of payroll taxes you pay on your wages, the overall reduction in taxable income can be substantial over time. Health Savings Accounts (HSAs) offer a triple tax advantage: tax-deductible contributions (reducing taxable income), tax-free growth, and tax-free withdrawals for qualified medical expenses, again impacting your income tax liability.

Professional Guidance for Complex Situations

For individuals with complex financial situations—such as those with multiple income streams, significant investment income, self-employment, or intricate deduction scenarios—seeking advice from a qualified tax professional is invaluable. Tax accountants, enrolled agents, or financial planners specializing in tax can help optimize your tax strategy, ensure compliance, identify overlooked deductions or credits, and plan for future tax liabilities, integrating both payroll and income tax considerations into a holistic financial plan.

The Broader Economic Impact

Beyond individual financial planning, payroll and income taxes play critical roles in the broader economy. Payroll taxes ensure the stability of essential social safety nets, directly contributing to the well-being and economic security of millions of Americans, which in turn supports consumer spending and economic stability. Income taxes provide the general revenue necessary for public investments in infrastructure, research, education, and defense, all of which are foundational to economic growth and national prosperity. The structure and rates of these taxes are subject to ongoing policy debates, reflecting differing philosophies on economic equity, government’s role, and fiscal responsibility, underscoring their profound and far-reaching impact.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.