Tax equity represents a specialized form of financing primarily used for capital-intensive projects that generate significant tax credits and depreciation benefits. It’s a critical mechanism that allows project developers, who may not have sufficient tax liability to utilize these benefits themselves, to monetize them by selling a portion of the project’s ownership or cash flow rights to large institutional investors. These investors, often corporations with substantial tax obligations, are willing to provide upfront capital in exchange for the predictable stream of tax benefits, effectively reducing their own taxable income. This symbiotic relationship accelerates project development, particularly in sectors deemed strategically important, such as renewable energy and affordable housing, which are often incentivized through federal and state tax programs.

The Fundamental Concept of Tax Equity

At its core, tax equity is about optimizing the allocation of tax attributes. Many large-scale projects, especially those with high upfront costs and long operational lifespans, are eligible for various governmental incentives designed to encourage investment in specific areas. These incentives often come in the form of tax credits (which directly reduce a taxpayer’s liability dollar-for-dollar) and accelerated depreciation (which allows a business to deduct a larger portion of an asset’s cost in the early years).

Bridging Tax Liabilities with Project Investment

The challenge for many project developers, particularly startups or those expanding rapidly, is that they may not generate enough taxable income to fully utilize these substantial tax benefits in the immediate future. A developer building a new solar farm, for instance, might incur significant capital expenditures but may not be profitable enough in its first few years to effectively claim the full investment tax credit (ITC) or production tax credit (PTC), alongside depreciation deductions. This is where tax equity investors step in. These investors, typically large financial institutions or corporations with consistent, high taxable income, possess the capacity to absorb and utilize these benefits immediately. By investing in the project, they acquire the rights to these tax benefits, using them to offset their own tax liabilities, while simultaneously providing essential capital to the project developer.

Key Players in a Tax Equity Structure

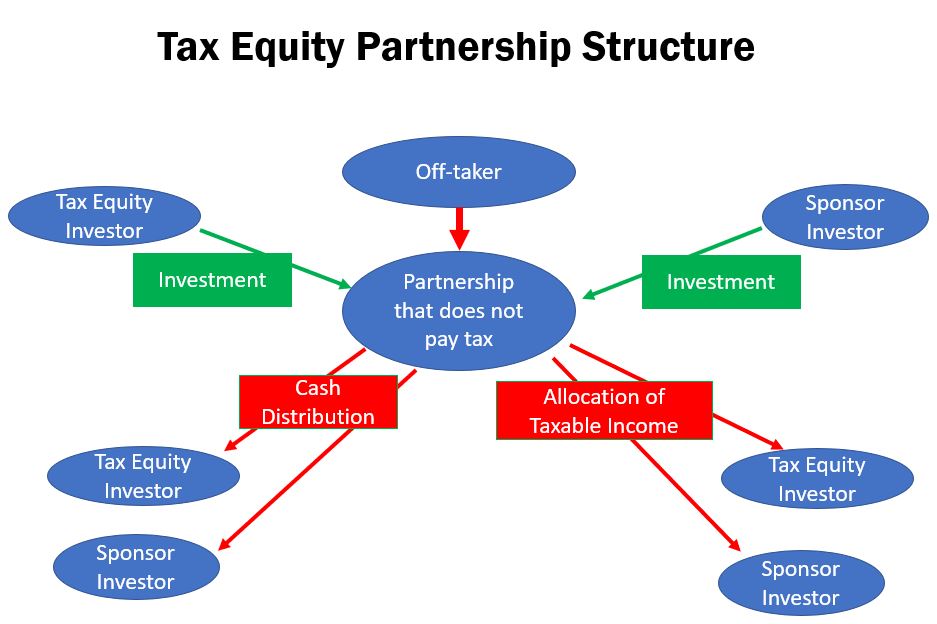

A typical tax equity transaction involves several key participants, each with distinct roles and motivations:

- Project Sponsor/Developer: This entity originates and develops the project, manages its construction and operation, and seeks capital to finance it. They benefit from reduced capital costs and the ability to realize value from tax attributes they couldn’t otherwise use.

- Tax Equity Investor: These are typically large financial institutions, banks, or corporate investors with significant tax appetites. They invest capital into the project in exchange for a share of its ownership, primarily driven by the desire to capture the tax credits and depreciation deductions generated by the project. Their investment decision is heavily influenced by the predictability and magnitude of these tax benefits.

