Understanding what constitutes poverty level income for a single person is crucial for grasping the financial realities faced by millions and for evaluating the effectiveness of social safety nets. While the term “poverty line” often conjures images of dire circumstances, its definition is a statistical measure with significant implications for an individual’s financial well-being, access to aid, and overall quality of life. This federal benchmark serves as a critical indicator for policymakers, social programs, and individuals striving for financial stability.

Understanding the Federal Poverty Threshold

The concept of a poverty threshold is foundational to public policy and economic analysis in many countries. In the United States, these thresholds are set and maintained by federal agencies, primarily the U.S. Census Bureau and the Department of Health and Human Services (HHS).

Origins and Purpose

The origins of the U.S. poverty thresholds can be traced back to the early 1960s when Mollie Orshansky, a statistician at the Social Security Administration, developed a set of poverty thresholds based on food consumption patterns. Her methodology leveraged the Department of Agriculture’s economy food plan, which estimated the cost of a nutritionally adequate diet, and multiplied it by three, based on the assumption that food costs represented approximately one-third of a household’s total expenses at the time. This initial framework was adopted by the Office of Economic Opportunity in 1964 and formally designated as the official poverty measure in 1969.

The primary purpose of the federal poverty thresholds is multifaceted:

- Statistical Measure: They provide a consistent metric for tracking poverty rates over time and across different demographic groups.

- Program Eligibility: They serve as a critical eligibility criterion for a wide array of federal assistance programs, including Medicaid, the Supplemental Nutrition Assistance Program (SNAP), housing assistance, and various educational and childcare subsidies.

- Policy Formulation: Policymakers use these figures to assess the impact of economic policies, design new social programs, and allocate resources to combat poverty.

How Poverty is Measured

The official poverty thresholds vary by family size and composition. For a single person, the calculation simplifies considerably, focusing solely on the individual’s income relative to the established threshold for a one-person household. Each year, the U.S. Census Bureau updates these thresholds to account for inflation, using the Consumer Price Index (CPI-U). It’s important to distinguish between the Census Bureau’s poverty thresholds (used for statistical purposes) and the HHS’s poverty guidelines (used for administrative purposes, specifically program eligibility). While closely related, the HHS guidelines are a simplified version of the Census Bureau’s thresholds, making them easier to apply across various programs. Both measures, however, are rooted in the same core concept: an income level below which an individual or family is considered to be living in poverty.

The income considered for comparison against these thresholds is “total money income,” which includes earnings from wages and salaries, self-employment income, Social Security, public assistance, interest, dividends, and other regular income sources before taxes. Non-cash benefits, such as SNAP or Medicaid, are not counted as income in the official poverty measure, a point of frequent debate regarding its accuracy and comprehensiveness.

The Numbers: Federal Poverty Guidelines for Individuals

The specific income thresholds that define poverty for a single person are updated annually and are a central point of reference for various financial and social programs. These figures, while seemingly simple, represent a critical line in the sand for an individual’s economic reality.

