New Hampshire holds a unique position in the landscape of U.S. labor law, particularly concerning its minimum wage. Unlike many states that have established their own minimum wage rates exceeding the federal standard, New Hampshire currently defers entirely to the federal minimum wage. This distinction carries significant financial implications for individuals, businesses, and the broader economy within the Granite State, necessitating a deeper dive into its financial ramifications.

Understanding New Hampshire’s Minimum Wage Landscape

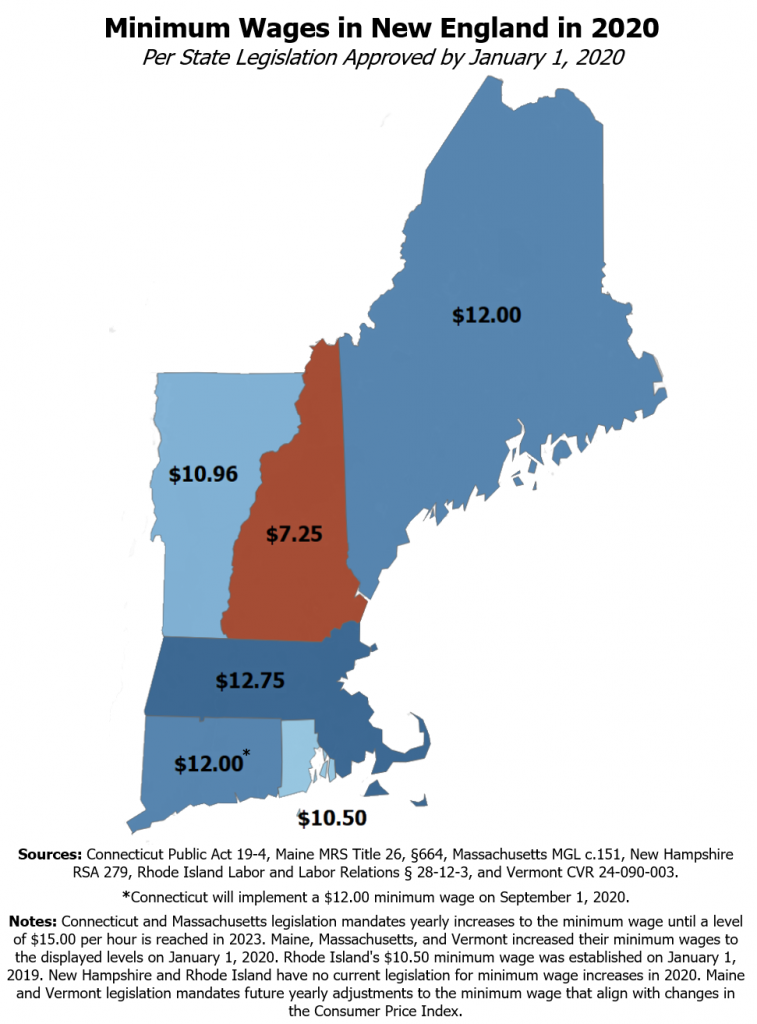

At present, New Hampshire’s official minimum wage is set at the federal rate of $7.25 per hour. This has been the standard since July 24, 2009, when the last federal increase took effect. The state’s decision to not establish its own, higher minimum wage is a long-standing legislative stance, often rooted in a philosophy that market forces, rather than government mandates, should primarily determine wage levels.

Historically, there have been numerous legislative attempts in New Hampshire to pass a state minimum wage law, with proposals ranging from modest increases to aligning with the rates of neighboring states. However, these efforts have consistently failed to gain sufficient traction or overcome gubernatorial vetoes. Proponents of maintaining the federal standard often argue that a higher state minimum wage could burden businesses, lead to job losses, and make the state less competitive economically. In contrast, advocates for a state minimum wage emphasize poverty reduction, increased consumer spending, and the basic dignity of a living wage.

To put New Hampshire’s approach into perspective, it’s useful to briefly consider its neighbors. Massachusetts, for instance, has a state minimum wage significantly higher than the federal rate, as does Vermont and Maine. This creates a distinct economic environment for businesses and workers in New Hampshire, where wage floors are among the lowest in the nation when considering state-level interventions. This reliance on the federal minimum wage fundamentally shapes the financial decisions and challenges faced by both employers and employees within the state.