- Lenders (Debt Providers): While tax equity provides a significant portion of the capital, most large projects also require traditional debt financing. Lenders provide senior debt, secured by the project’s assets and cash flows, operating alongside the tax equity and sponsor equity.

- Legal and Financial Advisors: Given the complexity of tax law, partnership agreements, and financial modeling, specialized legal and financial advisors are crucial for structuring and executing these intricate transactions.

How Tax Equity Structures Work

Tax equity structures are sophisticated financial arrangements designed to efficiently transfer tax benefits from the project to the investor. The most common structures include partnership flips and various lease structures.

The Role of Tax Credits and Depreciation

The core incentives driving tax equity are generally:

- Investment Tax Credit (ITC): A direct credit against federal income tax liability, calculated as a percentage of the eligible basis of qualified energy property placed in service. For example, a 30% ITC on a $100 million solar project would provide $30 million in direct tax savings.

- Production Tax Credit (PTC): An annual credit per kilowatt-hour of electricity produced by eligible renewable energy facilities for a specified period (e.g., 10 years).

- Accelerated Depreciation (MACRS): Allows for faster recovery of the cost of tangible property through depreciation deductions, leading to larger deductions in the early years of an asset’s life, thereby reducing taxable income sooner. Bonus depreciation provisions can further enhance this benefit.

These benefits are “owned” by the owner of the project. A tax equity structure essentially allows the project developer to bring in an investor as a co-owner for a period, specifically to utilize these benefits.

Typical Project Types Utilizing Tax Equity

While theoretically applicable to any project generating substantial tax benefits, tax equity is most prevalent in:

- Renewable Energy Projects: Solar (utility-scale, commercial, residential portfolios), wind, geothermal, fuel cells, and biomass projects are major users, driven by ITCs and PTCs.

- Affordable Housing Projects: Low-Income Housing Tax Credits (LIHTC) are the primary driver here, encouraging the development and rehabilitation of affordable rental housing.

- Other Projects: Certain energy efficiency improvements, carbon capture projects, and historically rehabilitated buildings can also utilize tax equity, depending on specific legislative incentives.

The Investment Mechanism: Partnership Flips and Leases

The most common tax equity structure is the Partnership Flip. In this arrangement, the project sponsor and the tax equity investor form a limited liability company (LLC) or a limited partnership (LP) to own the project. The tax equity investor contributes capital to this partnership and receives a large percentage (often 99%) of the tax credits, depreciation, and early-stage cash flow until they achieve a pre-determined internal rate of return (IRR) or capital account balance. Once the investor reaches this “flip point,” their ownership percentage of the project’s cash flow and residual value “flips” down to a much smaller percentage (e.g., 5%), while the sponsor’s percentage increases significantly. The investor typically maintains a small equity interest for the remainder of the project’s life. This structure ensures the investor receives the bulk of the tax benefits when they are most valuable (early in the project’s life) while allowing the sponsor to regain control and a higher share of operational cash flows later.

Another structure is the Sale-Leaseback. In this model, the project sponsor sells the project’s assets to the tax equity investor, who then leases them back to the sponsor. The investor, as the owner, claims the tax credits and depreciation, while the sponsor operates the project and makes lease payments. This is less common for very large utility-scale projects due to potential complexities with tax credit allocation rules but is sometimes used for smaller, modular projects or equipment.

Benefits and Risks of Tax Equity Financing

Tax equity is a powerful financial tool, offering distinct advantages to both project sponsors and investors, but it also comes with inherent complexities and risks.

Advantages for Project Sponsors

For project developers, tax equity offers several compelling benefits:

- Lower Capital Costs: By monetizing tax attributes, sponsors can reduce the amount of traditional equity or debt required for a project, leading to a lower overall cost of capital. This makes otherwise unfinanceable projects viable.

- Access to Specialized Funding: It opens a channel to a specialized pool of capital from investors specifically seeking tax benefits, which might not be available through conventional lenders or equity providers.

- Risk Mitigation: By sharing ownership and some project risks with a sophisticated financial partner, sponsors can somewhat de-risk their ventures, especially in nascent industries or new technologies.