Current and Recent Thresholds

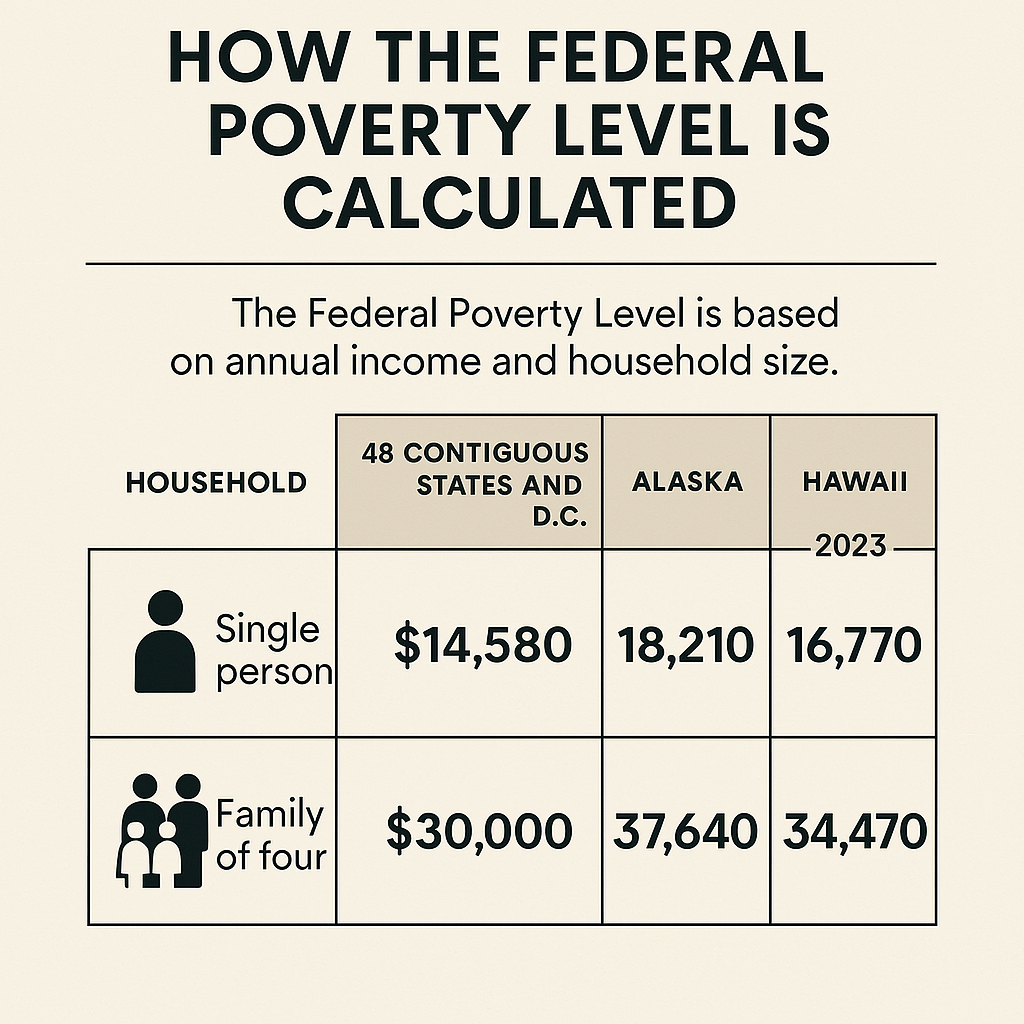

The Department of Health and Human Services (HHS) issues its poverty guidelines, which are often the more commonly referenced figures for program eligibility. For a single person in the contiguous 48 states and the District of Columbia, the poverty level income has typically fallen within a specific range over recent years:

- 2023: $14,580

- 2022: $13,590

- 2021: $12,880

- 2020: $12,760

These figures represent an annual gross income. If a single individual’s total money income falls below these amounts, they are considered to be living in poverty according to federal standards. This means earning an average of roughly $1,215 per month in 2023 for a single person, or about $280 per week. For many, this amount barely covers basic necessities, illustrating the immense financial strain faced by those at or below this line.

It’s crucial to understand that these guidelines are a national average. The cost of living varies dramatically across different regions, cities, and even neighborhoods within the United States. An income that might barely suffice in a rural area could be catastrophically insufficient in a major metropolitan center.

Geographic Variations and Updates

Recognizing significant differences in living costs, the federal poverty guidelines include specific adjustments for Alaska and Hawaii. Due to their exceptionally high cost of living, the poverty thresholds for these states are notably higher than those for the rest of the nation. For example, for a single person in 2023:

- Alaska: $18,210

- Hawaii: $16,770

These adjustments underscore the implicit understanding that a static national figure fails to capture the true economic hardship in certain high-cost areas. However, aside from these two states, no other geographic adjustments are made to the federal poverty guidelines, despite vast differences in housing, transportation, and utility costs across the contiguous U.S. states.

The annual update process involves adjusting the previous year’s guidelines based on the percentage change in the Consumer Price Index for All Urban Consumers (CPI-U), excluding medical care, for the preceding 12-month period. This inflation adjustment ensures that the purchasing power represented by the poverty line remains relatively consistent over time, although critics often argue that the CPI-U doesn’t fully capture the rising costs of essential goods and services for low-income households, particularly healthcare and housing.

The Reality Beyond the Line: True Cost of Living

While federal poverty guidelines provide a statistical benchmark, they often fall short of reflecting the actual financial requirements for a single person to live a dignified life. The “poverty line” and the “living wage” are distinct concepts, with the latter offering a more realistic picture of economic necessity.

Distinguishing Poverty from a Living Wage

The federal poverty level is primarily a statistical and programmatic threshold. It defines a minimum income necessary to avoid destitution based on a decades-old methodology primarily focused on food costs. In contrast, a “living wage” is an income deemed necessary for an individual or family to afford basic necessities, participate in community life, and maintain a minimal standard of living without reliance on public assistance or incurring debt.

For a single person, a living wage typically accounts for basic expenses such as housing, food, transportation, healthcare, and other miscellaneous costs, including modest savings. Research from organizations like MIT’s Living Wage Calculator consistently shows that the living wage for a single adult in nearly every county in the U.S. is significantly higher—often two to three times higher—than the federal poverty guideline. This stark difference highlights the inadequacy of the poverty line as a measure of what it truly takes to make ends meet in today’s economy. An individual earning just above the poverty line, say $15,000 per year, would still find themselves struggling immensely in most parts of the country.