Financial Implications for Individuals and Households

The $7.25 per hour minimum wage poses substantial challenges for individuals and households attempting to navigate the cost of living in New Hampshire. While the state is celebrated for its natural beauty and quality of life, it is not an inexpensive place to live, particularly concerning essential expenses.

The Cost of Living in New Hampshire

New Hampshire’s cost of living, especially for housing, energy, and transportation, often exceeds the national average. For an individual working full-time (40 hours a week) at $7.25 per hour, annual gross income totals approximately $15,080. This figure falls significantly below what is considered a livable wage in many parts of the state. For example, a single adult without children would likely need to earn considerably more just to cover basic needs without relying on public assistance, according to various living wage calculators. When factoring in the expenses for a family, the disparity becomes even more pronounced. The gap between the minimum wage and the actual cost of living necessitates difficult financial trade-offs, often leading to housing insecurity, food insecurity, and limited access to healthcare for those at the lowest end of the income spectrum.

Budgeting Challenges and Strategies

Individuals earning minimum wage in New Hampshire are frequently forced to employ rigorous and often stressful budgeting strategies. This might include working multiple jobs to piece together a sustainable income, often sacrificing work-life balance and personal well-being. Side hustles become not just supplemental income streams but essential components of a household budget. Many rely on government assistance programs, such as food stamps (SNAP), Medicaid, or housing subsidies, to bridge the financial gap, creating a situation where low wages effectively transfer costs from employers to taxpayers. Financial planning on such an income often revolves around scarcity, prioritizing immediate needs over long-term goals.

Impact on Personal Finance Goals

The ability to save, invest, or build wealth is severely hampered for those earning the minimum wage. Emergency funds, crucial for financial stability, are difficult to establish. Retirement savings, a cornerstone of long-term financial security, often remain an unattainable luxury. Debt accumulation, particularly high-interest credit card debt, can become a common pitfall as individuals struggle to cover unexpected expenses or even routine bills. This perpetuates a cycle of financial vulnerability, making upward economic mobility incredibly challenging without significant intervention or a change in employment.

The “Living Wage” Concept

It’s critical to distinguish between the statutory minimum wage and the concept of a “living wage.” A living wage is generally defined as the minimum income necessary for a worker to meet their basic needs (food, housing, healthcare, transportation, childcare) without relying on public assistance. In New Hampshire, the calculated living wage for even a single adult is substantially higher than $7.25 per hour. This disparity highlights the financial strain on minimum wage earners and underscores why many financial experts and policymakers argue for a higher wage floor to ensure greater economic stability and reduced poverty.

Economic Considerations for Businesses in New Hampshire

The absence of a state-mandated minimum wage higher than the federal standard also shapes the operational and strategic decisions for businesses across New Hampshire. While some argue it provides a competitive advantage, others point to market forces that compel businesses to pay above this statutory minimum regardless.

Business Operating Costs

For businesses, particularly those in sectors like hospitality, retail, and certain service industries where entry-level positions are common, labor costs are a significant component of their operating budget. The federal minimum wage of $7.25 per hour represents the absolute lowest legal wage they can pay. This allows businesses the flexibility to set wages based on their specific industry, location, and the prevailing market rates, potentially keeping baseline labor costs lower than in states with higher minimums. However, this theoretical advantage often clashes with the realities of a competitive labor market.

Wage Competition and Talent Acquisition

Despite the low statutory minimum, many New Hampshire businesses find themselves paying significantly more than $7.25 per hour. The primary driver for this is the need to attract and retain talent in a competitive labor market, especially in regions with low unemployment rates. If businesses only offered minimum wage, they would likely struggle to fill positions, as potential employees would seek better-paying opportunities elsewhere, whether in other companies within New Hampshire or in neighboring states with higher wages. Therefore, the “effective” minimum wage in many sectors is often dictated by supply and demand, rather than strictly by the federal mandate. Businesses must conduct thorough market analysis to determine competitive wage rates to ensure they can maintain adequate staffing levels and reduce employee turnover.

Impact on Consumer Spending

The debate around minimum wage often includes its potential impact on consumer spending. Proponents of higher minimum wages argue that putting more money into the pockets of low-wage earners can stimulate local economies, as these individuals are more likely to spend additional income on essential goods and services. This increased demand can, in turn, benefit local businesses. Conversely, opponents raise concerns that higher labor costs could force businesses to raise prices, potentially leading to inflation, or reduce their workforce to maintain profitability. The New Hampshire context allows for a natural experiment where these forces play out, with wages often being determined by market dynamics rather than state-level intervention.