- Enhanced Project Development: The availability of tax equity financing accelerates the deployment of projects that align with public policy goals, such as renewable energy infrastructure.

Advantages for Tax Equity Investors

Tax equity investors also derive significant benefits from these structures:

- Predictable Tax Benefits: The primary driver is the reliable stream of tax credits and depreciation, which directly offsets their corporate tax liabilities. These are often more predictable than traditional investment returns.

- Competitive Returns: While the returns are tax-driven, the effective yield on a tax equity investment can be attractive when considering the direct tax savings.

- ESG and Green Investing Alignment: For many corporate investors, participation in renewable energy or affordable housing projects aligns with their Environmental, Social, and Governance (ESG) objectives and corporate social responsibility initiatives.

- Diversification: Tax equity investments can offer portfolio diversification, as their returns are often correlated more with tax policy and project operational stability than broader market cycles.

Navigating the Risks

Despite its advantages, tax equity financing is not without its challenges and risks:

- Regulatory and Tax Law Changes: Changes in tax law or interpretations by the IRS can significantly impact the value of tax credits and depreciation, posing a major risk to investors.

- Project Performance Risk: The actual generation of tax credits (especially PTCs) and operational cash flows is dependent on the project’s performance (e.g., wind speeds, solar irradiation, tenant occupancy). Underperformance can reduce investor returns.

- Basis Risk: For ITCs, the credit amount is based on the project’s eligible cost basis. Disputes over eligible costs or recapture events (where the asset is disposed of too early) can lead to unexpected tax liabilities for the investor.

- Complexity and Transaction Costs: Structuring tax equity deals is highly complex, involving extensive legal, tax, and financial due diligence. This results in significant transaction costs, making it typically suitable only for larger projects.

- IRS Scrutiny: Due to the often large sums involved and the complex nature of the structures, tax equity deals can be subject to rigorous scrutiny from the Internal Revenue Service, requiring meticulous compliance.

The Impact and Future of Tax Equity

Tax equity has played an indispensable role in financing critical infrastructure and social initiatives that align with national priorities. Its impact extends beyond mere financial transactions, influencing broader economic and environmental landscapes.

Driving Sustainable Development and Economic Growth

In the renewable energy sector, tax equity has been the single largest source of capital, facilitating the rapid expansion of solar and wind power across the globe. Without the ability to monetize ITCs and PTCs, many pioneering projects would simply not have been financially viable, slowing the transition to a cleaner energy grid. Similarly, in affordable housing, LIHTCs have been instrumental in addressing housing shortages and providing safe, quality housing for low-income communities. By attracting substantial private investment, tax equity indirectly stimulates job creation, technological innovation, and local economic development in these vital sectors.

Evolving Landscape and Policy Influences

The landscape of tax equity is dynamic, heavily influenced by legislative changes and evolving market conditions. Policy shifts, such as the introduction of new tax credits, extensions of existing ones, or changes to corporate tax rates, directly impact the demand and supply for tax equity. Recent legislation, like the Inflation Reduction Act (IRA) in the United States, has not only extended and enhanced existing tax credits but also introduced new mechanisms like “transferability” and “direct pay.” These provisions aim to broaden the market for tax benefits, potentially allowing a wider array of investors and even tax-exempt entities to benefit from project-generated credits, thereby reducing the reliance solely on traditional tax equity investors and possibly lowering transaction costs. While not fully replacing tax equity, these new mechanisms are expected to coexist and diversify financing options.

Strategic Considerations for Investors and Developers

For investors, strategic engagement in the tax equity market requires a deep understanding of tax law, comprehensive financial modeling capabilities, and robust risk management frameworks. Identifying reputable project sponsors, conducting thorough due diligence on project viability, and structuring agreements that protect against adverse tax events are paramount. Developers, on the other hand, must focus on structuring projects efficiently to maximize eligible tax benefits, building strong relationships with experienced tax equity investors, and navigating the complexities of construction, operation, and regulatory compliance. As the market evolves, both sides must remain agile, adapting to new policy incentives and exploring hybrid financing solutions that combine traditional tax equity with newer transferability or direct pay options, ensuring continued access to the capital necessary to drive impactful projects forward.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.