Key Expense Drivers for Single Individuals

For a single person, navigating the financial landscape involves several critical expense categories that consume a disproportionate share of a low income:

- Housing: This is often the largest single expense. Rent, utilities (electricity, gas, water, internet), and renter’s insurance can easily consume 40-60% or more of a low-income individual’s budget, especially in urban and suburban areas.

- Food: While a basic diet can be cheap, a healthy, varied diet can be costly. The official poverty measure’s reliance on food costs from the 1960s often doesn’t align with contemporary nutritional needs or food prices.

- Healthcare: Even for those with some insurance, deductibles, co-pays, and prescription costs can quickly erode a modest income. For the uninsured or underinsured, an unexpected medical event can be financially catastrophic.

- Transportation: Whether it’s the cost of a car (payments, insurance, fuel, maintenance) or public transit fares, getting to work, appointments, and daily errands is a mandatory expense that can be substantial.

- Personal Care and Miscellaneous: This includes clothing, hygiene products, cell phone bills, and other essential but often overlooked expenses.

- Taxes: Even low-income individuals pay taxes (payroll taxes, sales taxes, etc.), further reducing their take-home pay.

The Hidden Costs of Being Poor

Beyond the direct expenses, there are often “hidden costs” associated with being poor. Individuals with limited financial resources often pay more for certain goods and services. For example, they may not have access to banking services and rely on check-cashing services that charge high fees. They might live in neighborhoods with fewer healthy food options, leading to higher costs for groceries or reliance on more expensive convenience stores. Without a car, they might spend more on public transport or struggle to access better-paying jobs further afield. The inability to buy in bulk, take advantage of sales, or invest in durable goods can also lead to higher long-term costs. Furthermore, the constant stress of financial precarity can impact health, job performance, and overall well-being, creating a vicious cycle that is difficult to break.

Navigating Financial Challenges and Building Resilience

For a single person living at or near the poverty line, the challenges are immense. However, a combination of accessing available support, strategic financial planning, and continuous self-improvement can pave the way toward greater financial stability and resilience.

Accessing Support Programs and Resources

Understanding and utilizing federal, state, and local assistance programs is a critical first step for individuals struggling with low income. Eligibility for many of these programs is directly tied to the Federal Poverty Guidelines (FPG), often set at 100%, 138%, or 200% of the FPG. Key programs include:

- Medicaid: Provides health coverage for low-income adults.

- Supplemental Nutrition Assistance Program (SNAP): Offers food assistance benefits.

- Housing Assistance Programs: Such as Section 8 vouchers, which help low-income individuals afford safe and sanitary housing.

- Temporary Assistance for Needy Families (TANF): Provides temporary financial assistance.

- Low Income Home Energy Assistance Program (LIHEAP): Helps with heating and cooling costs.

- Earned Income Tax Credit (EITC): A refundable tax credit for low-to moderate-income working individuals and families, which can provide a significant boost to annual income.

Beyond government programs, numerous non-profit organizations offer food banks, shelter services, job training, and financial counseling. Researching local community resources and connecting with social workers or financial navigators can unlock vital support that addresses immediate needs and helps lay a foundation for future stability.

Strategies for Financial Advancement

Moving beyond the poverty line requires a proactive and strategic approach to personal finance and income generation. For a single person, these strategies can be particularly impactful:

- Aggressive Budgeting and Expense Tracking: Creating a detailed budget to understand where every dollar goes is fundamental. Identifying and cutting unnecessary expenses, no matter how small, can free up crucial funds. Tools and apps can simplify this process, helping individuals stick to their financial goals.

- Building an Emergency Fund: Even a small emergency fund (e.g., $500-$1,000) can prevent minor setbacks from spiraling into major financial crises. Prioritizing saving, even tiny amounts consistently, is essential.

- Debt Management: High-interest debt, such as credit card debt, can be a significant drain. Developing a plan to pay down high-interest debts, perhaps using the “debt snowball” or “debt avalanche” method, can free up more disposable income over time.

- Increasing Income: This is arguably the most powerful lever for a single person. Strategies include:

- Skill Development and Education: Investing in education, vocational training, or acquiring new certifications can significantly boost earning potential.

- Side Hustles: Exploring part-time gigs, freelancing, or other side hustles can supplement primary income. Options range from driving for ride-share services to online content creation or selling crafts.

- Negotiating Salary: For those employed, developing negotiation skills and advocating for fair compensation during reviews or job changes can lead to higher wages.

The Role of Financial Literacy

Financial literacy is not just for the wealthy; it is a vital tool for everyone, especially those striving to overcome financial hardship. Understanding basic concepts like interest rates, credit scores, savings, and investments can empower individuals to make informed decisions and avoid predatory financial products. Free workshops, online courses, and resources from non-profit organizations often provide accessible education on these topics. By building a strong foundation in financial literacy, a single person can not only navigate their current economic situation more effectively but also lay the groundwork for long-term wealth building and financial independence, moving far beyond the mere subsistence level defined by the poverty line.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.