Small Business Perspectives

Small businesses, which form the backbone of New New Hampshire’s economy, face a nuanced situation. While they might theoretically benefit from lower statutory wage floors, they are also often the most sensitive to local labor market conditions. Many small businesses pride themselves on offering competitive wages and benefits to foster loyalty and productivity. However, those operating on thin margins in highly competitive industries might feel the pinch more acutely if forced by market conditions to significantly exceed the $7.25 minimum, potentially impacting their ability to compete with larger corporations.

The Broader Economic Debate and Future Outlook

The discussion around New Hampshire’s minimum wage is inextricably linked to broader economic debates about labor markets, poverty, and economic growth.

Arguments For and Against a State Minimum Wage

The arguments for implementing a state minimum wage in New Hampshire often center on social equity and economic stimulus. Proponents contend it would lift thousands out of poverty, reduce reliance on public assistance, improve worker morale and productivity, and inject more money into the local economy through increased consumer spending. It’s seen as a moral imperative to ensure that full-time work provides a pathway out of poverty.

Conversely, opponents typically focus on the potential negative impacts on businesses. They argue that a state minimum wage could lead to job losses, particularly among less-skilled workers, as businesses reduce staff or automation to offset higher labor costs. Concerns about inflation, reduced business competitiveness, and the idea that government should not interfere with free-market wage determination are also frequently cited. The economic models supporting both sides often present conflicting data, making the debate complex.

Legislative Efforts and Public Sentiment

Despite the current deferral to the federal rate, legislative efforts to establish a state minimum wage in New Hampshire are a recurring feature of each legislative session. Public sentiment on the issue is often divided, with polls sometimes showing support for an increase, while other segments of the population prioritize fiscal conservatism and limited government intervention. The state’s political climate often sees these efforts stalled or defeated, reflecting a deeply ingrained philosophy regarding economic policy.

Economic Trends and Wage Growth

Regardless of the statutory minimum wage, actual wages in New Hampshire are significantly influenced by broader economic trends. Factors such as a low unemployment rate, labor shortages in specific sectors, and inflationary pressures often compel employers to offer wages well above $7.25 an hour to attract and retain employees. For example, during periods of strong economic growth and tight labor markets, even entry-level positions might command $15, $18, or even $20+ per hour, particularly in metropolitan areas or in industries facing talent scarcity. This means that for many working New Hampshirites, the federal minimum wage is a floor that is rarely, if ever, touched due to market dynamics. However, for those in the most vulnerable positions, it remains the legal baseline, often leading to underemployment or reliance on supplementary income.

Navigating Financial Realities in New Hampshire

For individuals working in New Hampshire, particularly those in entry-level or low-wage positions, a proactive approach to personal finance is crucial to thrive in an environment where the statutory minimum wage does not reflect the cost of living.

Financial Planning Beyond Minimum Wage

Strategies for individuals to improve their financial situation often involve increasing their earning potential. This can include investing in skill development, pursuing educational opportunities, or acquiring certifications that lead to higher-paying jobs. Exploring online income opportunities or developing profitable side hustles are also vital for supplementing income. Robust budgeting, aggressive debt management, and seeking out jobs that offer better wages and benefits are key to moving beyond the financial constraints imposed by low wages. Even small increases in income can make a substantial difference in budgeting and the ability to save.

Resources for Financial Support

For those struggling to make ends meet, New Hampshire offers various community resources and financial literacy programs. These can provide assistance with food, housing, healthcare, and education, as well as guidance on budgeting, saving, and debt reduction. Local non-profits, state agencies, and community organizations often serve as critical lifelines, helping individuals navigate complex financial challenges and access vital support networks.

The Role of Financial Tools

Leveraging modern financial tools can also be instrumental. Budgeting apps, personal finance software, and online banking platforms can help individuals track spending, manage savings, and set financial goals more effectively. These tools can provide a clear picture of one’s financial health, identify areas for improvement, and automate savings or bill payments, making it easier to manage finances strategically, even on a tight budget.

In summary, while New Hampshire’s official minimum wage mirrors the federal standard, the true financial landscape for its residents and businesses is shaped by a complex interplay of legislative decisions, market forces, and the inherent cost of living in the state. Understanding these dynamics is essential for informed personal finance decisions and for businesses seeking to thrive in New Hampshire’s distinctive economic climate.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.